Navigating the world of higher education often involves the significant financial hurdle of tuition fees. For many students, securing a bank loan becomes a necessary step towards achieving their academic goals. Understanding the various types of student loans, their associated interest rates, repayment plans, and the overall application process is crucial for making informed decisions. This guide provides a comprehensive overview to empower students to confidently manage their finances throughout their educational journey and beyond.

From understanding eligibility criteria and required documentation to exploring alternative funding options and developing effective debt management strategies, we aim to equip you with the knowledge needed to make the most of your student loan experience. We’ll delve into the complexities of interest calculations, repayment schedules, and the long-term financial implications of borrowing, ensuring you’re well-prepared for the financial realities of higher education.

Application Process and Requirements

Securing a student bank loan can significantly ease the financial burden of higher education. Understanding the application process and meeting the necessary requirements are crucial for a successful outcome. This section Artikels the typical steps involved, the required documentation, the importance of creditworthiness, and provides helpful tips for a smooth application.

The application process generally involves several key steps. First, you’ll need to research and select a lender that offers student loans. This might involve comparing interest rates, repayment terms, and any additional fees. Next, you’ll complete the loan application form, providing accurate and complete information. This typically includes personal details, educational information, and financial details. Following this, the lender will review your application and supporting documentation. This review process may involve a credit check and verification of your information. Finally, if approved, you’ll receive a loan offer outlining the terms and conditions. You’ll then need to accept the offer and complete any necessary paperwork to finalize the loan process.

Required Documents for Student Loan Applications

Lenders typically require a comprehensive set of documents to verify your identity, eligibility, and financial standing. Providing these documents promptly and accurately is essential for a timely processing of your application.

- Completed loan application form

- Proof of identity (e.g., driver’s license, passport)

- Social Security number

- Proof of enrollment (e.g., acceptance letter, transcript)

- Financial aid award letter (if applicable)

- Tax returns (or proof of income for co-signer, if required)

- Bank statements (to demonstrate financial responsibility)

Importance of Credit Score and Co-signers

A good credit score significantly increases your chances of loan approval and securing favorable interest rates. Lenders assess your credit history to determine your creditworthiness and risk level. A strong credit score indicates responsible financial management, reducing the lender’s perceived risk. However, if you lack a credit history or have a low credit score, a co-signer with a good credit history can greatly improve your chances of approval. A co-signer essentially guarantees the loan, sharing the responsibility for repayment.

Tips for Efficient and Successful Application

Careful planning and preparation can greatly enhance the efficiency and success of your student loan application. These tips can streamline the process and increase your chances of approval.

- Start early: Begin the application process well in advance of your academic deadlines to allow ample time for processing.

- Gather all necessary documents: Organize all required documents before starting the application to avoid delays.

- Read the fine print: Carefully review the loan terms and conditions before accepting the loan offer.

- Maintain open communication: Keep in contact with your lender throughout the application process to address any questions or concerns promptly.

- Consider your repayment options: Explore different repayment plans to choose one that aligns with your anticipated post-graduation income.

Interest Rates and Repayment Plans

Understanding the interest rates and repayment options for your student loan is crucial for effective financial planning. Choosing the right repayment plan can significantly impact your overall loan cost and your monthly budget. This section details how interest rates are calculated and Artikels various repayment plans available, allowing you to make informed decisions.

Interest Rate Determination

Several factors influence the interest rate applied to your student loan. These include your credit history (if applicable), the type of loan (federal or private), the loan’s term length, and prevailing market interest rates. Federal student loans typically have fixed interest rates, meaning the rate remains constant throughout the loan’s life. Private student loans, however, often have variable interest rates, which fluctuate based on market conditions. A strong credit history may lead to a lower interest rate, while a shorter loan term might also result in a lower rate. The specific interest rate offered will be clearly stated in your loan agreement.

Repayment Plan Options

Several repayment plans cater to different financial situations and repayment preferences. Understanding the differences between these plans is key to choosing the best option for your circumstances.

- Standard Repayment Plan: This plan typically involves fixed monthly payments over a 10-year period. It’s straightforward but may result in higher monthly payments compared to other options.

- Graduated Repayment Plan: Payments start low and gradually increase over time. This can be helpful initially, but payments can become significantly higher in later years.

- Extended Repayment Plan: This plan extends the repayment period, leading to lower monthly payments but higher overall interest costs. The repayment period can extend up to 25 years for some federal loans.

- Income-Driven Repayment Plans (IDR): These plans link your monthly payment to your income and family size. Payments are typically lower than other plans, but the repayment period can be longer, potentially leading to higher overall interest paid. Examples include Income-Based Repayment (IBR), Pay As You Earn (PAYE), and Revised Pay As You Earn (REPAYE).

Long-Term Cost Comparison

The long-term cost of a student loan depends heavily on the interest rate and the chosen repayment plan. A lower interest rate and shorter repayment period will result in lower overall interest costs. Conversely, a higher interest rate and longer repayment period will significantly increase the total amount repaid.

For example, a $30,000 loan with a 5% interest rate repaid over 10 years will cost considerably less in total than the same loan repaid over 25 years. The extended repayment plan will reduce the monthly payment but will increase the total interest paid by several thousand dollars. Income-driven repayment plans can provide short-term relief, but the extended repayment periods often result in higher overall costs.

Sample Repayment Schedule

The following table illustrates the impact of different interest rates and repayment plans on a $20,000 loan. These are simplified examples and do not account for all potential factors.

| Repayment Plan | Interest Rate | Loan Term (Years) | Approximate Monthly Payment | Approximate Total Interest Paid |

|---|---|---|---|---|

| Standard | 5% | 10 | $212 | $4,240 |

| Graduated | 5% | 10 | Starts at $150, increases gradually | $4,240 |

| Extended | 5% | 25 | $106 | $11,500 |

Note: These figures are estimates and actual amounts may vary. Consult with your lender for precise calculations.

Managing Student Loan Debt

Successfully navigating student loan debt requires proactive planning and responsible financial habits. Understanding your repayment options and developing effective budgeting strategies are crucial for minimizing financial stress and ensuring timely repayment. Ignoring your student loans can lead to serious consequences, impacting your credit score and future financial opportunities.

Strategies for Responsible Student Loan Debt Management

Effective student loan management begins with understanding your loan terms, including interest rates, repayment schedules, and any applicable fees. Prioritize creating a realistic budget that accounts for all your expenses, including loan payments. Consider exploring different repayment plans, such as income-driven repayment or extended repayment, to find one that aligns with your financial situation. Regularly monitor your loan balance and make consistent, on-time payments to avoid late fees and maintain a positive credit history. Additionally, explore opportunities to reduce your debt, such as refinancing at a lower interest rate if eligible. Finally, maintaining open communication with your loan servicer can help address any concerns or difficulties you may encounter.

Budgeting and Financial Planning for Students with Loan Debt

Creating a comprehensive budget is paramount for managing student loan debt. Start by listing all your monthly income and expenses. Categorize expenses into needs (housing, food, transportation) and wants (entertainment, dining out). Allocate a specific amount each month for your student loan payments. Track your spending to identify areas where you can cut back and reallocate funds towards debt repayment. Consider using budgeting apps or spreadsheets to monitor your progress and stay organized. Building an emergency fund can provide a safety net for unexpected expenses, preventing you from falling behind on loan payments. Regularly review and adjust your budget as your income or expenses change. For example, a student working part-time might allocate a portion of their earnings towards loan repayment and build a small emergency fund.

Consequences of Defaulting on Student Loans

Defaulting on student loans has severe financial repercussions. Your credit score will be significantly damaged, making it difficult to obtain loans, credit cards, or even rent an apartment in the future. Wage garnishment is a possibility, where a portion of your earnings is directly seized to repay the debt. Tax refunds can be withheld, and you may face legal action, including lawsuits and potential wage garnishment. Furthermore, defaulting can make it challenging to secure employment in certain fields or obtain professional licenses. The long-term consequences of default can severely impact your financial well-being for years to come. For example, a defaulted loan could lead to a significant drop in credit score, making it harder to qualify for a mortgage or car loan, even years after the default.

Resources and Tools for Effective Student Loan Debt Management

Several resources are available to help students manage their loan debt effectively. These resources can provide valuable guidance and support throughout the repayment process.

- National Student Loan Data System (NSLDS): Provides a central location to access information about your federal student loans.

- Your Loan Servicer: Contact your loan servicer directly for personalized assistance with repayment options and managing your account.

- Federal Student Aid Website (studentaid.gov): Offers comprehensive information on federal student loans, repayment plans, and debt management strategies.

- Consumer Financial Protection Bureau (CFPB): Provides resources and guidance on managing debt and avoiding predatory lending practices.

- Credit Counseling Agencies: Non-profit organizations that offer free or low-cost credit counseling and debt management services.

Alternatives to Bank Loans

Securing funding for higher education shouldn’t solely rely on bank loans. Several alternative financing options exist, each with its own set of advantages and disadvantages. Understanding these alternatives is crucial for students to make informed decisions about how to best finance their education. Careful consideration of the pros and cons, along with the application processes involved, can significantly impact a student’s financial well-being during and after their studies.

Scholarships

Scholarships are merit-based or need-based financial awards that don’t require repayment. They are often offered by universities, colleges, private organizations, and corporations. The selection process usually involves submitting an application, including academic transcripts, essays, and letters of recommendation. Successful applicants demonstrate academic excellence, exceptional talent, or financial need.

Grants

Similar to scholarships, grants are forms of financial aid that don’t need to be repaid. However, grants are typically awarded based on financial need, determined by the student’s and family’s financial situation. Federal and state governments, as well as private organizations, offer various grant programs. The application process generally involves completing the Free Application for Federal Student Aid (FAFSA) form, which assesses financial eligibility.

Work-Study Programs

Work-study programs offer part-time employment opportunities to students, allowing them to earn money to help cover educational expenses. These programs are often administered through the university or college and are usually based on financial need. Students are typically assigned jobs on campus or at affiliated organizations, with wages contributing to their educational costs. The application process typically involves completing the FAFSA form and indicating interest in the work-study program.

Comparison of Funding Options

The following table compares bank loans with the alternative funding options discussed above:

| Funding Option | Advantages | Disadvantages | Application Process |

|---|---|---|---|

| Bank Loan | Large sums available, flexible repayment options | Accumulates interest, requires repayment, impacts credit score | Credit check, application form, documentation of income and expenses |

| Scholarships | Free money, no repayment required | Competitive application process, limited availability | Application form, essays, transcripts, letters of recommendation |

| Grants | Free money, no repayment required | Based on financial need, limited availability, competitive | FAFSA completion, documentation of financial need |

| Work-Study | Earns income to offset costs, valuable work experience | Limited earnings potential, may impact study time | FAFSA completion, application through university/college |

Understanding Loan Terms and Conditions

Navigating the complexities of a student loan agreement requires a thorough understanding of its terms and conditions. Failing to grasp these details can lead to unexpected costs and financial difficulties down the line. This section clarifies key terms and their implications, empowering you to make informed decisions.

Student loan agreements contain a variety of terms that significantly impact the overall cost and repayment of your loan. Understanding these terms is crucial to avoid unforeseen financial burdens. Key terms include the Annual Percentage Rate (APR), various fees, deferment and forbearance options, and the overall repayment plan structure.

Annual Percentage Rate (APR)

The APR represents the annual cost of borrowing money, expressed as a percentage. It includes the interest rate plus any other fees charged by the lender. A higher APR means you’ll pay more in interest over the life of the loan. For example, a loan with a 7% APR will cost significantly less in interest over 10 years than a loan with a 10% APR, assuming all other factors remain equal. Understanding the APR is vital for comparing different loan offers and selecting the most cost-effective option.

Fees Associated with Student Loans

Several fees can be associated with student loans, including origination fees, late payment fees, and prepayment penalties. Origination fees are charged by the lender at the time the loan is disbursed and are typically a percentage of the loan amount. Late payment fees are charged if you miss a payment, while prepayment penalties are assessed if you pay off the loan early. These fees can significantly increase the total cost of the loan, so it’s essential to understand what fees apply and how they are calculated. A loan with a 1% origination fee on a $10,000 loan adds $100 to the initial loan amount.

Deferment and Forbearance

Deferment and forbearance are options that allow borrowers to temporarily postpone or reduce their loan payments. Deferment typically applies to specific situations, such as returning to school or experiencing unemployment, and often involves no interest accrual during the deferment period. Forbearance, on the other hand, is a more general option that allows borrowers to temporarily reduce or suspend their payments, though interest usually continues to accrue during this period. The availability and terms of deferment and forbearance vary depending on the lender and the type of loan. A borrower facing temporary financial hardship might choose forbearance to avoid default, though it will result in a larger total loan repayment amount due to accrued interest.

Repayment Plans

Different repayment plans are available, each with its own terms and conditions. Standard repayment plans typically require fixed monthly payments over a set period (e.g., 10 years). Income-driven repayment plans adjust monthly payments based on income and family size, potentially resulting in lower monthly payments but a longer repayment period and increased total interest paid. Choosing the right repayment plan depends on your individual financial situation and long-term goals. For example, a standard repayment plan might offer lower total interest paid but higher monthly payments compared to an income-driven plan.

Interpreting a Sample Loan Agreement

A sample loan agreement would typically include a detailed breakdown of the loan amount, APR, fees, repayment schedule, and other terms and conditions. It is crucial to carefully review the entire agreement before signing, paying close attention to the details of the interest rate, any fees, and the repayment plan. Any unclear or confusing aspects should be clarified with the lender before accepting the loan. For example, a sample loan agreement might specify a 6% APR, a $100 origination fee, a 10-year repayment term, and monthly payments of $100. Understanding each of these components is critical to responsible borrowing.

The Impact of Student Loans on Future Finances

Student loan debt can significantly influence your financial trajectory for years, even decades, after graduation. Understanding the long-term implications is crucial for making informed borrowing decisions and developing effective repayment strategies. Failing to plan can lead to considerable financial strain and limit opportunities.

Student loan debt’s impact extends beyond simply repaying the principal and interest. It affects your credit score, your ability to secure future loans (like mortgages or auto loans), and your overall financial well-being. Careful consideration of borrowing amounts, repayment plans, and potential long-term consequences is essential.

Credit Score Impact

Student loan debt directly impacts your credit score. Consistent on-time payments demonstrate responsible borrowing behavior, positively affecting your score. Conversely, missed or late payments can severely damage your credit, making it harder to obtain loans or credit cards in the future with favorable terms. A lower credit score can also translate to higher interest rates on future borrowing, increasing the overall cost of credit. For instance, a person with a low credit score might face an interest rate of 8% on a mortgage, compared to 4% for someone with excellent credit. This difference can amount to tens of thousands of dollars over the life of the loan.

Future Borrowing Capacity

Your student loan debt affects your debt-to-income ratio (DTI), a crucial factor lenders consider when evaluating loan applications. A high DTI, resulting from substantial student loan payments, can reduce your chances of securing a mortgage, auto loan, or other significant loans. Lenders view a high DTI as a higher risk, making them less likely to approve your application, or offering less favorable terms if they do. For example, someone with a high DTI might be denied a mortgage, or might only qualify for a smaller loan amount than someone with a lower DTI.

Strategies for Minimizing Long-Term Impact

Several strategies can mitigate the long-term effects of student loan debt. Borrowing only what’s necessary for education, exploring scholarships and grants to reduce loan dependence, and choosing a repayment plan aligned with your post-graduation income are crucial steps. Prioritizing repayment, even small amounts, early on, can save significant money on interest over time. Furthermore, regularly monitoring your credit report and addressing any errors promptly is essential to maintain a good credit score.

Hypothetical Scenario: Long-Term Effects of Borrowing and Repayment

Let’s consider two hypothetical graduates, both pursuing the same degree. Graduate A borrows $50,000 with a 6% interest rate and a standard 10-year repayment plan. Graduate B borrows $100,000 with the same interest rate and repayment plan. Over 10 years, Graduate A will pay significantly less in total interest compared to Graduate B. Graduate A’s higher monthly payment initially may seem daunting, but it leads to substantial long-term savings. Graduate B will face a much larger monthly payment, and the total interest paid will be significantly higher, potentially impacting their ability to save for a down payment on a house, retirement, or other financial goals. The difference in total interest paid could easily exceed $20,000, highlighting the importance of responsible borrowing and strategic repayment planning.

Summary

Securing a bank loan for your education is a significant decision, but with careful planning and a thorough understanding of the available options, you can navigate the process successfully. Remember to compare different loan types, carefully review loan agreements, and develop a robust repayment strategy. By proactively managing your student loan debt and exploring alternative funding sources, you can minimize the long-term financial impact and focus on your academic pursuits with greater peace of mind. Ultimately, responsible borrowing allows you to invest in your future, unlocking opportunities for personal and professional growth.

Query Resolution

What happens if I can’t repay my student loan?

Defaulting on a student loan can have severe consequences, including damage to your credit score, wage garnishment, and potential legal action. Contact your lender immediately if you anticipate difficulties in repayment to explore options like deferment or forbearance.

Can I refinance my student loans?

Yes, refinancing can potentially lower your interest rate and monthly payments. However, it’s crucial to compare offers from multiple lenders and understand the terms and conditions before refinancing.

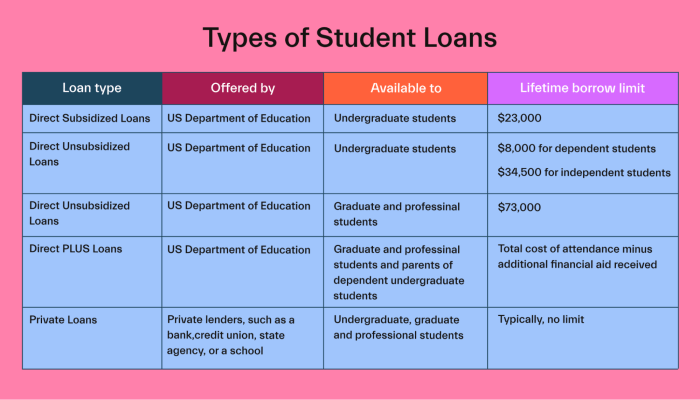

What is the difference between subsidized and unsubsidized loans?

Subsidized loans don’t accrue interest while you’re in school, whereas unsubsidized loans do. Subsidized loans typically require greater financial need demonstration.

How long does the loan application process take?

The application process varies depending on the lender and the type of loan. It can range from a few weeks to several months. It’s best to start the application process well in advance of your needed funds.