The question of parental responsibility for student loans is a complex one, weaving together legal obligations, financial implications, and deeply personal family dynamics. Navigating this landscape requires understanding not only the legal frameworks governing co-signing and loan defaults but also the broader societal and cultural expectations surrounding higher education financing. This exploration delves into the multifaceted aspects of this issue, offering insights into the potential risks and rewards for both parents and students.

From the legal ramifications of co-signing in various countries to the long-term financial consequences for parents, we will examine the ethical considerations and practical strategies involved. We’ll also explore alternative funding options and the importance of open communication between parents and students about financial responsibility. Ultimately, this discussion aims to provide a comprehensive understanding of the shared responsibilities and potential pitfalls inherent in financing a child’s education.

Legal Responsibility of Parents for Student Loans

The legal landscape surrounding parental responsibility for student loan debt varies significantly across countries. Understanding these differences is crucial for both parents and students considering co-signing loan agreements. This section will examine the legal frameworks in several countries, focusing on co-signer liability, consequences of default, and legal recourse available to parents.

Co-Signer Liability and Legal Frameworks

In many countries, parents can become legally liable for their children’s student loans by co-signing the loan agreement. This act transforms them from a guarantor into a joint borrower, meaning they share equal responsibility for repayment. The legal framework governing this varies. For instance, in the United States, the co-signer is equally responsible for repayment regardless of the student’s ability or willingness to pay. This is explicitly detailed within the loan agreement. In contrast, some countries may have stricter regulations about the process of co-signing, requiring specific legal documentation or providing certain protections for co-signers. The specific conditions under which a parent becomes legally liable are defined within the loan agreement itself and relevant national legislation. It is imperative to thoroughly understand these terms before signing.

Consequences of Student Loan Default

The ramifications for parents when a student defaults on their loan differ substantially depending on the country’s legal system and the specific loan agreement. In the US, lenders can pursue legal action against the co-signer, including wage garnishment, bank levy, and even lawsuits to recover the outstanding debt. The severity of the consequences is directly proportional to the amount owed. In other countries, the legal recourse available to lenders might be limited or the legal process might be more protracted. Some jurisdictions may offer more protection to co-signers, while others may hold them fully responsible. Understanding the potential legal repercussions is essential for parents before committing to co-signing.

Legal Recourse for Parents

Parents who have co-signed a student loan and are facing financial hardship due to the student’s default may have limited legal recourse. In some countries, they might be able to negotiate repayment plans with the lender or seek bankruptcy protection. However, these options are not always available or effective. The success of such legal maneuvers depends greatly on the specific circumstances and the country’s legal system. In some cases, mediation or arbitration might be an option to resolve the dispute. The availability of such recourse depends on individual circumstances and local laws.

Comparative Table of Parental Liability

| Country | Co-signer Liability | Default Consequences for Parents | Legal Recourse for Parents |

|---|---|---|---|

| United States | Joint and several liability; equally responsible with the student. | Wage garnishment, bank levy, lawsuits, credit score damage. | Negotiating repayment plans, bankruptcy (limited effectiveness), mediation. |

| Canada | Liability depends on the loan agreement; can be joint and several or secondary. | Credit score damage, legal action to recover debt (depending on agreement). | Negotiating repayment plans, potential for legal challenges to the lender’s actions (depending on agreement). |

| United Kingdom | Generally, parents are not automatically liable unless they co-sign. | Limited direct consequences for parents unless they co-signed. | Limited recourse unless they are a co-signer on the loan. |

Financial Implications for Parents

Co-signing a student loan can have significant and long-lasting financial consequences for parents. While it can be a helpful way to assist a child in securing higher education, it’s crucial to understand the potential risks involved before committing. The responsibility for repayment falls equally on both the student and the co-signer, regardless of the student’s ability to repay.

The most significant risk is the impact on a parent’s credit score and future borrowing capacity. A missed or late payment on the student loan will negatively affect the co-signer’s credit history, just as if it were their own debt. This can make it harder to obtain loans in the future, such as a mortgage, car loan, or even a credit card, or it can result in higher interest rates on future borrowing. Furthermore, the student loan debt will appear on the co-signer’s credit report, potentially reducing their credit score and available credit lines.

Impact on Credit Score and Borrowing Capacity

Co-signing a student loan significantly impacts a parent’s credit score and borrowing capacity. For example, let’s say a parent with an excellent credit score of 780 co-signs a $50,000 student loan for their child. If the student experiences financial hardship and defaults on the loan, the parent’s credit score could plummet by 100 or more points, depending on the severity and duration of the delinquency. This drop could lead to higher interest rates on future loans, limiting access to credit, and potentially impacting their ability to buy a house or refinance their mortgage. In essence, a co-signed student loan becomes a significant financial liability that can affect the parent’s financial stability for years to come. The potential for such a dramatic negative impact underscores the importance of careful consideration before co-signing.

Strategies to Mitigate Financial Risks

Before co-signing, parents should explore all available options for their child to finance their education, including scholarships, grants, and federal student loans. Thoroughly reviewing the loan terms, including the interest rate, repayment schedule, and potential fees, is crucial. Parents should also carefully assess their own financial situation to determine if they can comfortably afford to make payments should the student default. A robust emergency fund can help buffer against unexpected financial setbacks. Finally, open communication with the student about their financial responsibility and repayment plan is essential. A co-signing agreement that includes clear expectations and contingencies can help protect both parties.

Ethical Considerations for Parents

The decision to co-sign a student loan involves ethical considerations. Parents must honestly assess their financial capacity and the potential risks involved. While supporting a child’s education is admirable, it’s unethical to co-sign if doing so jeopardizes the parent’s financial security or future goals. Open and honest conversations with the student about the responsibilities of repayment are crucial. The student should understand the weight of the financial commitment and the potential consequences of default. Ultimately, the decision should be based on a realistic assessment of both the parent’s and the student’s financial capabilities and a shared understanding of the responsibilities involved.

The Role of Parental Financial Support in Higher Education

Parental financial support plays a significant role in determining a student’s access to and success in higher education. While student loans often dominate the conversation, a multitude of other avenues exist through which parents can contribute, each with its own implications for both the student and the family’s financial well-being. Understanding these options and their potential impacts is crucial for making informed decisions.

Parents can contribute to their children’s education in various ways beyond loans and co-signing. Direct financial contributions, such as covering tuition costs, living expenses, or purchasing necessary materials, are common. Many parents also utilize savings plans, like 529 plans, to set aside funds specifically for education. Additionally, parents may offer support indirectly through reduced living expenses at home, allowing students to allocate more of their own resources towards education. The choice of support method significantly impacts the student’s debt burden and overall financial stability post-graduation.

Alternative Funding Options for Higher Education

A range of options exists for financing higher education, excluding student loans and parental co-signing. These alternatives can help mitigate the reliance on debt and reduce the overall financial strain on both the student and their family.

- Scholarships and Grants: These are forms of financial aid that do not need to be repaid. Many scholarships are merit-based, awarded for academic achievement, athletic prowess, or other talents. Grants are often need-based, awarded to students demonstrating financial need. A diligent search for scholarships and grants can significantly reduce educational costs.

- Work-Study Programs: These programs allow students to work part-time while attending school, earning money to contribute towards their education. This reduces reliance on loans and teaches valuable work experience.

- Savings Plans (529 Plans): These tax-advantaged savings plans allow families to save money specifically for education expenses. Earnings grow tax-deferred, and withdrawals are tax-free when used for qualified education expenses.

- Part-time Employment (Student): Students can supplement their financial resources through part-time jobs. This approach can reduce the need for loans or parental support, fostering independence and financial responsibility.

Impact of Parental Financial Contributions on Student Debt Management

The level of parental financial support directly influences a student’s ability to manage debt. Significant parental contributions can drastically reduce or eliminate the need for student loans, minimizing post-graduation debt. Conversely, minimal parental support can lead to increased reliance on loans, potentially resulting in substantial debt burdens that impact future financial decisions like purchasing a home or starting a family. For example, a student whose parents cover tuition may only need to take out loans for living expenses, while a student with no parental support might need to borrow significantly more to cover all educational costs.

Pros and Cons of Parental Financial Support Methods

Choosing the right method of parental support involves weighing the benefits and drawbacks of each approach.

- Direct Tuition Payments:

- Pros: Reduces or eliminates student loan debt, simplifies financial planning for the student.

- Cons: Can place a significant financial burden on parents, may require parents to delay their own financial goals.

- Contribution to Living Expenses:

- Pros: Reduces student loan need, allows students to focus on studies.

- Cons: May not fully cover all expenses, requires ongoing financial commitment from parents.

- 529 Plan Contributions:

- Pros: Tax advantages, dedicated savings for education, encourages financial planning.

- Cons: Requires consistent savings over time, funds may not cover all educational costs.

The Student’s Responsibility and Parental Expectations

Navigating the financial landscape of higher education requires a clear understanding of roles and responsibilities. While parental support plays a significant part, the student’s active participation in managing their educational debt is equally crucial. A healthy balance between parental assistance and the student’s personal accountability is key to avoiding future financial strain and fostering a sense of independence.

The student’s primary responsibility begins with a thorough understanding of the financial aid package, including loans, grants, and scholarships. This involves carefully reviewing loan terms, interest rates, and repayment schedules. Active participation in budgeting and tracking expenses related to tuition, fees, books, and living costs is essential. Students should actively seek opportunities to minimize debt by exploring scholarships and grants, working part-time jobs, and prioritizing their academic performance to maintain eligibility for financial aid. Proactive communication with financial aid offices and loan servicers is also vital for staying informed and addressing any potential issues promptly. Failure to understand and manage these aspects can lead to significant financial difficulties later.

Student Responsibilities in Debt Management

Effective debt management starts with understanding the loan terms. This includes knowing the principal amount borrowed, the interest rate, the repayment schedule, and any associated fees. Students should create a realistic budget that incorporates loan repayments alongside other expenses. Tracking income and expenses is crucial to ensure they stay on track. Exploring repayment options, such as income-driven repayment plans, can help manage debt in the long term. Finally, maintaining good credit is essential for securing favorable loan terms in the future. A proactive approach to debt management minimizes the long-term financial burden and fosters responsible financial habits.

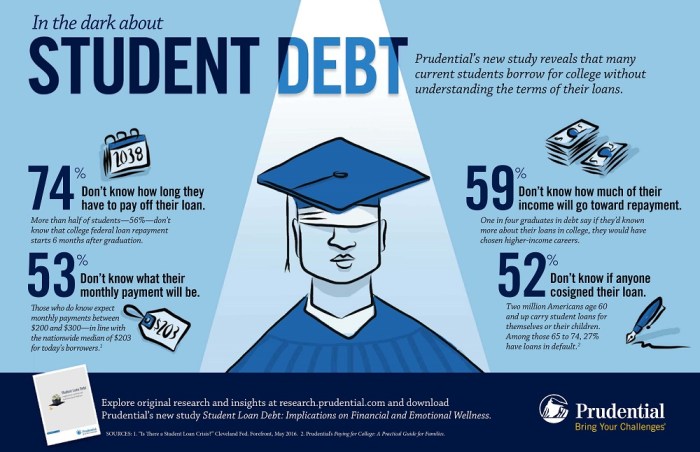

Parental Expectations versus Willingness to Help

Parental expectations regarding their children’s financial independence often vary widely. Some parents may anticipate their children contributing significantly to their education costs, emphasizing the importance of self-reliance and responsible financial management. Others may be more willing to provide extensive financial support, viewing it as an investment in their child’s future. This difference in expectations can stem from various factors, including family financial resources, cultural background, and individual parenting styles. The willingness of parents to help with student loans is often influenced by their own financial situations, their perception of their child’s academic commitment, and their belief in the value of higher education. A candid conversation about expectations and financial capabilities is crucial to avoid misunderstandings and potential conflicts.

Potential for Conflict Between Parents and Students

Disagreements between parents and students regarding financial responsibility for higher education are common. These conflicts often arise from differing perspectives on the level of parental support needed, the student’s commitment to academic success, and the choices made regarding educational paths and lifestyle expenses. Unrealistic expectations from either side can exacerbate the tension. For instance, parents might expect their child to maintain a strict budget while the student feels their allowances are insufficient. Conversely, students may feel entitled to a certain level of financial support without considering their own contribution. Open communication, mutual understanding, and a willingness to compromise are essential to navigate these challenges effectively.

Hypothetical Scenario: A Healthy Discussion

Imagine Sarah, a bright and motivated student, is discussing her college financing with her parents. Sarah’s parents have offered to contribute a significant portion of her tuition but expect her to take on some student loans and work part-time. Sarah, initially hesitant about taking on debt, expresses her concerns about managing repayments after graduation. Her parents, understanding her apprehension, explain the various repayment options available and emphasize the importance of responsible budgeting. They jointly review Sarah’s financial aid package, discussing the terms of her loans and the potential impact on her post-graduation financial situation. They agree on a realistic budget that includes her part-time job earnings, loan repayments, and living expenses. This collaborative approach fosters mutual understanding and a shared sense of responsibility for managing her educational debt. The open dialogue ensures that Sarah feels supported while also understanding the importance of her own contribution and responsible financial management.

Societal and Cultural Influences

Societal norms and cultural expectations significantly shape the degree to which parents become involved in financing their children’s higher education. These influences are complex and multifaceted, varying across different socioeconomic groups and cultural backgrounds, and evolving across generations. Understanding these influences is crucial for comprehending the prevailing dynamics surrounding student loan debt and parental responsibility.

Cultural norms often dictate the perceived role of parents in their children’s lives, including educational pursuits. In some cultures, providing financial support for higher education is deeply ingrained, considered a fundamental parental obligation and a demonstration of love and commitment. In others, the expectation may be less pronounced, with greater emphasis placed on individual responsibility and self-reliance. This difference significantly affects the likelihood of parents taking on student loan debt.

Socioeconomic and Cultural Variations in Parental Involvement

The level of parental financial involvement in higher education is strongly correlated with socioeconomic status. Higher-income families generally have more resources available to directly fund their children’s education, reducing reliance on loans. Conversely, lower-income families may face greater financial constraints, forcing them to rely heavily on loans, potentially leading to increased parental debt. Cultural backgrounds also play a role; some cultures prioritize education intensely, motivating parents to make significant sacrifices, while others may place less emphasis on higher education, influencing parental financial investment accordingly. For example, in some Asian cultures, there is a strong emphasis on filial piety and the importance of parental support for children’s education, often resulting in significant parental financial contribution. In contrast, some Western cultures may place a greater emphasis on individual achievement and self-reliance, leading to less parental financial involvement.

Generational Differences in Perspectives on Parental Responsibility

Generational differences significantly influence perspectives on parental responsibility for student loans. Older generations may have experienced different educational landscapes, where higher education was less accessible and more reliant on parental support. Consequently, they may feel a stronger sense of obligation to assist their children financially. Younger generations, having grown up in an era of rising tuition costs and increased student loan debt, may hold differing views, with some expecting more individual responsibility for educational financing. This generational shift in perspectives can lead to intergenerational conflict and varying expectations regarding parental financial support. For instance, Baby Boomers may feel a stronger moral obligation to help their children with college expenses than Millennials, who might be more accustomed to navigating the higher education system with significant personal debt.

Societal Pressures and Educational Debt

Societal pressures related to higher education and the accumulation of educational debt significantly impact both parents and students. The societal emphasis on higher education as a pathway to success can create immense pressure on parents to provide financial support, even if it means incurring substantial debt. Students, in turn, may feel pressured to pursue higher education, even if it leads to significant personal debt, due to societal expectations and the perceived necessity of a college degree for career advancement. This pressure can lead to unrealistic expectations about educational attainment and career prospects, potentially resulting in overwhelming levels of debt for both parents and students. The “keeping up with the Joneses” mentality, prevalent in many societies, further exacerbates this issue, driving parents to make financial commitments beyond their means to ensure their children receive a higher education comparable to that of their peers.

Closing Summary

Ultimately, the decision of whether or not parents should co-sign student loans is deeply personal and should be made after careful consideration of the legal, financial, and familial implications. Open communication between parents and students is crucial in establishing realistic expectations and shared responsibility. While the financial burden of higher education can be significant, a proactive and informed approach can mitigate risks and foster a stronger parent-child relationship throughout the process. Understanding the legal landscape and exploring alternative financing options empowers families to make informed choices that align with their individual circumstances and values.

Helpful Answers

What happens if my child defaults on their student loan and I co-signed?

If your child defaults, the lender can pursue you for the full amount of the loan. This can severely damage your credit score and financial stability.

Can I refuse to co-sign a student loan for my child?

Yes, you are under no legal obligation to co-sign. Your child may need to explore alternative funding options.

Are there any benefits to co-signing a student loan?

Co-signing may improve your child’s chances of loan approval and potentially secure a lower interest rate. However, this comes with significant risk.

What if I can no longer afford to help with my child’s student loans?

Explore options like loan refinancing or contacting the lender to discuss repayment plans. Early communication is key.