Navigating the complexities of higher education financing often leaves students and families grappling with substantial student loan debt. While 529 plans are designed for educational expenses, many wonder if they can be leveraged to alleviate the burden of student loan repayments. This guide delves into the intricacies of using 529 funds for non-qualified expenses like student loan payoff, exploring the potential benefits, drawbacks, and crucial legal and tax implications. We’ll examine the circumstances under which this strategy might be advantageous, and when alternative approaches might be more financially sound.

Understanding the tax advantages of 529 plans, the various student loan repayment options, and the penalties associated with using 529 funds for non-educational purposes are key to making an informed decision. We’ll compare 529 plans to other savings vehicles and discuss alternative student loan repayment strategies, helping you determine the best course of action for your specific financial situation.

529 Plan Basics

529 plans are tax-advantaged savings plans designed to encourage saving for future higher education expenses. These plans offer significant benefits to families aiming to fund college or other qualified education costs, making them a popular choice for long-term educational savings. Understanding the mechanics and advantages of 529 plans is crucial for maximizing their potential.

Purpose and Tax Advantages of 529 Plans

The primary purpose of a 529 plan is to provide a tax-advantaged vehicle for saving for qualified education expenses. These expenses include tuition, fees, books, supplies, and even room and board, under certain circumstances. The key tax advantage lies in the fact that earnings grow tax-deferred, meaning you don’t pay taxes on investment gains until the money is withdrawn for qualified education expenses. Furthermore, withdrawals used for qualified education expenses are generally tax-free at the federal level. This combination of tax-deferred growth and tax-free withdrawals significantly boosts the potential returns of your savings. State tax benefits also vary, with some states offering deductions or credits for contributions.

Eligibility Requirements for 529 Plan Beneficiaries

Anyone can contribute to a 529 plan, regardless of income or the beneficiary’s age. The beneficiary can be a child, grandchild, or even yourself. Importantly, the beneficiary can be changed at any time, offering flexibility should circumstances change. There are no income limitations for contributions, though there may be annual contribution limits set by each state. A single beneficiary can have multiple 529 plans open at the same time. It’s important to note that while there are no restrictions based on the beneficiary’s academic performance or intended field of study, the funds must be used for qualified education expenses to avoid tax penalties.

Types of 529 Plans and Investment Options

529 plans are offered by states, and each state typically offers its own plan or plans. There are two main types: state-sponsored plans and private plans. State-sponsored plans are generally managed by the state’s government or a designated investment firm, while private plans are offered by financial institutions. Investment options vary widely depending on the plan. Many offer a range of choices, from age-based portfolios that automatically adjust asset allocation as the beneficiary gets closer to college, to more hands-on options that allow for individual stock selection or investment in mutual funds. Investors can choose options based on their risk tolerance and investment goals. For example, a conservative investor might opt for a plan with a higher allocation to bonds, while a more aggressive investor might choose one with a higher allocation to stocks.

Comparison of Tax Benefits: 529 Plans vs. Other Savings Vehicles

| Feature | 529 Plan | Roth IRA | Traditional IRA |

|---|---|---|---|

| Tax-Deferred Growth | Yes | Yes | Yes |

| Tax-Free Withdrawals (for qualified expenses) | Yes | Yes (for qualified withdrawals) | No (taxed as ordinary income) |

| Contribution Limits | Varies by state | $6,500 (2023) | $6,500 (2023) |

| Early Withdrawal Penalties | Yes (for non-qualified withdrawals) | Yes (for non-qualified withdrawals) | Yes (for non-qualified withdrawals) |

Student Loan Repayment Options

Navigating the complexities of student loan repayment can feel daunting, but understanding the available options and their implications is crucial for effective financial planning. Choosing the right repayment plan depends on your individual circumstances, including your income, loan amount, and financial goals. This section explores various repayment plans and factors to consider when developing a repayment strategy.

Student loan repayment plans offer different approaches to managing debt, each with its own set of advantages and disadvantages. The most common plans include Standard Repayment, Extended Repayment, Graduated Repayment, and Income-Driven Repayment (IDR) plans. Refinancing is another option that can potentially lower monthly payments or shorten the repayment term.

Standard Repayment Plan

The Standard Repayment Plan is a fixed monthly payment plan typically spread over 10 years. This plan offers the shortest repayment period, resulting in less interest paid overall. However, the fixed monthly payments may be higher than other plans, potentially making it challenging for borrowers with limited income.

Extended Repayment Plan

The Extended Repayment Plan extends the repayment period to up to 25 years. This significantly lowers the monthly payment amount compared to the Standard Repayment Plan, making it more manageable for borrowers with lower incomes. However, it results in paying significantly more interest over the life of the loan.

Graduated Repayment Plan

The Graduated Repayment Plan starts with lower monthly payments that gradually increase over time. This can be beneficial for borrowers who anticipate increased income in the future. However, the increasing payments may become burdensome later in the repayment period.

Income-Driven Repayment (IDR) Plans

IDR plans, such as Income-Based Repayment (IBR), Pay As You Earn (PAYE), and Revised Pay As You Earn (REPAYE), tie your monthly payments to your income and family size. These plans offer lower monthly payments, potentially making them more affordable for borrowers with lower incomes. However, they often extend the repayment period, resulting in higher total interest paid over the life of the loan. Furthermore, remaining balances after 20 or 25 years may be forgiven, but this forgiveness is considered taxable income.

Factors Influencing Student Loan Repayment Strategies

Several factors influence the selection of a suitable repayment strategy. These include the borrower’s income, loan amount, interest rate, and financial goals. For instance, a borrower with a high income might prefer a Standard Repayment Plan to minimize interest paid, while a borrower with a low income might opt for an IDR plan to manage monthly payments.

Refinancing Student Loans: Beneficial Scenarios

Refinancing student loans can be advantageous in specific scenarios. For example, borrowers with good credit scores might secure a lower interest rate through refinancing, leading to lower monthly payments and reduced overall interest paid. Refinancing can also consolidate multiple loans into a single loan, simplifying repayment management. However, refinancing may extend the repayment term, potentially increasing the total interest paid if the new interest rate isn’t significantly lower. Consider refinancing if you can obtain a significantly lower interest rate than your current loans, especially if you have excellent credit.

Comparison of Repayment Plans

| Repayment Plan | Monthly Payment | Repayment Term | Total Interest Paid |

|---|---|---|---|

| Standard Repayment | High | 10 years | Low |

| Extended Repayment | Low | Up to 25 years | High |

| Graduated Repayment | Low initially, increasing over time | 10 years | Moderate |

| Income-Driven Repayment | Variable, based on income | Up to 20-25 years | High |

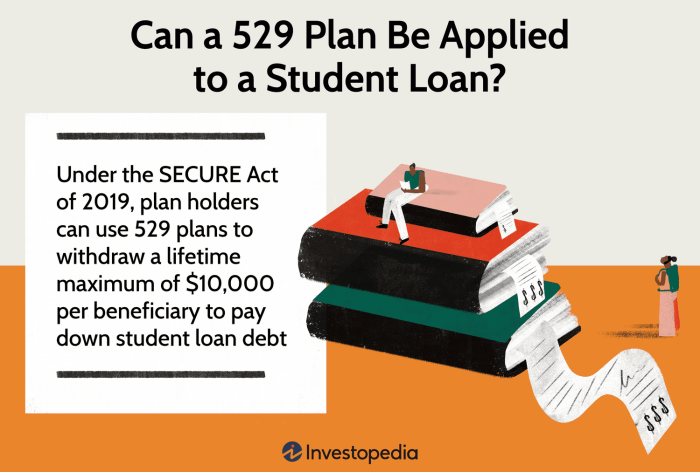

Using 529 Funds for Non-Qualified Expenses

Using 529 plan funds for anything other than qualified education expenses incurs tax penalties. While the primary purpose of a 529 plan is to save for higher education, understanding the implications of using these funds for non-qualified expenses is crucial for informed financial planning. This section will Artikel the penalties, circumstances where non-qualified withdrawals might be considered, and examples of situations where the benefits might outweigh the costs.

Penalties for Non-Qualified Withdrawals

Distributions from a 529 plan used for non-qualified expenses are subject to income tax on the earnings portion, plus a 10% penalty. This means that only the original contributions are penalty-free; any investment earnings are taxed and penalized. For example, if $10,000 was contributed to a 529 plan and grew to $15,000, a non-qualified withdrawal of the entire amount would result in income tax on the $5,000 in earnings, plus a $500 penalty (10% of $5,000). This can significantly reduce the overall benefit of the investment. Careful consideration should be given before using 529 funds for anything other than qualified education expenses.

Circumstances Where Non-Qualified Withdrawals Might Be Considered

While generally discouraged, there are rare circumstances where using 529 funds for non-qualified expenses might be deemed necessary or advantageous. This often involves a significant change in circumstances that alters the original educational plans, making the funds unusable for their intended purpose. For example, a beneficiary might decide not to pursue higher education, or the funds might be needed for an unforeseen emergency.

Examples of Advantageous Non-Qualified Withdrawals Despite Penalties

Although penalties apply, there are exceptional cases where the financial benefit of using 529 funds for non-qualified expenses outweighs the penalties. Consider a scenario where a student faces a catastrophic illness requiring substantial medical expenses. Using the 529 funds, even with the penalty, might be less financially burdensome than other borrowing options. Similarly, if a severe economic downturn affects the family’s financial stability, accessing the 529 funds might be a more favorable option than depleting other savings or taking on high-interest debt. The decision requires careful evaluation of the specific circumstances and financial implications.

Potential Non-Qualified Expenses and Associated Tax Implications

The following list Artikels potential non-qualified expenses and their tax consequences. It is crucial to consult with a financial advisor or tax professional for personalized guidance.

- Non-Qualified Expense: Purchase of a home. Tax Implications: Income tax on earnings portion, plus 10% penalty.

- Non-Qualified Expense: Business startup costs. Tax Implications: Income tax on earnings portion, plus 10% penalty.

- Non-Qualified Expense: Medical expenses (unrelated to a qualified disability). Tax Implications: Income tax on earnings portion, plus 10% penalty. (Note: Some medical expenses *may* be deductible on federal income taxes, but this is separate from the 529 penalty.)

- Non-Qualified Expense: Purchase of a vehicle. Tax Implications: Income tax on earnings portion, plus 10% penalty.

Alternatives to Using 529 Funds for Student Loans

While 529 plans offer tax advantages for education expenses, using them to pay off student loans isn’t always the most financially sound strategy. Exploring alternative repayment methods and understanding their implications is crucial for effective debt management. This section will Artikel several approaches to student loan repayment, comparing their benefits and drawbacks to help you make informed decisions.

Student Loan Repayment Methods: A Comparison

Several strategies exist for repaying student loans, each with its own set of advantages and disadvantages. Choosing the right method depends on individual financial circumstances, loan types, and long-term goals.

| Repayment Plan | Description | Benefits | Drawbacks |

|---|---|---|---|

| Standard Repayment | Fixed monthly payments over 10 years. | Predictable payments, faster loan payoff. | Higher monthly payments, may be difficult for some borrowers. |

| Graduated Repayment | Payments start low and gradually increase over time. | Lower initial payments, easier to manage initially. | Payments become significantly higher later, potentially causing financial strain. |

| Extended Repayment | Longer repayment period (up to 25 years). | Lower monthly payments. | Higher total interest paid over the life of the loan. |

| Income-Driven Repayment (IDR) | Monthly payments based on income and family size. | Affordable monthly payments, potential for loan forgiveness. | Longer repayment period, may not be suitable for high earners. |

Income-Driven Repayment Plans: Benefits and Drawbacks

Income-driven repayment (IDR) plans, such as Income-Based Repayment (IBR), Pay As You Earn (PAYE), and Revised Pay As You Earn (REPAYE), adjust monthly payments based on your discretionary income and family size.

- Benefit: Affordability. Payments are significantly lower than standard repayment, making them manageable for borrowers with lower incomes.

- Benefit: Potential for Loan Forgiveness. After making payments for a specified period (usually 20-25 years), remaining loan balances may be forgiven. This is a significant advantage, effectively eliminating a substantial debt.

- Drawback: Longer Repayment Period. IDR plans typically extend repayment periods significantly, leading to higher overall interest payments.

- Drawback: Tax Implications. Forgiven loan amounts may be considered taxable income, potentially resulting in a tax liability upon forgiveness.

For example, a borrower with a $50,000 loan might see their monthly payment reduced from $500 under a standard plan to $200 under an IDR plan. However, they would end up paying significantly more in interest over the extended repayment period.

Loan Forgiveness Programs: Impact on Repayment Strategies

Several federal loan forgiveness programs exist, including those tied to public service employment and IDR plans. These programs can significantly reduce or eliminate student loan debt.

- Impact: These programs incentivize borrowers to pursue careers in public service or utilize IDR plans, potentially offering substantial long-term savings.

- Impact: The existence of these programs influences repayment strategy. Borrowers might prioritize IDR plans to maximize their chances of loan forgiveness, even if it means paying more interest in the short term.

- Impact: However, it’s important to understand the eligibility criteria and potential tax implications of loan forgiveness programs before relying on them as the primary repayment strategy.

Decision-Making Flowchart for Choosing a Student Loan Repayment Method

The flowchart below visually represents the decision-making process for selecting a suitable student loan repayment plan.

[Imagine a flowchart here. The flowchart would start with a box: “Assess your financial situation (income, expenses, debt)”. This would branch to two boxes: “High Income/Low Debt” and “Low Income/High Debt”. The “High Income/Low Debt” box would branch to “Standard Repayment” and possibly “Graduated Repayment”. The “Low Income/High Debt” box would branch to “Income-Driven Repayment” and “Extended Repayment”. Each repayment option would then have a box detailing its pros and cons, potentially leading to a final box: “Choose Repayment Plan”.]

Legal and Tax Implications

Using 529 funds for non-qualified expenses carries significant legal and tax ramifications for both the account owner and the beneficiary. Understanding these implications is crucial before diverting these funds from their intended purpose of education expenses. Improper use can lead to penalties and taxes, potentially negating any perceived financial benefit.

Tax Implications for Non-Qualified Withdrawals

When 529 plan funds are withdrawn for non-qualified expenses, the earnings portion of the withdrawal is subject to income tax at the beneficiary’s tax rate, plus a 10% penalty. This means that only the original contributions are tax-free. For example, if $10,000 is withdrawn, and $2,000 represents the original contributions, then $8,000 (the earnings) will be taxed as ordinary income, and a further $800 (10% of the earnings) will be assessed as a penalty. This can significantly reduce the net amount received and impact the beneficiary’s overall tax liability. The tax implications are determined at the time of withdrawal and reported on the beneficiary’s tax return.

Tax Implications for Account Owner

While the primary tax burden falls on the beneficiary, the account owner also has responsibilities. The owner is responsible for accurately reporting the distribution on the appropriate tax forms. Failure to do so can result in penalties for the account owner as well. Accurate record-keeping is paramount to avoid discrepancies and potential audits. This includes maintaining records of contributions, earnings, and withdrawals.

Examples of Tax Law Impact

Consider a scenario where a student has accumulated $20,000 in 529 plan earnings. If they withdraw this amount to pay off student loans, they will owe income tax on the entire $20,000 plus a 10% penalty, totaling $4,000. This contrasts with using the funds for qualified education expenses, where the earnings would be tax-free. The tax burden significantly alters the financial equation and may make alternative repayment strategies more appealing. Another example might involve a family using 529 funds for a down payment on a house. This would incur the income tax and penalty, potentially making the use of other savings more efficient.

Scenario Leading to an Audit

A scenario that could trigger an IRS audit might involve claiming education expenses for a withdrawal that was demonstrably used for non-educational purposes. For example, if a beneficiary withdraws funds for a down payment on a car and then attempts to claim it as tuition payment on their tax return, this misrepresentation would likely lead to an audit. The IRS often cross-references information from various sources, including bank statements and other financial records, to verify the accuracy of tax filings. Inconsistencies in the claimed use of funds versus documented evidence of spending would immediately raise red flags. Similarly, claiming unusually large withdrawals for expenses not commensurate with typical educational costs could invite scrutiny.

Illustrative Scenarios

Understanding when using 529 funds for student loan repayment is beneficial or detrimental hinges on a careful evaluation of individual financial circumstances and tax implications. The following scenarios illustrate these contrasting outcomes.

While using 529 plans for non-qualified expenses incurs a 10% penalty on earnings, along with state income taxes in some states, there might be rare situations where it could still be advantageous. This decision should be made only after careful consideration of all available options and potential financial consequences.

Scenario: Financially Advantageous Use of 529 Funds for Student Loans

Imagine Sarah, a high-income earner, who has maxed out her 529 plan for her child’s education. Her child unexpectedly decides to attend a less expensive community college, leaving a substantial surplus in the 529 plan. Simultaneously, Sarah’s child incurs significant student loan debt for postgraduate studies. In this case, using the 529 funds to pay down high-interest student loans, even with the 10% penalty, might be financially advantageous. The interest saved on the loan could potentially outweigh the penalty, especially considering her higher tax bracket. This scenario highlights the importance of considering the overall financial picture, including the interest rates on the loans and the individual’s tax bracket.

Scenario: Financially Disadvantageous Use of 529 Funds for Student Loans

Consider Mark, a middle-income earner, whose child received a generous scholarship, leaving a small balance in their 529 plan. The child has only a small amount of student loan debt at a relatively low interest rate. For Mark, the 10% penalty on the 529 withdrawals, plus potential state taxes, would likely outweigh the benefits of using those funds to pay off the loans. In this situation, he would be better off using other resources, such as savings or a low-interest loan, to repay the student loans and preserving the remaining 529 funds for future educational expenses or other financial goals. This scenario emphasizes the need to compare the cost of the penalty against the potential interest savings.

Family Financial Situation and Optimal 529 Fund Use

The Johnson family has two children. They contributed the maximum allowed to their 529 plans for both children over several years, accumulating $100,000 in each plan. Their older child, Emily, received a full scholarship to a prestigious university. Their younger child, Tom, received a partial scholarship and is now burdened with $30,000 in student loan debt at a 7% interest rate. The family has $50,000 in savings.

Given Emily’s full scholarship, the family has a significant surplus in her 529 plan. Using a portion of Emily’s 529 funds to pay off Tom’s student loans, even with the 10% penalty, could be a prudent strategy. The high-interest rate on Tom’s loans makes the interest savings potentially greater than the penalty. The family should carefully calculate the potential savings versus the penalty to determine the optimal amount to withdraw from Emily’s 529 plan. The remaining funds in both plans can be preserved for future educational expenses or other potential needs. The family’s substantial savings also provide a safety net, allowing them to be more flexible in their approach.

Outcome Summary

Ultimately, the decision of whether or not to use 529 funds to pay off student loans is highly personal and depends on individual circumstances. While the possibility exists, it’s crucial to carefully weigh the potential tax penalties against the benefits of reducing student loan debt. Thoroughly understanding the legal and tax implications, exploring alternative repayment options, and potentially consulting with a financial advisor are vital steps in making an informed and financially responsible choice. This guide has provided a framework for that evaluation, equipping you with the knowledge to navigate this complex financial landscape effectively.

FAQ Explained

What are the tax penalties for using 529 funds for non-qualified expenses?

Earnings withdrawn for non-qualified expenses are subject to income tax plus a 10% penalty.

Can I use 529 funds for graduate school tuition?

Yes, 529 plans can be used for graduate school tuition, provided it meets the plan’s definition of qualified education expenses.

Are there any exceptions to the 10% penalty for non-qualified withdrawals?

There are limited exceptions, such as certain disability expenses for the beneficiary. Consult the IRS guidelines for specifics.

What is the maximum contribution to a 529 plan?

Contribution limits vary by state, but there is usually no federal limit. Check your state’s specific regulations.