The weight of student loan debt casts a long shadow over the lives of millions of graduates. It’s not just about the numbers; it’s about the profound impact on financial stability, mental well-being, career choices, and even geographic mobility. This exploration delves into the multifaceted consequences of this pervasive issue, examining its short-term and long-term effects on individuals and families alike.

From the immediate struggle to manage monthly payments to the long-term implications for saving, investing, and major life decisions, student loan debt presents significant challenges. This analysis will explore the various ways in which this debt shapes the trajectory of graduates’ lives, considering its impact across financial, psychological, and societal dimensions.

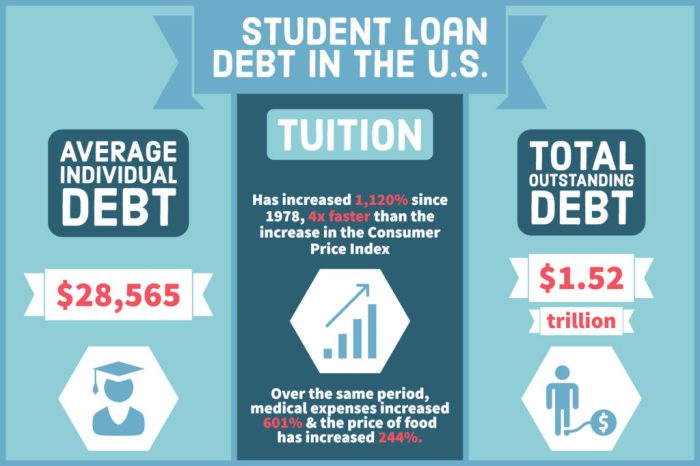

Financial Impacts of Student Loan Debt

The weight of student loan debt significantly impacts the financial well-being of recent graduates, influencing their immediate spending habits and long-term financial goals. The sheer magnitude of these loans can create a ripple effect, affecting everything from daily expenses to major life milestones.

Immediate Financial Burdens

Graduates with substantial student loan debt often face immediate financial constraints. Loan repayments typically begin within six months of graduation, adding a considerable monthly expense to already limited incomes. This can necessitate trade-offs, forcing graduates to postpone or forgo purchases like a new car, upgrading their living situation, or even prioritizing necessities over wants. Many find themselves living paycheck to paycheck, struggling to meet their basic needs while also managing their loan payments. The stress associated with this financial burden can also impact mental health and overall well-being.

Long-Term Effects on Saving and Investing

Student loan debt significantly hampers the ability to save and invest for the future. The substantial monthly payments leave little disposable income for building an emergency fund, contributing to retirement accounts, or investing in other opportunities for wealth building. This can lead to a delayed start to saving and investing, resulting in a smaller nest egg in the long run. The compounding effect of lost investment opportunities over time can be substantial, potentially impacting financial security in retirement. For example, a graduate who delays investing by five years due to loan repayments will miss out on significant potential growth.

Impact on Major Life Decisions

Student loan debt often postpones or prevents major life decisions, such as homeownership and starting a family. The high cost of housing, combined with monthly loan payments, can make homeownership unattainable for many graduates. Similarly, the financial demands of raising children can be overwhelming when burdened with significant student loan debt. Many graduates delay marriage or having children until they have a better handle on their debt, significantly altering their life timelines. For instance, a couple may delay purchasing a home for several years to reduce their debt load, impacting their long-term financial planning.

Financial Comparison: Graduates With and Without Significant Student Loan Debt

The following table illustrates the stark contrast in financial situations between graduates with and without significant student loan debt. These figures are illustrative and represent averages, varying based on individual circumstances and field of study.

| Income Bracket | Average Debt (USD) | Average Savings (USD) | Percentage Owning Homes |

|---|---|---|---|

| $40,000 – $50,000 | $40,000 | $5,000 | 15% |

| $40,000 – $50,000 | $5,000 | $20,000 | 40% |

| $60,000 – $70,000 | $60,000 | $10,000 | 25% |

| $60,000 – $70,000 | $10,000 | $30,000 | 60% |

Mental Health and Well-being

The crushing weight of student loan debt extends far beyond the financial realm, significantly impacting the mental health and overall well-being of borrowers. The constant pressure of repayment, coupled with the often-overwhelming feeling of being trapped in a cycle of debt, contributes to a pervasive sense of stress and anxiety. This isn’t simply a matter of occasional worry; for many, it’s a chronic condition that significantly affects their daily lives and relationships.

The persistent financial strain associated with student loans has a demonstrably negative correlation with mental health. Studies have shown a strong link between high levels of student loan debt and an increased risk of developing or exacerbating conditions like depression and anxiety. The inability to meet basic needs, the fear of financial ruin, and the feeling of being burdened by debt for years, even decades, can lead to feelings of hopelessness and despair. This can manifest in various ways, from difficulty concentrating and decreased productivity to more severe symptoms such as insomnia, social withdrawal, and even suicidal ideation. The constant worry about finances can overshadow other aspects of life, making it difficult to focus on personal goals, relationships, and overall happiness.

The Correlation Between Student Loan Debt and Increased Stress and Anxiety

The constant pressure of looming loan payments, coupled with the often-delayed gratification of career goals and financial stability, fuels a cycle of stress and anxiety. Borrowers often find themselves juggling multiple jobs, sacrificing personal time and leisure activities, and experiencing sleep disturbances due to financial worries. This chronic stress can take a toll on both physical and mental health, leading to increased irritability, difficulty concentrating, and decreased overall well-being. For example, a recent graduate struggling to repay their loans while simultaneously trying to establish themselves in their chosen career might experience heightened anxiety before each loan payment is due, leading to difficulty sleeping and decreased focus at work. This persistent stress can negatively impact their job performance and overall quality of life.

The Impact of Chronic Financial Strain on Depression

Chronic financial strain from student loan debt can significantly contribute to the development or worsening of depression. The feeling of being trapped in a cycle of debt, the inability to plan for the future, and the constant worry about financial stability can lead to feelings of hopelessness, helplessness, and worthlessness – all key symptoms of depression. This can manifest as decreased motivation, social withdrawal, changes in appetite and sleep patterns, and a general lack of interest in activities once enjoyed. Imagine a young professional burdened by substantial student loan debt, struggling to save for a down payment on a house or even afford a vacation. The constant financial pressure can lead to feelings of isolation and despair, exacerbating pre-existing depressive tendencies or triggering the onset of depression.

Strategies for Managing the Psychological Effects of Student Loan Debt

Addressing the mental health consequences of student loan debt requires a multi-pronged approach. Open communication with friends, family, or a therapist can provide crucial emotional support and help individuals process their feelings. Developing healthy coping mechanisms, such as regular exercise, mindfulness practices, and engaging in hobbies, can help manage stress and anxiety levels. Seeking professional help from a therapist or counselor specializing in financial stress is highly recommended. Financial counseling can also provide practical strategies for managing debt and developing a realistic repayment plan. Remember, seeking help is a sign of strength, not weakness. Many resources are available to assist individuals in navigating the emotional and psychological challenges of student loan debt.

Coping Mechanisms for Managing the Mental Health Burden of Student Loans

It is crucial to proactively implement coping strategies to mitigate the negative mental health impact of student loan debt. Here are some effective approaches:

- Seek professional help: A therapist or counselor can provide support and guidance in managing stress and anxiety related to debt.

- Develop a realistic budget: Creating a detailed budget can help reduce financial stress and provide a sense of control.

- Prioritize self-care: Engage in activities that promote relaxation and well-being, such as exercise, meditation, or spending time in nature.

- Connect with support systems: Talk to friends, family, or support groups to share your experiences and receive emotional support.

- Explore debt management options: Consider options like income-driven repayment plans or debt consolidation to make repayment more manageable.

- Practice mindfulness and stress reduction techniques: Techniques like deep breathing exercises and yoga can help manage anxiety and improve mental clarity.

- Set realistic financial goals: Breaking down large financial goals into smaller, achievable steps can reduce feelings of overwhelm.

Career Choices and Opportunities

Student loan debt significantly impacts the career paths graduates pursue, often forcing difficult choices between financial security and personal fulfillment. The weight of repayment can influence decisions about job selection, entrepreneurial ventures, and overall career satisfaction. Understanding these impacts is crucial for both individuals navigating the post-graduate world and policymakers aiming to create a more equitable system.

Influence of Student Loan Debt on Career Choices

The pressure to repay student loans frequently leads graduates to prioritize higher-paying jobs over careers aligned with their passions. Individuals burdened with substantial debt may feel compelled to accept lucrative positions, even if those roles are less fulfilling, to expedite loan repayment. This can lead to a sense of professional dissatisfaction and a feeling of being trapped in a career path chosen out of necessity rather than genuine interest. For example, a recent graduate with a passion for environmental science might opt for a higher-paying job in finance to quickly reduce their debt, foregoing their initial career aspirations. This prioritization of financial stability often overshadows long-term career goals and personal well-being.

Effect of Student Loan Debt on Entrepreneurial Pursuits

The substantial financial burden of student loan debt can significantly deter individuals from pursuing entrepreneurial ventures. Starting a business requires significant upfront investment and carries inherent risk, making it a less appealing option for those already struggling with loan repayments. The fear of business failure, coupled with the ongoing pressure of loan payments, creates a significant barrier to entry for aspiring entrepreneurs. For instance, an individual with a strong business idea but considerable student loan debt might choose a more stable, albeit less rewarding, employment path to ensure consistent income for loan repayments. This risk aversion can stifle innovation and limit economic growth.

Relationship Between Student Loan Debt and Career Satisfaction

A strong correlation exists between the level of student loan debt and career satisfaction. Studies consistently show that individuals with higher levels of student loan debt report lower levels of job satisfaction. The constant financial stress associated with loan repayments can negatively impact mental well-being, leading to burnout and decreased engagement in the workplace. This stress can also affect decision-making, potentially hindering career advancement. For example, a graduate with a manageable debt load might feel more comfortable taking risks, pursuing further education, or negotiating for better compensation, leading to greater career satisfaction. Conversely, someone burdened with significant debt might feel limited in their career options and opportunities for growth.

Comparison of Career Paths Chosen by Graduates with Varying Debt Levels

The following table illustrates a comparison of career paths typically chosen by graduates with high versus low student loan debt levels. It is important to note that these are averages and individual experiences will vary.

| Career Field | Average Salary | Average Debt | Job Satisfaction Rating (1-5, 5 being highest) |

|---|---|---|---|

| Engineering | $80,000 | $50,000 | 4 |

| Education | $45,000 | $40,000 | 3.5 |

| Finance | $95,000 | $60,000 | 3 |

| Arts | $40,000 | $30,000 | 4.5 |

Geographic Mobility and Location Decisions

Student loan debt significantly impacts the life choices of recent graduates, particularly regarding where they live and work. The weight of repayment obligations often restricts geographic mobility, forcing graduates to prioritize financial stability over potentially more fulfilling career paths or lifestyle preferences in different locations. This section explores the intricate relationship between student loan debt and location decisions.

Student loan debt limits geographic mobility primarily through two intertwined factors: job opportunities and cost of living. Graduates often feel compelled to accept employment in areas with a higher concentration of jobs in their field, even if the salary isn’t as competitive or the cost of living is exceptionally high. This is because the pressure to begin repaying loans immediately overrides the desire to explore other options that might offer better long-term prospects or a higher quality of life. Conversely, even with a desirable job offer, the high cost of living in certain areas can make repayment incredibly challenging, forcing graduates to seek more affordable locations, potentially limiting their career advancement.

Repayment Plan Influence on Location Choices

The type of repayment plan a graduate chooses directly influences their location decisions. Income-driven repayment plans, for instance, tie monthly payments to income. This can make living in high-cost areas more manageable initially, as payments are lower, but it can also prolong the repayment period significantly. Conversely, standard repayment plans demand fixed monthly payments regardless of income, making it crucial for graduates to secure employment in areas where their salary can comfortably cover these payments. This often necessitates accepting jobs in locations with a lower cost of living, even if career progression is slower.

Impact on Relocating for Better Opportunities

The ability to relocate for better opportunities is often severely hampered by student loan debt. The financial burden of moving – including security deposits, moving expenses, and potential temporary unemployment – can be insurmountable for graduates already struggling with loan repayments. Even if a better job opportunity arises in a different city or state, the associated costs and risks might deter graduates from pursuing it, trapping them in less desirable situations purely for financial stability. This can limit career growth and earning potential over the long term.

Scenario: Weighing Job Offers with Student Loan Debt

Imagine Sarah, a recent graduate with $50,000 in student loan debt. She receives two job offers: one in her hometown, a smaller city with a lower cost of living and a salary of $45,000, and another in a major metropolitan area with a higher cost of living and a salary of $65,000. While the higher salary in the city would seemingly be better, the increased cost of rent, transportation, and everyday expenses would significantly reduce her disposable income, making loan repayment a considerable challenge. In her hometown, while the salary is lower, her living expenses are significantly less, allowing her to allocate a larger portion of her income towards loan repayment, potentially reducing the overall repayment period and associated interest. Sarah must carefully weigh these factors, considering her long-term financial goals and quality of life alongside her career aspirations, to make the most informed decision.

Intergenerational Effects of Student Loan Debt

Student loan debt is no longer a burden solely carried by the individual borrower; its impact reverberates through families, affecting financial stability across generations. The escalating cost of higher education has created a situation where many families are deeply entangled in the financial consequences of student loans, creating a ripple effect that impacts not only the borrower but also their parents, siblings, and future generations.

The weight of student loan debt significantly alters the financial landscape for families, influencing crucial decisions related to savings, investments, and long-term financial planning. This impact is especially pronounced for families with multiple children pursuing higher education.

Financial Strain on Parents Supporting Children with Student Loan Debt

Parents often find themselves providing substantial financial support to their children grappling with significant student loan debt. This support can manifest in various ways, including co-signing loans, directly contributing to loan repayments, or providing financial assistance for living expenses while their children are repaying loans. This financial burden can delay or prevent parents from achieving their own financial goals, such as retirement planning or purchasing a home. For example, a parent might postpone retirement to help their child manage their student loan payments, impacting their own financial security in later life. Similarly, parents might delay saving for their own retirement or for their grandchildren’s education, diverting funds to help their children with their debt. The stress and anxiety associated with these financial responsibilities can also negatively affect family relationships.

Long-Term Implications for Inheritance and Wealth Transfer

Student loan debt can significantly reduce the amount of wealth a family can transfer to future generations. The considerable debt repayments often consume a substantial portion of a borrower’s income, leaving less available for saving and investing. This directly impacts the amount of inheritance or financial support they can provide to their children or other family members. For instance, a family who might have otherwise been able to leave a substantial inheritance to their children may instead find that a large portion of their assets are used to repay the children’s student loan debt, thereby reducing the overall wealth transfer. This intergenerational impact can perpetuate a cycle of debt and limit opportunities for future generations.

Comparison of Financial Inheritance Prospects

The financial inheritance prospects for families with and without substantial student loan debt differ dramatically. Families without significant student loan burdens typically have greater capacity to save, invest, and accumulate wealth over time. This accumulated wealth can then be passed on to future generations as an inheritance, providing financial security and opportunities for their children and grandchildren. In contrast, families burdened by student loan debt often experience a reduced capacity for wealth accumulation, leading to a smaller inheritance or even the need for children to contribute financially to their parents’ well-being in their later years instead of receiving an inheritance.

| Factor | Families Without Substantial Student Loan Debt | Families With Substantial Student Loan Debt | Impact on Future Generations |

|---|---|---|---|

| Savings & Investments | Higher savings rates, diversified investment portfolios | Lower savings rates, limited investment opportunities due to debt repayments | Greater financial security and opportunities for inheritance |

| Wealth Accumulation | Significant wealth accumulation over time | Reduced wealth accumulation due to debt servicing | Larger inheritance and potential for intergenerational wealth building |

| Inheritance | Substantial inheritance passed down to future generations | Smaller or potentially no inheritance due to debt burden | Reduced financial security and fewer opportunities for future generations |

| Financial Independence | Early achievement of financial independence | Delayed achievement of financial independence due to debt repayment | Impact on career choices, homeownership, and other major life decisions |

Impact on Social Mobility

Student loan debt significantly impacts social mobility, the ability of individuals to improve their economic and social standing. The substantial financial burden imposed by loans can hinder upward economic advancement, trapping individuals and families in cycles of debt and limiting their opportunities for progress. This effect is particularly pronounced for certain vulnerable populations, further exacerbating existing inequalities.

The weight of student loan debt disproportionately affects specific demographics. Lower-income individuals and families, often relying on loans to finance higher education, face a steeper climb towards financial stability. Similarly, minority groups frequently experience higher rates of loan default and struggle more with repayment due to systemic barriers and historical disadvantages. The accumulation of debt can limit access to homeownership, investment opportunities, and other pathways to wealth accumulation that contribute to social mobility.

Government Policies and Programs Addressing Social Mobility

Several government policies and programs aim to mitigate the impact of student loan debt on social mobility. Income-driven repayment plans adjust monthly payments based on income, making repayment more manageable for borrowers with lower earnings. Loan forgiveness programs, such as those targeting public service workers or those who attended specific institutions, provide partial or complete debt cancellation, offering a pathway to financial freedom and enhanced social mobility. Additionally, increased funding for grants and scholarships, aimed at reducing reliance on loans, is crucial for improving access to higher education and bolstering social mobility prospects. These initiatives represent efforts to create a more equitable system where financial constraints do not unduly hinder upward economic advancement.

Case Study: The Miller Family

The Miller family exemplifies the impact of student loan debt on social mobility. Both parents, Sarah and David, incurred significant student loan debt pursuing undergraduate and graduate degrees. While their education enhanced their earning potential, the substantial loan repayments consumed a large portion of their income. This limited their ability to save for a down payment on a house, restricting them to a smaller, less desirable neighborhood with poorer schools for their children. Furthermore, the financial strain impacted their ability to invest in their children’s future, limiting opportunities for extracurricular activities and college savings. The Millers’ trajectory, while individually successful in terms of education and employment, was hampered by the persistent burden of student loan debt, demonstrating how it can impede the intergenerational transfer of wealth and opportunity, a key element of social mobility.

Final Thoughts

In conclusion, the effects of student loan debt extend far beyond the simple repayment of borrowed funds. It profoundly influences nearly every aspect of a graduate’s life, from their financial security and mental health to their career path and even their social mobility. Understanding these far-reaching consequences is crucial for developing effective strategies to mitigate the burden and create a more equitable future for generations to come. Further research and policy interventions are essential to address this complex issue effectively.

FAQ Summary

What are some common strategies for managing student loan debt?

Strategies include creating a realistic budget, exploring income-driven repayment plans, refinancing loans to secure lower interest rates, and seeking financial counseling.

Can student loan debt affect my credit score?

Yes, missed or late payments on student loans can negatively impact your credit score, making it harder to obtain loans or credit in the future.

What happens if I can’t repay my student loans?

Failure to repay student loans can lead to wage garnishment, tax refund offset, and damage to your credit score. It’s crucial to contact your loan servicer to explore options like deferment or forbearance if you are facing financial hardship.

Are there any government programs to help with student loan debt?

Yes, several government programs exist, including income-driven repayment plans and loan forgiveness programs for certain professions (e.g., public service). Eligibility criteria vary.