Navigating the complexities of student loan repayment can be daunting, and understanding the potential impact of deferment on your credit score is crucial. Many borrowers choose deferment to temporarily pause payments, but this decision carries implications that extend beyond immediate financial relief. This exploration delves into the multifaceted relationship between student loan deferment and your creditworthiness, offering insights to help you make informed choices.

This guide clarifies how deferments are reported, the factors influencing their impact, and strategies for mitigating potential negative consequences. We’ll also explore alternatives to deferment and provide a roadmap for managing your credit effectively, both during and after a deferment period. By understanding the nuances of this process, you can navigate student loan repayment with greater confidence and protect your financial future.

Deferment Definition and Types

Student loan deferment is a temporary postponement of your student loan payments. This means you don’t have to make payments during the deferment period, offering a much-needed financial break. However, it’s crucial to understand that deferment doesn’t erase your debt; it simply delays payments. Interest may still accrue during the deferment period, depending on the type of loan and the specific deferment granted. Let’s explore the different types of deferments available.

Types of Student Loan Deferments

Several types of deferments exist, each with its own eligibility requirements and implications. Understanding these differences is vital for borrowers to choose the most appropriate option for their circumstances.

In-School Deferment

In-school deferment is available to students enrolled at least half-time in an eligible degree or certificate program. Eligibility typically requires maintaining satisfactory academic progress, as defined by the institution. This deferment usually continues as long as the student remains enrolled at least half-time.

Economic Hardship Deferment

This deferment is granted to borrowers experiencing significant financial difficulties. Specific criteria for eligibility vary by lender, but generally involve demonstrating an inability to meet basic living expenses while also making loan payments. Documentation, such as proof of unemployment or financial hardship, is usually required.

Unemployment Deferment

Borrowers who have become unemployed may qualify for an unemployment deferment. Lenders typically require proof of unemployment, such as a termination letter or unemployment benefits documentation. The duration of this deferment is often limited and may require periodic recertification of unemployment status.

Total and Permanent Disability Deferment

Borrowers with a total and permanent disability may be eligible for a deferment. This usually requires documentation from a physician or other qualified medical professional certifying the disability. This deferment can be indefinite, depending on the borrower’s circumstances and the lender’s policies.

Deferment Comparison Table

The following table compares the different types of deferments, highlighting their key characteristics:

| Deferment Type | Eligibility Criteria | Duration | Interest Accrual |

|---|---|---|---|

| In-School | At least half-time enrollment in eligible program, satisfactory academic progress | Duration of enrollment | May accrue (depending on loan type) |

| Economic Hardship | Demonstrated financial hardship, inability to meet basic living expenses | Varies, often requires periodic recertification | May accrue (depending on loan type) |

| Unemployment | Proof of unemployment | Varies, often requires periodic recertification | May accrue (depending on loan type) |

| Total and Permanent Disability | Documentation of total and permanent disability from a qualified medical professional | Potentially indefinite | May accrue (depending on loan type) |

Impact on Credit Reporting

A student loan deferment, while offering temporary relief from repayment, does have implications for your credit report. Understanding how deferments are reported and their potential effects on your credit score is crucial for managing your financial health. The impact isn’t uniform and depends on several factors, including the lender and how they choose to report the deferment.

Deferments are generally reported to credit bureaus as “accounts in deferment.” This notation indicates that payments are temporarily suspended, not necessarily that you’re delinquent. However, the exact way this information appears on your credit report can vary. Some lenders may report the deferment as a negative mark, potentially affecting your credit score, while others may handle it more neutrally. The key difference lies in how the lender codes the information to the credit bureaus.

Lender Reporting Practices

The manner in which a lender reports a deferment significantly influences its impact on your credit score. Some lenders might report the deferment as a “special comment” without impacting the credit score directly, while others may report it as a form of delinquency, albeit a specific one associated with a deferment. For example, one lender might simply note the deferment period, while another might register it as a missed payment, even though it’s a legally sanctioned temporary pause in payments. This inconsistency across lenders highlights the importance of understanding your specific lender’s policies. Consider contacting your lender directly to clarify their reporting practices regarding deferments to manage expectations about your credit score.

Potential Effects on Credit Scores

While a deferment itself doesn’t automatically tank your credit score, it can still have a negative impact. The effect depends on several factors, including your overall credit history, the length of the deferment, and the lender’s reporting methods. A long deferment period, for instance, could signal to lenders that you may be struggling with repayment, even if the deferment was due to unforeseen circumstances like job loss or illness. Furthermore, the mere presence of a deferment on your report, even if not negatively coded, could slightly lower your credit score due to the impact on your payment history, a significant factor in credit scoring models. Conversely, a short deferment period, coupled with a strong credit history, might have a minimal or negligible impact.

Factors Influencing Credit Score Impact

While a student loan deferment can temporarily affect your credit score, several factors can mitigate the negative impact or even lessen its severity. Understanding these factors is crucial for maintaining a healthy credit profile, even during periods of financial strain. The effect of a deferment is not uniform and depends significantly on pre-existing credit habits and the overall management of one’s financial situation.

The impact of a deferment on your credit score isn’t solely determined by the deferment itself. Several factors interact to determine the overall effect. A strong credit history prior to the deferment acts as a buffer, reducing the negative impact. Conversely, a weak credit history will magnify the negative effects. Furthermore, the length of the deferment and how diligently other credit obligations are managed also play significant roles.

Mitigating Factors

Several factors can lessen the negative impact of a student loan deferment on your credit score. Maintaining a good payment history on all other credit accounts is paramount. This demonstrates responsible financial behavior to credit bureaus, counteracting the effect of the deferred student loan payment. Additionally, keeping your credit utilization low (the amount of credit you use compared to your total available credit) will also help. A low credit utilization ratio generally indicates responsible credit management. Finally, proactively communicating with your lenders about your financial situation can sometimes help mitigate negative impacts on your credit report.

Pre-Deferment Credit History’s Influence

A strong credit history before initiating a deferment significantly influences the overall impact on your credit score. Individuals with a long history of on-time payments and low credit utilization will generally experience a less dramatic drop in their score compared to those with a shorter or weaker credit history. For example, someone with a consistently high credit score and a long history of responsible credit use might only see a minor dip during a deferment, while someone with a thin credit file or a history of late payments could experience a more substantial decline. This is because credit scoring models consider the entire history of credit activity, not just the current status.

Deferment vs. Late Payments

The impact of a student loan deferment on your credit score differs significantly from the impact of late payments on other accounts. While a deferment is reported to credit bureaus, it’s generally treated differently than a missed payment. A deferment indicates a temporary suspension of payments, not necessarily a failure to pay. Late payments, on the other hand, directly signal a failure to meet financial obligations. Consequently, late payments typically have a more severe negative impact on credit scores than a student loan deferment. The difference lies in the intent and the reporting – a deferment is a planned action, while a late payment is often an indicator of financial distress. For instance, a single late payment can significantly lower a credit score, whereas a deferment, especially for a short period, might have a much less pronounced effect, particularly for individuals with otherwise excellent credit.

Managing Credit During Deferment

Entering a student loan deferment can feel unsettling, especially concerning its potential impact on your credit score. However, proactive management can significantly mitigate negative effects and even maintain a healthy credit profile. By understanding the implications and taking strategic steps, you can navigate this period effectively without long-term damage to your financial standing.

Maintaining a Positive Credit History During Deferment

While deferment temporarily pauses your loan payments, it doesn’t erase your credit history. To maintain a good credit score, consistent responsible financial behavior remains crucial. This includes managing existing credit accounts effectively and continuing to demonstrate creditworthiness.

- Pay other bills on time: Diligent payment of all other debts, such as credit cards and other loans, showcases responsible financial management, counteracting the negative impact of the deferred loan. Consistent on-time payments demonstrate your commitment to fulfilling financial obligations.

- Keep credit utilization low: Avoid maxing out your credit cards. Aim to keep your credit utilization ratio (the amount you owe compared to your total credit limit) below 30%, ideally closer to 10%. This shows lenders you manage your credit responsibly.

- Monitor your credit report regularly: Check your credit report from all three major credit bureaus (Equifax, Experian, and TransUnion) at least annually through AnnualCreditReport.com. This allows you to identify and address any errors or discrepancies promptly.

- Consider a secured credit card: If you have limited credit history or are rebuilding your credit, a secured credit card can help. This requires a security deposit, which acts as your credit limit, and responsible use can improve your credit score over time. It provides a safe way to build credit while avoiding high-interest rates and potential debt.

Proactive Steps to Protect Credit During Deferment

Taking proactive steps beyond simply paying your other bills can further protect your credit health. These actions demonstrate financial responsibility and help maintain a positive credit profile despite the temporary pause in loan payments.

- Communicate with your lender: Inform your student loan servicer of your financial situation and explore options for minimizing the impact on your credit report. While deferment is already in place, open communication can sometimes lead to additional support or alternative solutions.

- Explore credit counseling: If you anticipate challenges managing your finances, consider seeking guidance from a reputable credit counseling agency. They can offer personalized advice and help you create a budget to manage your debts effectively.

- Avoid opening new credit accounts unnecessarily: While it’s important to manage existing credit, avoid applying for new credit cards or loans during deferment. Multiple credit applications can temporarily lower your credit score.

Checklist for Minimizing Negative Impact of Deferment

This checklist provides a structured approach to managing your credit effectively during a student loan deferment period.

| Action | Frequency | Importance |

|---|---|---|

| Pay all non-student loan bills on time | Monthly | High – Demonstrates consistent financial responsibility |

| Check credit report for accuracy | Annually (or more frequently if needed) | High – Prevents negative impacts from errors |

| Maintain low credit utilization | Monthly | High – Shows responsible credit management |

| Review budget and expenses | Monthly | Medium – Helps identify areas for improvement |

| Communicate with loan servicer | As needed | Medium – Keeps them informed and allows for potential solutions |

Alternatives to Deferment

Student loan deferment, while offering temporary relief, isn’t always the best solution. Understanding alternative options is crucial for managing your student loan debt effectively and minimizing potential negative impacts on your credit score. Exploring these alternatives allows you to choose the strategy that best aligns with your current financial situation and long-term goals.

For borrowers facing temporary financial hardship, several alternatives to deferment exist, each with its own set of advantages and disadvantages. Careful consideration of these options is vital to making an informed decision.

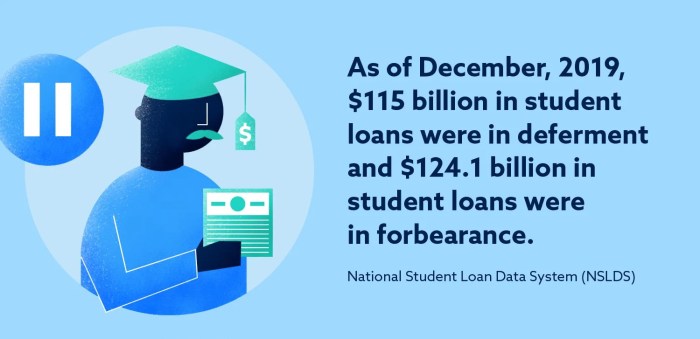

Forbearance

Forbearance is another option that temporarily suspends or reduces your student loan payments. Unlike deferment, forbearance doesn’t always require demonstrating financial hardship. However, interest usually continues to accrue during forbearance, leading to a larger total debt upon repayment. This can significantly impact the overall cost of your loans.

- Advantage: Offers flexibility for borrowers facing temporary financial difficulties, even without strict hardship requirements.

- Disadvantage: Interest typically continues to accrue, increasing the total loan amount over time. This can lead to a larger repayment burden later.

Income-Driven Repayment Plans

Income-driven repayment (IDR) plans adjust your monthly payments based on your income and family size. These plans are designed to make student loan repayment more manageable for borrowers with lower incomes. While payments are lower, repayment periods are often extended, potentially leading to more interest paid over the life of the loan. Several types of IDR plans exist, each with slightly different eligibility requirements and payment calculation methods.

- Advantage: Lower monthly payments make repayment more affordable for borrowers with limited income.

- Disadvantage: Extended repayment periods can result in paying significantly more interest over the life of the loan. Also, the exact terms and eligibility criteria can vary depending on the specific IDR plan and lender.

Comparison of Deferment, Forbearance, and Income-Driven Repayment

The following table summarizes the key differences between deferment, forbearance, and income-driven repayment plans:

| Feature | Deferment | Forbearance | Income-Driven Repayment |

|---|---|---|---|

| Payment Suspension | Yes | Yes (or reduced) | Adjusted based on income |

| Interest Accrual | May or may not accrue, depending on the loan type | Usually accrues | Usually accrues |

| Financial Hardship Requirement | Often required | Often not required | Based on income and family size |

| Credit Score Impact | Potentially negative | Potentially negative | Potentially less negative than deferment or forbearance |

| Repayment Period | Extended | Extended | Extended |

Long-Term Effects on Credit

While a student loan deferment offers temporary relief, its long-term impact on your creditworthiness shouldn’t be underestimated. Understanding these potential consequences and proactively managing your finances during and after a deferment period is crucial for maintaining a healthy credit profile.

The primary long-term effect stems from the fact that deferment, while not technically a default, still indicates to lenders that you’ve had difficulty making timely payments on your student loans. This can create a negative perception, even if the deferment was due to legitimate circumstances such as unemployment or illness. The length of the deferment and your overall credit history will influence the severity of this impact. A short deferment for a specific, temporary hardship may have a minimal effect, whereas multiple extended deferments can significantly hurt your credit score.

Impact on Future Loan Applications

Successfully navigating a deferment period can positively influence future loan applications. Demonstrating responsible financial behavior during and after the deferment – such as consistent on-time payments once the deferment ends and maintaining a low debt-to-income ratio – shows lenders that you’re capable of managing your finances effectively, even during challenging times. This responsible approach can improve your chances of securing favorable loan terms and interest rates in the future. Conversely, a history of multiple deferments without clear evidence of financial recovery might make obtaining future loans more difficult and potentially result in higher interest rates. For example, someone who secured a deferment due to unemployment but diligently saved and repaid the deferred amount promptly might be viewed favorably compared to someone who repeatedly used deferments without demonstrable efforts to improve their financial situation.

Rebuilding Credit After Deferment

Rebuilding credit after a deferment requires a proactive and consistent approach. The key is to demonstrate responsible credit behavior. This involves consistently making on-time payments on all your debts, including the student loans that were previously deferred. Maintaining a low credit utilization ratio (the percentage of available credit you’re using) is also essential. A ratio below 30% is generally considered healthy. Furthermore, regularly monitoring your credit report for errors and disputing any inaccuracies is crucial. Consider exploring credit-building strategies such as securing a secured credit card or becoming an authorized user on a credit card with a positive payment history. These actions, combined with consistent on-time payments, can gradually improve your credit score over time. The time it takes to rebuild credit varies depending on the severity of the initial impact and your subsequent financial behavior; however, consistent responsible management can lead to significant improvements within a few years.

Illustrative Scenarios

Understanding the impact of student loan deferment on credit scores requires examining specific examples. The effect isn’t uniform; it depends heavily on individual financial situations and credit history before the deferment. Two contrasting scenarios illustrate this variability.

Minimal Impact Scenario

This scenario depicts a borrower with a strong credit history who utilizes a deferment strategically. Sarah, a 30-year-old software engineer, has a FICO score of 780. She has consistently made on-time payments on all her accounts (credit cards, auto loan) for the past seven years, maintaining a low credit utilization ratio (always below 10%). Her student loan debt totals $50,000, and she chooses a short-term deferment (6 months) due to a temporary job loss. During the deferment, she continues to make timely payments on all other debts and actively monitors her credit report. After the deferment period, she resumes her student loan payments immediately. The temporary deferment has a negligible impact on her credit score, dropping perhaps a few points, which quickly recover due to her overall strong credit profile. Her credit utilization remains low, and her payment history remains excellent.

Significant Impact Scenario

In contrast, consider Mark, a 25-year-old recent graduate with a FICO score of 620. He has a history of late payments on several credit accounts and carries a high credit utilization rate (consistently above 70%). His student loan debt is $75,000, and he enters a 2-year income-driven repayment plan deferment due to financial hardship. During this deferment, he struggles to manage his other debts, resulting in further late payments and increased credit utilization. He doesn’t actively monitor his credit report and doesn’t take steps to improve his financial situation. After the deferment period, he is still unable to make consistent payments on his student loans. His credit score plummets significantly, potentially dropping below 550. The prolonged deferment, coupled with his pre-existing poor credit habits, severely damages his creditworthiness.

Visual Representation of Credit Score Changes

In the minimal impact scenario (Sarah), the credit score graph would show a slight, temporary dip during the six-month deferment period. The line representing the score would descend only slightly, then rapidly rebound to near its original level upon resumption of payments. The overall trend remains consistently high.

In the significant impact scenario (Mark), the graph would illustrate a far more dramatic decline. The score would gradually decrease during the two-year deferment due to the accumulation of negative information on his credit report. The line would fall substantially and remain low, even after the deferment, reflecting the continued financial difficulties and poor payment behavior. The overall trend is a significant downward trajectory.

Closing Notes

Ultimately, while a student loan deferment can temporarily impact your credit score, proactive management and a clear understanding of the process can minimize negative effects. By carefully considering the implications, exploring alternative repayment options, and actively protecting your credit history, you can successfully navigate this phase of loan repayment and maintain a strong financial standing. Remember that responsible financial planning is key to long-term credit health, regardless of your repayment strategy.

Helpful Answers

Does a deferment always negatively impact my credit score?

Not necessarily. The impact varies depending on factors like your credit history before deferment and how the lender reports it.

How long does the negative impact of a deferment last?

The negative impact typically remains on your credit report for the duration of the deferment and for several years afterward, depending on the reporting practices of your lender and credit bureaus.

Can I get a new loan while my student loans are deferred?

It will be more difficult. Lenders consider deferments when assessing your creditworthiness, potentially impacting your approval chances and interest rates.

What if I forget to reapply for deferment?

Failing to reapply will likely result in your loan entering delinquency, significantly harming your credit score. Contact your loan servicer immediately if this happens.