The soaring costs of higher education often leave students and families grappling with substantial student loan debt. Simultaneously, many diligently save for college using 529 education savings plans, designed to offer tax advantages for qualified education expenses. This naturally leads to the question: can the funds carefully accumulated in a 529 plan be used to alleviate the burden of student loan repayment? The answer, while not a simple yes or no, involves understanding the specific rules and regulations governing 529 plans and exploring alternative financial strategies.

This exploration delves into the intricacies of 529 plans, examining their purpose, benefits, and limitations. We’ll compare and contrast various student loan repayment options, highlighting the potential consequences of default and exploring alternative funding sources. Finally, we’ll discuss the importance of comprehensive financial planning to effectively manage both student loan debt and college savings.

Understanding 529 Plans

529 plans are tax-advantaged savings plans designed to encourage saving for future education expenses. They offer significant benefits for families looking to fund college or other qualified education costs, and understanding their mechanics is crucial for maximizing their potential.

Purpose and Benefits of 529 Education Savings Plans

The primary purpose of a 529 plan is to provide a tax-advantaged vehicle for saving money to pay for qualified education expenses. The main benefit is the tax-deferred growth of investments within the plan. Earnings are not taxed as long as the funds are used for qualified expenses. This allows for significant long-term growth potential that surpasses what would be possible in a taxable account. Furthermore, withdrawals used for qualified education expenses are generally tax-free at the federal level. Many states also offer additional tax benefits, such as state income tax deductions for contributions. The flexibility of 529 plans allows for changes in beneficiary designation, enabling adjustments to family circumstances if needed.

Types of 529 Plans

There are two main types of 529 plans: state-sponsored plans and private plans. State-sponsored plans are offered by individual states and often offer residents of that state additional benefits, such as tax deductions or credits. Private plans are managed by private investment firms and may offer a wider range of investment options. The choice between a state-sponsored and a private plan depends on individual circumstances, investment preferences, and the availability of specific benefits within each plan. Both types offer the same federal tax advantages.

Tax Advantages Associated with 529 Plans

The significant tax advantages of 529 plans make them a highly attractive savings option. As mentioned, earnings grow tax-deferred, meaning you don’t pay taxes on investment gains until they are withdrawn. Even better, when withdrawals are used for qualified education expenses, they are generally tax-free at the federal level. This combination of tax-deferred growth and tax-free withdrawals significantly boosts the overall return on investment. State tax benefits vary, so it’s essential to check the rules in your state of residence.

Eligible Education Expenses Covered by 529 Plans

529 plans can cover a wide range of qualified education expenses, extending beyond just tuition fees. This broad coverage enhances their utility and makes them a versatile tool for financing education.

| Expense Type | Example | Eligibility | Tax Implications |

|---|---|---|---|

| Tuition | Undergraduate or graduate tuition fees at a college or university | Must be from an eligible educational institution | Tax-free withdrawals for qualified expenses |

| Fees | Mandatory fees charged by the institution (e.g., student activity fees) | Must be required by the institution | Tax-free withdrawals for qualified expenses |

| Books and Supplies | Textbooks, notebooks, and other required course materials | Must be required for enrolled courses | Tax-free withdrawals for qualified expenses |

| Room and Board | On-campus housing and meal plans | Limited to the actual cost of room and board; proportional to the number of academic periods enrolled | Tax-free withdrawals for qualified expenses |

| Computers and Software | Laptop, tablet, or software required for coursework | Must be directly related to coursework | Tax-free withdrawals for qualified expenses |

| K-12 Expenses | Tuition at a public, private, or religious K-12 school; up to $10,000 per beneficiary per year | Limited to $10,000 per year, per beneficiary. | Tax-free withdrawals for qualified expenses |

Student Loan Repayment Options

Navigating the complexities of student loan repayment can feel daunting, but understanding the available options is crucial for successful repayment and long-term financial health. This section Artikels various repayment plans and their features, highlighting key differences between federal and private loans, and explaining the severe consequences of default.

Federal and Private Student Loan Differences

Federal and private student loans differ significantly in their terms, repayment options, and consequences of default. Federal loans generally offer more borrower protections and flexible repayment plans, while private loans often have stricter terms and less government oversight. For example, federal loans typically offer income-driven repayment plans that adjust monthly payments based on income and family size, a feature rarely found in private loans. Defaulting on a federal loan may lead to wage garnishment and tax refund offset, while the consequences of defaulting on a private loan can vary widely depending on the lender, potentially impacting credit scores and leading to legal action.

Student Loan Repayment Plans

Several repayment plans exist for federal student loans, each designed to cater to different financial situations. These include:

- Standard Repayment: Fixed monthly payments over 10 years.

- Graduated Repayment: Payments start low and gradually increase over 10 years.

- Extended Repayment: Payments are spread over a longer period (up to 25 years), resulting in lower monthly payments but higher overall interest paid.

- Income-Driven Repayment (IDR): Monthly payments are calculated based on your income and family size. Several IDR plans exist, including Income-Based Repayment (IBR), Pay As You Earn (PAYE), and Revised Pay As You Earn (REPAYE). These plans often lead to loan forgiveness after 20 or 25 years, depending on the plan and income level, but the forgiven amount is considered taxable income.

Private student loans typically offer fewer repayment options, often limiting borrowers to standard repayment plans with fixed monthly payments over a set period. Negotiating repayment terms with private lenders can be challenging compared to the established options available for federal loans.

Consequences of Student Loan Default

Defaulting on student loans has serious and long-lasting financial consequences. For federal loans, this can result in:

- Damage to credit score: A significant negative impact on your credit report, making it difficult to obtain loans, credit cards, or even rent an apartment in the future.

- Wage garnishment: A portion of your wages can be legally seized to repay the debt.

- Tax refund offset: Your tax refund can be used to pay off the debt.

- Collection agency involvement: The debt can be sold to a collection agency, which may aggressively pursue repayment.

Defaulting on private loans can also severely damage your credit score and potentially lead to lawsuits and legal action from the lender. The specific consequences depend on the lender and the terms of the loan agreement. In some cases, the lender may pursue legal action to recover the debt, potentially leading to wage garnishment or the seizure of assets.

Student Loan Repayment Flowchart

The following flowchart illustrates the general steps involved in repaying student loans:

[Imagine a flowchart here. The flowchart would begin with “Student Loan Disbursement”. The next step would be “Choose Repayment Plan” branching into “Federal Loan Plans” (listing Standard, Graduated, Extended, IDR) and “Private Loan Plans” (listing Standard). Each plan would lead to “Make Monthly Payments”. Failure to make payments would lead to “Default”, resulting in “Negative Credit Impact”, “Wage Garnishment (Federal)”, “Tax Refund Offset (Federal)”, and “Legal Action (Private/Federal)”. Successful completion of payments would lead to “Loan Repayment Completion”.]

Alternative Funding Options for Student Loans

Securing funding for student loan repayment can be challenging, but several options exist beyond the traditional methods. Exploring these alternatives can significantly impact your repayment strategy and overall financial well-being. Understanding the pros and cons of each approach is crucial for making informed decisions.

Refinancing Student Loans

Refinancing involves replacing your existing student loans with a new loan from a different lender, often at a lower interest rate. This can lead to significant savings over the life of the loan. For example, someone with $50,000 in federal student loans at 7% interest could save thousands of dollars by refinancing to a private loan with a 4% interest rate.

Pros: Lower interest rates, potentially lower monthly payments, simplified repayment process (consolidating multiple loans into one).

Cons: Loss of federal loan benefits (such as income-driven repayment plans and loan forgiveness programs), potential for higher fees, eligibility requirements may be stringent (requiring good credit).

Income-Driven Repayment Plans

Income-driven repayment (IDR) plans adjust your monthly payments based on your income and family size. These plans are offered by the federal government and can significantly lower your monthly payments, especially during periods of lower income. However, it’s important to understand that IDR plans typically extend the repayment period, potentially leading to higher overall interest paid.

Pros: Affordable monthly payments, flexibility to adjust payments based on income changes, potential for loan forgiveness after a specified period (depending on the plan and eligibility).

Cons: Longer repayment periods leading to higher total interest paid, complex application process, eligibility requirements.

Comparison of Repayment Strategies

The choice of repayment strategy depends heavily on individual circumstances. Consider the following comparison:

| Option | Pros | Cons | Eligibility |

|---|---|---|---|

| Standard Repayment Plan (Federal) | Fixed monthly payment, predictable repayment schedule | Potentially high monthly payments, inflexible | Federal student loans |

| Extended Repayment Plan (Federal) | Lower monthly payments than standard plan | Longer repayment period, higher total interest paid | Federal student loans |

| Graduated Repayment Plan (Federal) | Lower initial payments, gradually increasing | Payments may become unaffordable later in the repayment period, higher total interest paid | Federal student loans |

| Income-Driven Repayment Plan (Federal) | Affordable monthly payments based on income | Longer repayment period, potential for higher total interest paid | Federal student loans, meet income requirements |

| Refinancing (Private) | Potentially lower interest rate, simplified repayment | Loss of federal benefits, eligibility requirements | Good credit, meet lender requirements |

Final Wrap-Up

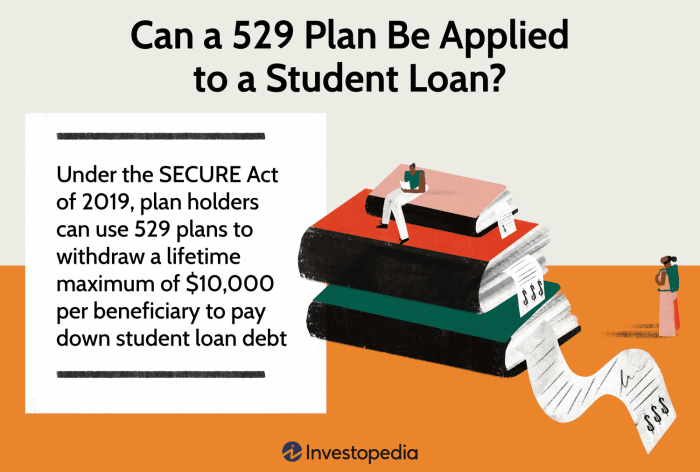

While a 529 plan cannot directly pay off existing student loans, understanding its limitations and exploring alternative financial strategies is crucial. Careful financial planning, encompassing both 529 savings and student loan repayment, is essential for long-term financial well-being. By leveraging the tax advantages of 529 plans for qualified education expenses and strategically managing student loan debt, individuals can navigate the complexities of higher education financing and achieve their financial goals. Remember to consult with a financial advisor for personalized guidance tailored to your specific circumstances.

Detailed FAQs

Can I use a 529 plan for graduate school?

Yes, 529 plans can be used for qualified graduate school expenses.

What happens if I withdraw 529 funds for non-qualified expenses?

You will be subject to income tax on the earnings portion of the withdrawal, plus a 10% penalty.

Are there income limits for contributing to a 529 plan?

No, there are no income limits for contributing to a 529 plan.

Can I change the beneficiary of my 529 plan?

Yes, you can generally change the beneficiary to another family member.

Can I use a 529 plan for room and board?

Yes, room and board expenses are considered qualified education expenses.