Navigating the complex world of undergraduate student loans can feel overwhelming. The sheer number of options, varying interest rates, and repayment plans often leave prospective students feeling lost. This guide aims to demystify the process, providing a clear and concise overview of federal and private student loans, helping you make informed decisions about financing your education.

From understanding the nuances of FAFSA applications to comparing the pros and cons of different loan types and lenders, we’ll equip you with the knowledge necessary to secure the best possible financing for your undergraduate studies. We’ll also explore alternative funding sources and strategies for effective debt management, empowering you to confidently plan for your financial future.

Factors Influencing Loan Selection

Choosing the right student loan is crucial for managing your finances during and after your undergraduate studies. Several key factors significantly impact the loan terms you’ll receive and the overall cost of borrowing. Understanding these factors empowers you to make informed decisions and secure the most favorable loan options available.

Credit Score and Credit History’s Influence on Loan Terms

A strong credit score and positive credit history are paramount in obtaining favorable student loan terms. Lenders assess your creditworthiness to determine the risk associated with lending you money. A higher credit score typically translates to lower interest rates, more favorable repayment terms, and potentially even access to larger loan amounts. Conversely, a poor credit history might result in higher interest rates, less flexible repayment options, or even loan denial. Building a good credit history before applying for student loans, even through small credit accounts managed responsibly, can significantly benefit your application. For example, a student with a credit score above 750 might qualify for a loan with a 4% interest rate, while a student with a score below 600 might face an interest rate exceeding 10%. This substantial difference in interest rates can significantly impact the total cost of the loan over its repayment period.

Undergraduate Program Cost and Student’s Financial Situation

The cost of your undergraduate program directly influences the amount of student loan funding you’ll need. Similarly, your current financial situation, including existing debts and income, plays a critical role in loan selection. Students attending expensive private universities may require larger loan amounts compared to those attending state-funded institutions. Your ability to contribute to the cost of education from savings, part-time jobs, or family contributions also affects your borrowing needs. For instance, a student with significant savings and part-time income might need a smaller loan, allowing them to focus on loans with lower interest rates but potentially stricter eligibility requirements. Conversely, a student with limited financial resources might need to consider loans with more lenient eligibility criteria, even if they come with higher interest rates.

Key Factors in Comparing Loan Offers

When comparing loan offers, several key aspects should be carefully considered. These include the interest rate (fixed vs. variable), loan fees, repayment terms (length and options), grace period, deferment and forbearance options, and the lender’s reputation and customer service. A lower interest rate will reduce the total cost of the loan, while flexible repayment options offer more financial flexibility. A longer repayment period lowers monthly payments but increases the total interest paid. Understanding all aspects of the loan agreement is vital to selecting the most suitable option. For example, one loan might offer a lower interest rate but charge higher fees, while another might have a higher interest rate but more flexible repayment options. A thorough comparison helps you determine which loan best suits your individual circumstances and financial goals.

Steps to Effectively Compare Loan Options

Before making a decision, it’s crucial to systematically compare different loan options.

- Gather Information: Collect details on interest rates, fees, repayment terms, and other relevant information from multiple lenders.

- Use a Loan Comparison Tool: Utilize online tools or spreadsheets to compare loan offers side-by-side.

- Read the Fine Print: Carefully review all loan documents to understand the terms and conditions.

- Consider Your Financial Situation: Assess your ability to repay the loan based on your income and expenses.

- Seek Professional Advice: Consult a financial advisor for personalized guidance.

Federal Student Loan Programs

Federal student loans offer a crucial pathway to higher education for many students. Understanding the application process, repayment options, and the nuances of different loan types is essential for making informed financial decisions. This section details the key aspects of federal student loan programs.

Federal Student Loan Application Process

The primary application for federal student aid is the Free Application for Federal Student Aid (FAFSA). This form collects information about your financial situation, including your income, assets, and family size. The information provided on the FAFSA determines your eligibility for federal grants, loans, and work-study programs. The application process involves creating an FSA ID, gathering necessary financial documents, and accurately completing the online form. After submission, the FAFSA data is processed, and your school receives your Student Aid Report (SAR), outlining your eligibility for federal aid. You will then be notified by your school regarding your financial aid package, which may include federal student loans.

Federal Student Loan Repayment Plans

Several repayment plans are available for federal student loans, each tailored to different financial situations. The Standard Repayment Plan involves fixed monthly payments over a 10-year period. The Graduated Repayment Plan starts with lower monthly payments that gradually increase over time. Income-Driven Repayment (IDR) Plans, such as the Income-Based Repayment (IBR), Pay As You Earn (PAYE), and Revised Pay As You Earn (REPAYE) plans, base your monthly payments on your income and family size. These plans often result in longer repayment periods but lower monthly payments. Choosing the right plan depends on your individual financial circumstances and long-term goals. For example, a recent graduate with a low income might benefit from an IDR plan, while someone with a higher income might prefer the Standard Repayment Plan to pay off their loans faster.

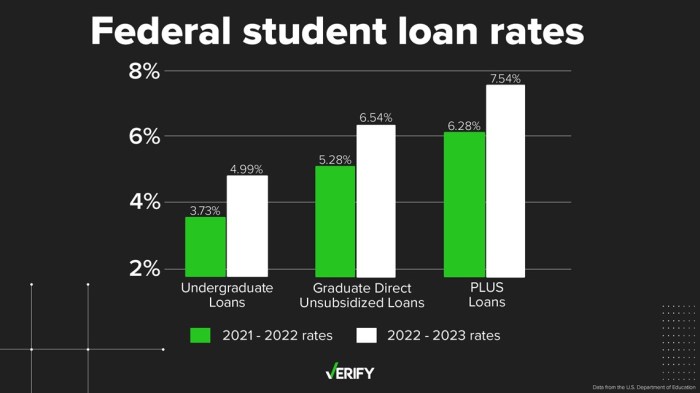

Subsidized vs. Unsubsidized Federal Student Loans

Subsidized and unsubsidized federal student loans differ primarily in how interest accrues. With subsidized loans, the government pays the interest while you are in school at least half-time, during grace periods, and during periods of deferment. Unsubsidized loans, however, accrue interest from the time the loan is disbursed, regardless of your enrollment status. This means that with unsubsidized loans, the total amount you owe will be higher than the initial loan amount due to accumulated interest. Therefore, while both types of loans offer financial assistance, subsidized loans are generally more advantageous for students who are still enrolled in school and have limited financial resources. For example, a student pursuing a four-year degree might find subsidized loans significantly reduce their overall debt burden compared to using only unsubsidized loans.

Private Student Loan Options

Private student loans offer an alternative funding source for higher education, supplementing federal loans or covering expenses not met by federal aid. Understanding their nuances is crucial for responsible borrowing. They are offered by various private lenders, including banks, credit unions, and online lenders, each with its own set of terms and conditions.

Features and Benefits of Private Student Loans

Private student loans can offer several advantages, such as potentially higher loan amounts than federal loans, allowing students to cover more of their educational costs. Some lenders may offer flexible repayment options, such as variable interest rates that could potentially decrease over time, or the ability to defer payments during periods of unemployment or financial hardship. However, it’s vital to remember that these benefits are contingent upon individual lender policies and borrower qualifications. It is important to compare multiple offers to find the most suitable loan.

Terms and Conditions of Private Student Loan Agreements

Understanding the terms and conditions of a private student loan agreement is paramount. This includes scrutinizing the interest rate (fixed or variable), fees (origination, late payment, etc.), repayment schedule (length, payment amount), and any prepayment penalties. A thorough review of the loan contract before signing prevents unexpected financial burdens. Borrowers should pay close attention to the APR (Annual Percentage Rate), which reflects the total cost of borrowing including fees. Failure to understand these terms could lead to unforeseen financial difficulties.

Potential Risks and Drawbacks of Private Student Loans

Private student loans carry inherent risks. Higher interest rates compared to federal loans can significantly increase the overall cost of borrowing. The absence of federal protections, such as income-driven repayment plans or loan forgiveness programs, exposes borrowers to greater financial vulnerability if they encounter unexpected financial hardship. Furthermore, private lenders may require a co-signer with good credit, limiting access for students without a creditworthy co-signer. Defaulting on a private student loan can severely damage credit scores, impacting future borrowing opportunities.

Comparison of Private Student Loan Lenders

The following table provides a sample comparison of private student loan lenders. Note that interest rates and repayment options are subject to change and are based on a hypothetical scenario for illustrative purposes. Actual rates and options will vary depending on individual creditworthiness and lender policies. Always check with the lender directly for the most up-to-date information.

| Lender | Interest Rate (Example – Variable) | Repayment Options | Other Features |

|---|---|---|---|

| Lender A | 6.5% – 10.5% | Standard, Graduated, Extended | Co-signer options available, potential for autopay discounts |

| Lender B | 7% – 11% | Standard, Income-Based (specific criteria apply) | Online application process, competitive rates for high credit scores |

| Lender C | 8% – 12% | Standard, Deferred Payment Options (specific criteria apply) | Focus on students pursuing specific fields, potential for scholarships |

| Lender D | 6.0% – 9.0% | Standard, Accelerated repayment | Loyalty programs for existing customers |

Managing Student Loan Debt

Successfully navigating student loan repayment requires proactive planning and consistent effort. Understanding your loan terms, budgeting effectively, and establishing a realistic repayment strategy are crucial for minimizing financial strain and avoiding potential long-term consequences. This section Artikels practical strategies for managing your student loan debt effectively.

Budgeting and Repayment Strategies

Effective budgeting is paramount to successful student loan repayment. Begin by creating a detailed budget that tracks all income and expenses. Categorize your expenses to identify areas where you can reduce spending and allocate more funds towards loan payments. Consider using budgeting apps or spreadsheets to simplify the process. Prioritize essential expenses like housing, food, and transportation, then allocate remaining funds towards your student loans. Explore different repayment methods offered by your lender, such as graduated repayment (lower payments initially, increasing over time) or income-driven repayment (payments based on your income and family size). These options can offer flexibility and prevent financial hardship. Remember to account for unexpected expenses in your budget to avoid falling behind on payments.

Importance of a Repayment Plan

Creating and adhering to a comprehensive repayment plan is vital for successful debt management. A well-defined plan Artikels your repayment strategy, including the chosen repayment method, payment amount, and payment due dates. This structured approach helps you stay organized, track your progress, and avoid missed payments. Regularly review and adjust your plan as needed, considering changes in income or expenses. Consider setting up automatic payments to ensure consistent repayments and avoid late fees. Maintaining a clear repayment plan minimizes stress and promotes financial stability. Failing to plan often results in missed payments and accumulating interest, ultimately increasing the total amount owed.

Consequences of Defaulting on Student Loan Payments

Defaulting on student loans has severe financial and legal ramifications. Default occurs when you fail to make payments for a specific period (typically 90 days). Consequences include damaged credit score, wage garnishment (a portion of your wages is seized to pay the debt), tax refund offset (your tax refund is used to pay the debt), and difficulty obtaining future loans or credit. Furthermore, default can negatively impact your ability to rent an apartment, secure a job, or even obtain professional licenses in some fields. The long-term financial implications of default are substantial and can significantly hinder your future financial well-being. In some cases, default may even lead to legal action.

Managing Repayment Difficulties

Facing challenges in repaying your student loans is not uncommon. Proactive measures can help mitigate difficulties and prevent default.

Exploring Alternative Funding Options

Securing funding for undergraduate education often extends beyond student loans. A diverse range of alternative funding sources can significantly reduce reliance on borrowed money and lessen the burden of future debt repayment. Exploring these options diligently can lead to substantial savings and a more manageable financial path through college.

Scholarships

Scholarships represent a form of financial aid that doesn’t require repayment. They are typically awarded based on merit, academic achievement, athletic ability, or demonstrated financial need. Many scholarships are offered by colleges and universities themselves, while others come from private organizations, corporations, and even community groups. A successful scholarship search requires careful research and strategic application.

Grants

Similar to scholarships, grants are forms of financial aid that don’t need to be repaid. However, grants are generally awarded based on demonstrated financial need, assessed through the Free Application for Federal Student Aid (FAFSA). Federal, state, and institutional grants exist, offering various amounts depending on individual circumstances and eligibility criteria. The FAFSA is a crucial tool for accessing many grant opportunities.

Work-Study Programs

Work-study programs offer part-time employment opportunities to students who demonstrate financial need. These jobs are often campus-based, providing flexible schedules to accommodate academic demands. Earnings from work-study can directly contribute to educational expenses, reducing the need for loans or other forms of borrowing. The availability of work-study positions varies between institutions.

Advantages and Disadvantages of Alternative Funding Options

The following table summarizes the key advantages and disadvantages of each alternative funding option:

| Funding Option | Advantages | Disadvantages |

|---|---|---|

| Scholarships | Free money; no repayment required; can be substantial; many opportunities exist. | Competitive; requires effort in research and application; eligibility criteria may be restrictive. |

| Grants | Free money; no repayment required; based on financial need; accessible through FAFSA. | Competitive; based on financial need; amount may not fully cover expenses. |

| Work-Study | Earned income; flexible schedule; can contribute to educational expenses; valuable work experience. | Limited earnings potential; may impact study time; availability depends on institutional programs. |

Researching and Applying for Scholarships and Grants

Effectively researching and applying for scholarships and grants involves a systematic approach. Begin by identifying potential sources through online databases, college financial aid offices, and professional organizations related to your field of study. Carefully review eligibility requirements and deadlines for each opportunity. Prepare strong applications, showcasing your qualifications and achievements. Seek feedback on your application materials before submission. Following up on applications is crucial, as it demonstrates your genuine interest.

Resources for Finding Alternative Funding Opportunities

Finding alternative funding opportunities requires diligent research. Here are some valuable resources:

- FAFSA (Free Application for Federal Student Aid): The primary gateway to federal grants and work-study. The FAFSA website provides detailed information and application instructions.

- College Financial Aid Offices: Each college and university has a financial aid office that can provide personalized guidance and information on scholarships, grants, and work-study programs specific to the institution.

- Fastweb, Scholarships.com, Peterson’s: These are popular online scholarship search engines that allow students to filter opportunities based on criteria such as major, GPA, and demographics.

- Professional Organizations: Many professional organizations offer scholarships to students pursuing careers in their respective fields.

- State and Local Governments: State and local governments often offer grants and scholarships to residents.

The Role of Financial Aid Counseling

Navigating the complex world of student loans and financial aid can be daunting for students and their families. A professional financial aid counselor provides invaluable guidance, helping students make informed decisions that minimize debt and maximize their educational opportunities. Their expertise can significantly impact a student’s financial well-being throughout their college career and beyond.

The benefits of seeking professional financial aid advice are numerous and far-reaching. A counselor can simplify the often-overwhelming application process, identify all available funding sources, and assist in strategizing a comprehensive financial plan for college. This proactive approach can lead to significant savings and reduce the stress associated with managing student loan debt. Moreover, a counselor can provide crucial insights into long-term financial planning, helping students build a solid foundation for their post-graduate financial future.

Services Offered by Financial Aid Counselors

Financial aid counselors offer a wide range of services designed to support students in their financial planning for higher education. These services typically include assistance with completing the Free Application for Federal Student Aid (FAFSA), exploring federal and private loan options, understanding grant and scholarship opportunities, and developing a personalized budget. Counselors also help students compare loan terms and interest rates, guiding them towards the most financially advantageous options. Furthermore, they provide valuable advice on managing debt after graduation, including repayment strategies and consolidation options. Many counselors offer workshops and seminars on financial literacy, equipping students with the knowledge and skills to manage their finances effectively.

Finding and Selecting a Qualified Financial Aid Counselor

Identifying a qualified financial aid counselor requires careful consideration and research. Several avenues exist for finding reputable professionals. Many colleges and universities employ their own financial aid offices staffed with experienced counselors readily available to their students. Alternatively, independent financial aid counselors can be found through professional organizations or online directories. When selecting a counselor, it’s crucial to verify their credentials and experience. Look for counselors with certifications or affiliations with reputable organizations, and check online reviews and testimonials from previous clients. A consultation is often offered, allowing prospective clients to assess the counselor’s expertise and suitability to their individual needs before committing to their services. It’s also wise to inquire about their fee structure and payment options to ensure transparency and affordability.

Closure

Securing funding for your undergraduate education is a crucial step towards achieving your academic goals. By carefully considering the information presented in this guide – from understanding the differences between federal and private loans to exploring alternative funding options and developing a sound repayment strategy – you can navigate the complexities of student loan financing with confidence. Remember, proactive planning and informed decision-making are key to a successful and financially responsible educational journey.

Frequently Asked Questions

What is the difference between subsidized and unsubsidized federal loans?

Subsidized loans don’t accrue interest while you’re in school, grace periods, or during deferment. Unsubsidized loans accrue interest from the time the loan is disbursed.

Can I refinance my student loans?

Yes, refinancing can potentially lower your interest rate and monthly payments. However, it often involves replacing federal loans with private loans, potentially losing federal protections.

What happens if I default on my student loans?

Defaulting can severely damage your credit score, leading to wage garnishment, tax refund offset, and difficulty obtaining future loans or credit.

How long does it take to receive student loan funds?

Disbursement times vary depending on the lender and the school’s processing time. It can take several weeks or even months.

What is a co-signer, and why might I need one?

A co-signer is someone who agrees to repay your loan if you cannot. Lenders often require co-signers for students with limited or no credit history.