Navigating the world of federal student loans can feel overwhelming, but understanding the application process is key to securing the financial support you need for higher education. This guide provides a comprehensive overview of the Federal Direct Student Loan program, from application to repayment, equipping you with the knowledge to make informed decisions about your financial future.

We’ll explore the various loan types, eligibility requirements, and repayment plans available. We’ll also address common concerns, such as managing student loan debt and avoiding potential scams. Our aim is to empower you with the tools and information necessary to confidently navigate the federal student loan system.

Understanding the Application Process

Applying for federal direct student loans can seem daunting, but the process is straightforward when broken down into manageable steps. This section will guide you through each stage, outlining the necessary documentation and explaining the different loan types available. Understanding your options is key to making informed decisions about financing your education.

The Step-by-Step Application Process

The application process generally begins with completing the Free Application for Federal Student Aid (FAFSA). This form collects information about your financial situation and is used to determine your eligibility for federal student aid, including loans. After submitting the FAFSA, your chosen school will receive your Student Aid Report (SAR), which summarizes your information and eligibility. Next, you’ll receive an offer of federal student aid from your school, detailing the types and amounts of loans you’re eligible for. You’ll then need to accept your loan offer and complete a master promissory note (MPN), a legally binding agreement outlining your responsibilities as a borrower. Finally, the funds will be disbursed to your school to cover tuition and fees.

Required Documentation

To successfully apply for federal direct student loans, you’ll need to provide accurate information on the FAFSA. This includes your Social Security number, tax information (yours and your parents’, if applicable), and information about your assets and income. You may also need to provide additional documentation if requested, such as proof of residency or verification of income. Failing to provide accurate and complete information can delay or prevent the processing of your application.

Types of Federal Student Loans and Eligibility Criteria

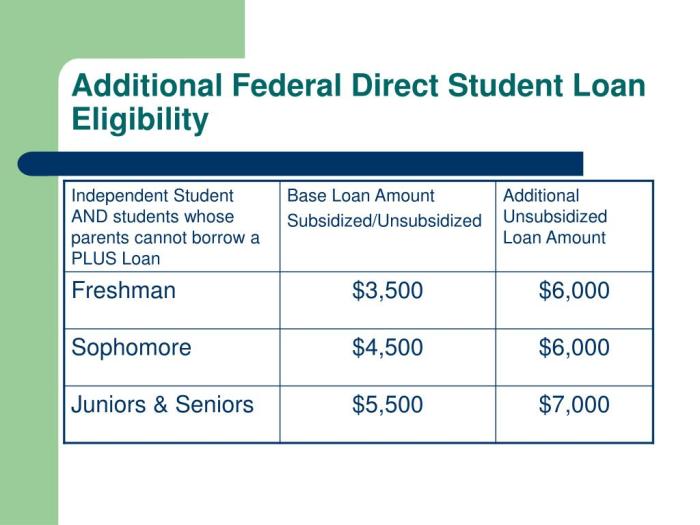

Several types of federal student loans are available, each with its own eligibility requirements and repayment terms. The primary types are Subsidized and Unsubsidized Federal Stafford Loans, and Federal PLUS Loans (for parents and graduate students). Eligibility generally depends on factors such as your enrollment status (full-time or part-time), your financial need (for subsidized loans), and your credit history (for PLUS loans). Graduate students may also be eligible for Grad PLUS loans.

Comparison of Federal Student Loan Programs

| Loan Type | Interest Rate (Example – Rates Vary) | Repayment Options | Eligibility Requirements |

|---|---|---|---|

| Subsidized Stafford Loan | Variable, set annually by the government. Example: 4.99% | Standard, Graduated, Extended | Demonstrated financial need, enrolled at least half-time |

| Unsubsidized Stafford Loan | Variable, set annually by the government. Example: 4.99% | Standard, Graduated, Extended | Enrolled at least half-time |

| Federal PLUS Loan (Parent) | Variable, set annually by the government. Example: 7.54% | Standard, Extended | Parent must pass a credit check |

| Federal PLUS Loan (Graduate) | Variable, set annually by the government. Example: 7.54% | Standard, Extended | Graduate student must pass a credit check |

*Note: Interest rates are subject to change and are examples only. Always check the official government website for the most up-to-date information.*

Financial Aid and Loan Eligibility

Securing federal student loans involves understanding the financial aid process and determining your eligibility. This section clarifies the requirements and steps involved in obtaining federal student aid. Successful navigation of this process hinges on a thorough understanding of the Free Application for Federal Student Aid (FAFSA) and the factors influencing loan approval.

The Free Application for Federal Student Aid (FAFSA)

The FAFSA is a crucial form that determines your eligibility for federal student aid, including grants, loans, and work-study programs. Completing the FAFSA is the first step in applying for federal student loans. It gathers information about your family’s financial situation to assess your need for financial assistance. The information provided on the FAFSA is used by your chosen educational institution and federal agencies to determine the amount and type of aid you qualify for. The FAFSA process is generally completed online, and it’s vital to ensure accuracy in all information provided.

Factors Influencing Loan Eligibility

Several factors determine your eligibility for federal student loans. These include your credit history (although a credit history is not always required for federal student loans, especially subsidized ones), your income and your family’s income, your enrollment status (full-time or part-time), and your educational program. Demonstrating a clear path towards completing your education, such as a solid academic record, also positively impacts your application. The Department of Education uses a complex formula considering these factors to calculate your eligibility. For example, a student with a high family income may receive less federal aid than a student from a low-income family.

Completing the FAFSA Form: A Step-by-Step Guide

- Gather Necessary Information: Before starting, collect your Social Security number, federal tax information (IRS tax returns, W-2s, and other relevant tax documents), and your parents’ tax information (if you are a dependent student). You will also need your driver’s license or state identification number.

- Create an FSA ID: Both you and your parent (if you are a dependent student) will need an FSA ID to sign the FAFSA electronically. This is a username and password combination that allows you to access and manage your FAFSA information.

- Complete the Online Application: Access the FAFSA website and begin filling out the application. Answer all questions accurately and completely. The website provides instructions and definitions for each section.

- Review and Submit: Carefully review your completed application for any errors before submitting. Once submitted, you cannot make changes, so double-check everything.

- Track Your FAFSA Status: After submission, monitor your FAFSA status online to see if any additional information is required from you or your parents.

Key Factors Affecting Financial Aid Eligibility

It’s important to understand the key factors that influence your eligibility for financial aid. These factors are carefully weighed by the federal government and your institution to determine the amount of aid you receive.

- Demonstrated Financial Need: This is calculated based on your family’s income and assets, as reported on the FAFSA.

- Cost of Attendance: This includes tuition, fees, room and board, books, and other educational expenses.

- Enrollment Status: Full-time students generally receive more financial aid than part-time students.

- Academic Progress: Maintaining satisfactory academic progress is usually a requirement for continued eligibility for financial aid.

- Citizenship Status: Eligibility requirements may vary based on your citizenship status.

Repayment Plans and Options

Understanding your repayment options is crucial for successfully managing your federal student loans. Choosing the right plan can significantly impact your monthly payments, overall repayment time, and potential long-term costs. This section details the various plans available and helps you understand the key differences between them.

Standard Repayment Plan

The Standard Repayment Plan is the default option for most federal student loan borrowers. It involves fixed monthly payments over a 10-year period. This plan offers predictable payments, but the monthly payments can be higher compared to income-driven repayment plans. The benefit is that you pay off your loans faster, reducing the overall interest accrued. However, the higher monthly payments might be a burden for some borrowers, especially those with limited income immediately after graduation.

Graduated Repayment Plan

The Graduated Repayment Plan starts with lower monthly payments that gradually increase over time. This option might be appealing to borrowers anticipating income growth, as the initial lower payments ease the financial strain in the early years of repayment. However, the increasing payments can become challenging later on, and the total repayment period is still 10 years. It’s important to carefully consider whether your projected income growth will sufficiently offset the escalating payments.

Extended Repayment Plan

The Extended Repayment Plan provides longer repayment terms, up to 25 years, resulting in lower monthly payments compared to the standard plan. This option is beneficial for borrowers who need more manageable monthly payments, but it results in significantly higher overall interest payments due to the extended repayment period. This increased interest cost should be carefully weighed against the benefit of lower monthly payments.

Income-Driven Repayment Plans

Income-driven repayment (IDR) plans link your monthly payments to your income and family size. These plans are designed to make repayment more manageable, particularly for borrowers with lower incomes. Several IDR plans exist, including Income-Based Repayment (IBR), Pay As You Earn (PAYE), Revised Pay As You Earn (REPAYE), and Income-Contingent Repayment (ICR). These plans offer lower monthly payments than standard repayment plans, potentially resulting in loan forgiveness after a set period (typically 20 or 25 years), depending on the specific plan and your income. However, this loan forgiveness comes at the cost of paying significantly more interest over the life of the loan.

Comparing Standard and Income-Driven Repayment Plans

Standard repayment plans offer fixed monthly payments over 10 years, leading to faster loan payoff but potentially higher monthly payments. Income-driven repayment plans offer lower monthly payments based on your income and family size, but repayment takes longer and may result in higher total interest paid, with potential for loan forgiveness after a specified period. The choice depends on your individual financial situation and long-term goals.

Applying for an Income-Driven Repayment Plan

Applying for an IDR plan typically involves completing a federal student aid application (FAFSA) and providing documentation of your income and family size. You’ll need to submit this information through the student loan servicer’s website. The specific requirements and processes may vary slightly depending on your loan servicer and the chosen IDR plan. It is crucial to carefully review the requirements and deadlines to ensure a smooth application process.

Repayment Plan Comparison

| Repayment Plan | Monthly Payment | Loan Forgiveness | Potential Long-Term Costs |

|---|---|---|---|

| Standard | Higher, fixed | None | Lower due to shorter repayment period |

| Graduated | Starts low, increases over time | None | Moderate, depending on income growth |

| Extended | Lower, fixed | None | Higher due to longer repayment period |

| Income-Driven (IBR, PAYE, REPAYE, ICR) | Variable, based on income | Possible after 20-25 years | Potentially very high due to longer repayment and accrued interest |

Managing Student Loan Debt

Successfully navigating student loan debt requires proactive planning and responsible financial habits. Understanding repayment strategies, budgeting effectively, and knowing the consequences of default are crucial steps towards achieving financial freedom after graduation. This section will provide practical strategies and resources to help you manage your student loans effectively.

Effective student loan debt management hinges on a well-defined strategy. This involves understanding your loan terms (interest rates, repayment periods, etc.), creating a realistic repayment plan, and consistently adhering to it. Prioritizing loan repayment within your overall financial picture is essential. For example, some borrowers prioritize paying off high-interest loans first to minimize the total interest paid over the life of the loan, while others prefer a consistent payment amount across all loans for easier budgeting. Choosing the right strategy depends on individual financial circumstances and goals.

Budgeting and Financial Planning for Loan Repayment

A comprehensive budget is the cornerstone of successful loan repayment. This involves tracking income and expenses meticulously to identify areas for savings. By allocating a specific portion of your monthly income towards loan payments, you establish a consistent repayment schedule and avoid accumulating further debt. Financial planning tools, such as budgeting apps or spreadsheets, can assist in visualizing your financial situation and projecting future loan repayment progress. For instance, a detailed budget might show that by reducing discretionary spending on entertainment by 10%, a borrower could free up an additional $200 per month for loan payments, significantly accelerating repayment.

Consequences of Student Loan Default

Defaulting on student loan payments carries severe financial and legal repercussions. These consequences can include damage to your credit score, wage garnishment, tax refund offset, and difficulty securing future loans or credit. Furthermore, defaulting can negatively impact your ability to rent an apartment, obtain a mortgage, or even secure certain employment opportunities. The impact of a default can be long-lasting and significantly hinder your financial well-being. For example, a severely damaged credit score resulting from default can make it challenging to secure a mortgage for years to come, delaying major life milestones such as homeownership.

Resources for Borrowers Facing Financial Hardship

Facing financial hardship does not necessitate defaulting on your student loans. Several resources can provide assistance and support.

It is crucial to explore available options before considering default. Many loan servicers offer hardship programs, such as forbearance or deferment, which can temporarily suspend or reduce payments. These programs provide breathing room to manage unforeseen financial challenges, allowing borrowers to regain financial stability before resuming regular payments. Additionally, government programs and non-profit organizations offer financial counseling and debt management services.

- Federal Student Aid website: Provides information on repayment plans, hardship programs, and other resources.

- National Foundation for Credit Counseling (NFCC): Offers free and low-cost credit counseling services.

- Student Loan Borrower Assistance (SLBA): A non-profit organization that assists borrowers in navigating the student loan system.

- Your loan servicer: Contact your loan servicer directly to discuss your options and explore potential solutions.

Potential Scams and Misinformation

Navigating the world of student loans can be complex, and unfortunately, this complexity makes borrowers vulnerable to scams and misleading information. Understanding common tactics used by fraudsters and how to identify reliable sources of information is crucial to protecting your financial well-being. This section will Artikel several common scams and provide guidance on how to avoid them.

Sadly, many individuals prey on students and recent graduates facing the financial pressures of higher education. These individuals often leverage the urgency and stress associated with student loan applications and repayment to their advantage. Understanding these tactics is the first step toward avoiding them.

Common Student Loan Scams

Scammers employ various deceptive methods to target student loan borrowers. These often involve promises of loan forgiveness, debt consolidation at unrealistically low rates, or expedited application processing for a fee. These promises are almost always false and designed to steal your money or personal information. For example, a common scam involves emails or text messages claiming to represent the Department of Education, offering immediate loan forgiveness in exchange for a processing fee. Another involves websites mimicking the official Federal Student Aid website, subtly altering the URL to appear legitimate. These fraudulent websites may request personal information, banking details, or Social Security numbers under the guise of loan application processing.

Recognizing and Avoiding Fraudulent Loan Services

Several key indicators can help you identify fraudulent loan services or websites. Be wary of any service promising unusually quick loan processing, extremely low interest rates, or loan forgiveness without meeting the established eligibility requirements. Always verify the legitimacy of a website or organization by independently researching their credentials. Check the Federal Student Aid website (StudentAid.gov) for a list of approved loan servicers and avoid any entity not listed there. Legitimate organizations will never ask for payment upfront for loan processing or forgiveness. If you are asked for money before receiving any services, this is a significant red flag. Furthermore, carefully review any website’s URL; fraudulent sites often use similar-looking but slightly altered URLs to trick users into believing they are legitimate.

Examples of Misleading Information

Misleading information regarding student loans is often disseminated through various channels, including social media, email, and unofficial websites. This information can range from inaccurate details about repayment plans to false promises of rapid loan forgiveness. For example, claims that simply contacting a loan servicer will automatically qualify you for loan forgiveness are untrue. Similarly, advertisements promising significantly lower interest rates than those offered by the government should be treated with extreme skepticism. Always cross-reference information from multiple reliable sources before making any decisions related to your student loans.

The Role of the Federal Student Aid Website

The official Federal Student Aid website (StudentAid.gov) serves as the primary source of accurate and up-to-date information regarding federal student loans. This website provides comprehensive details on loan applications, repayment plans, eligibility criteria, and other crucial aspects of student loan management. It is imperative to rely solely on this website and other official government sources for information about your student loans, avoiding any information obtained from unverified sources. The site also offers resources to help you identify and report potential scams. Using StudentAid.gov ensures you are making informed decisions based on accurate and reliable data.

Impact of Federal Student Loans on Higher Education

Federal student loans have profoundly reshaped the landscape of higher education in the United States, making college accessible to millions who might otherwise be unable to afford it. This accessibility, however, comes with significant long-term financial implications for both individuals and the national economy. Understanding these impacts is crucial for prospective students and policymakers alike.

The availability of federal student loans has undeniably increased access to higher education. For many students, these loans bridge the gap between tuition costs and family resources, enabling them to pursue degrees and certifications that lead to better job opportunities and higher earning potential. This increased access has broadened participation in higher education, leading to a more diverse and skilled workforce. However, the rising cost of tuition, coupled with increased borrowing, has also created a complex relationship between student loan debt and future financial well-being.

Student Loan Debt’s Influence on Future Financial Planning

The significant debt burden incurred by many students can significantly impact their future financial planning. Graduates often face challenges in saving for retirement, purchasing a home, or starting a family due to monthly loan repayments. This can lead to delayed major life milestones and increased financial stress. For example, a graduate with $50,000 in student loan debt at a 6% interest rate might face monthly payments exceeding $500, significantly impacting their ability to save and invest for the future. Careful budgeting and financial planning are essential to navigate these challenges.

Long-Term Implications of Educational Borrowing

The long-term implications of borrowing for education extend beyond immediate repayment responsibilities. The weight of student loan debt can influence career choices, limiting individuals’ ability to pursue lower-paying but personally fulfilling careers. It can also affect credit scores, making it more difficult to secure loans for other major purchases like a car or a house. Furthermore, the accumulation of interest over time can substantially increase the total amount owed, potentially extending the repayment period for many years. Understanding these long-term consequences is vital for making informed borrowing decisions.

Visual Representation: Student Loan Debt and Future Earnings

Imagine a graph with two lines. The horizontal axis represents years after graduation, and the vertical axis represents cumulative earnings (in dollars). One line, representing “Earnings without Student Loan Debt,” steadily increases, showing a consistent growth in income over time. The other line, “Earnings with Student Loan Debt,” initially shows a slower increase due to loan repayments, then eventually intersects and surpasses the “no debt” line. However, the gap between the two lines illustrates the opportunity cost of borrowing – the potential for greater wealth accumulation if debt was avoided or minimized. The point where the lines intersect demonstrates the point at which the increased earning power from a degree offsets the financial burden of the loan. This intersection point will vary greatly depending on the amount borrowed, the interest rate, and the individual’s earning potential after graduation. For example, a high-earning professional might reach this intersection point relatively quickly, while someone in a lower-paying field might take considerably longer, or may never surpass the earnings of someone without student loan debt.

Final Summary

Securing a federal direct student loan is a significant step towards achieving your educational goals. By understanding the application process, eligibility criteria, and available repayment options, you can effectively manage your student loan debt and plan for a financially secure future. Remember to utilize the resources available to you and always be vigilant against potential scams. With careful planning and informed decision-making, you can successfully navigate the path to higher education and beyond.

FAQ Insights

What happens if I don’t complete the FAFSA?

You won’t be eligible for most federal student aid, including federal direct student loans.

Can I get a federal student loan if I have bad credit?

Credit history is not a primary factor for federal student loans, but your overall financial situation will be considered.

What if I can’t afford my student loan payments?

Contact your loan servicer to explore income-driven repayment plans or other options to avoid default.

How long do I have to repay my student loans?

The repayment period varies depending on the loan type and repayment plan chosen; it can range from 10 to 25 years or more.

Where can I find trustworthy information about federal student loans?

The official Federal Student Aid website (studentaid.gov) is the best source for accurate and up-to-date information.