Navigating the complex world of student loans can feel overwhelming, especially when faced with the choice between federal and private options, varying repayment plans, and the long-term financial implications. This guide provides a clear and concise overview of credit student loans, equipping you with the knowledge to make informed decisions about financing your education and managing your debt effectively. We’ll explore everything from eligibility and application processes to loan forgiveness programs and strategies for minimizing the impact of student loan debt on your future financial well-being.

Understanding the nuances of interest rates, loan terms, and available repayment options is crucial for responsible borrowing. We’ll delve into practical budgeting techniques and financial planning tools to help you stay on track with your payments and avoid the serious consequences of default. Ultimately, our aim is to empower you with the information needed to successfully manage your student loan journey.

Types of Student Loans

Navigating the world of student loans can feel overwhelming, but understanding the fundamental differences between loan types is crucial for making informed financial decisions. This section will clarify the distinctions between federal and private student loans, outlining repayment options and comparing interest rates and fees. Choosing the right loan significantly impacts your long-term financial health.

Federal vs. Private Student Loans

Federal student loans are offered by the U.S. government through programs like Direct Subsidized and Unsubsidized Loans, and PLUS Loans. Private student loans, on the other hand, are provided by banks, credit unions, and other private lenders. A key difference lies in the borrower protections and repayment options available. Federal loans typically offer more flexible repayment plans and protections against default, while private loan terms can vary significantly depending on the lender. Federal loans also generally have more favorable interest rates, especially for borrowers with good credit.

Federal Student Loan Repayment Plans

Several repayment plans exist for federal student loans, each tailored to different financial situations. The Standard Repayment Plan is a fixed monthly payment over 10 years. The Graduated Repayment Plan starts with lower payments that gradually increase over time. The Extended Repayment Plan stretches payments over a longer period (up to 25 years), resulting in lower monthly payments but higher overall interest paid. Income-Driven Repayment (IDR) plans, such as the Revised Pay As You Earn (REPAYE) plan, tie monthly payments to your income and family size, offering more affordability for borrowers with lower incomes. Choosing the right plan depends on individual financial circumstances and long-term goals.

Interest Rates and Fees: A Comparison

Interest rates and fees vary considerably between federal and private student loans. Federal student loan interest rates are set by the government and are generally lower than those offered by private lenders. Private loan interest rates are influenced by creditworthiness, the loan amount, and the borrower’s chosen repayment terms. Private loans often involve higher fees, including origination fees and prepayment penalties. The table below summarizes these key differences.

| Loan Type | Lender | Interest Rate | Repayment Options |

|---|---|---|---|

| Federal Direct Subsidized Loan | U.S. Department of Education | Variable; depends on loan type and year | Standard, Graduated, Extended, Income-Driven |

| Federal Direct Unsubsidized Loan | U.S. Department of Education | Variable; depends on loan type and year | Standard, Graduated, Extended, Income-Driven |

| Federal Direct PLUS Loan | U.S. Department of Education | Variable; depends on loan type and year | Standard, Extended, Income-Driven (may be limited) |

| Private Student Loan | Banks, Credit Unions, etc. | Variable; based on creditworthiness and other factors | Varies by lender; may include options similar to federal loans but often less flexible |

Managing Student Loan Debt

Successfully navigating student loan debt requires proactive planning and consistent effort. Understanding repayment options, budgeting effectively, and utilizing available resources are crucial for minimizing financial strain and achieving long-term financial well-being. Failing to manage student loan debt effectively can lead to serious consequences, impacting credit scores and overall financial health.

Budgeting and Managing Student Loan Payments

Creating a realistic budget is paramount to managing student loan payments. This involves tracking income and expenses to identify areas for potential savings. Prioritizing student loan payments within the budget ensures timely repayments and avoids late fees or penalties. Consider using budgeting apps or spreadsheets to monitor your financial situation and track progress toward your repayment goals. A successful budget incorporates not only essential expenses like housing and food but also allocates funds specifically for student loan payments, treating them as a non-negotiable expense. Flexibility is key; adjust your budget as needed to accommodate unexpected expenses or changes in income.

Consequences of Defaulting on Student Loans

Defaulting on student loans has severe repercussions. It significantly damages your credit score, making it difficult to secure loans, rent an apartment, or even get a job in certain fields. Wage garnishment is a possibility, where a portion of your earnings is directly deducted to repay the debt. The government may also seize tax refunds or social security benefits. Furthermore, defaulting can lead to legal action, including lawsuits and potential damage to your financial reputation. In short, defaulting can create a cycle of financial hardship that is difficult to escape.

Financial Planning Tools and Resources

Numerous resources are available to assist with student loan debt management. The National Foundation for Credit Counseling (NFCC) offers free and low-cost credit counseling services, including guidance on debt management plans. StudentAid.gov, the official U.S. Department of Education website, provides comprehensive information on federal student loan programs and repayment options. Many online budgeting tools and apps, such as Mint or YNAB (You Need A Budget), can help track expenses and create personalized budgets. Finally, consider seeking advice from a financial advisor who can provide personalized guidance based on your specific financial situation.

Sample Budget Incorporating Student Loan Payments

The following is a sample budget, and individual needs will vary significantly. Remember, this is just an example, and your actual budget should reflect your personal income and expenses.

| Income | Amount |

|---|---|

| Monthly Net Income | $3000 |

| Expenses | Amount |

| Housing | $1000 |

| Food | $500 |

| Transportation | $200 |

| Utilities | $150 |

| Student Loan Payment | $300 |

| Other Expenses (Entertainment, Savings, etc.) | $850 |

| Total Expenses | $3000 |

Remember to adjust this sample budget to reflect your own income and expenses. Prioritize essential expenses and allocate funds for student loan payments consistently.

Loan Forgiveness and Repayment Programs

Navigating the complexities of student loan repayment can feel overwhelming. Fortunately, several programs exist to help borrowers manage their debt and, in some cases, achieve complete loan forgiveness. Understanding the eligibility criteria, requirements, and benefits of these programs is crucial for effective debt management. This section will explore various loan forgiveness and repayment options available to student loan borrowers.

Public Service Loan Forgiveness (PSLF) Program Criteria

The Public Service Loan Forgiveness (PSLF) program offers complete forgiveness of remaining federal student loan debt after 120 qualifying monthly payments under an income-driven repayment plan while working full-time for a qualifying government or non-profit organization. Key criteria include employment by a qualifying employer, consistent repayment under an income-driven repayment plan, and the type of federal student loans held. It’s important to note that only Direct Loans qualify for PSLF; Federal Family Education Loan (FFEL) Program loans and Perkins Loans generally do not, unless they’ve been consolidated into a Direct Consolidation Loan. Furthermore, consistent, on-time payments are critical; even a single missed payment can significantly impact eligibility. Careful tracking of payments and employment verification are essential for successful PSLF application.

Income-Driven Repayment Plan Requirements

Income-driven repayment (IDR) plans adjust monthly payments based on your income and family size. Several IDR plans exist, including Income-Based Repayment (IBR), Pay As You Earn (PAYE), Revised Pay As You Earn (REPAYE), and Income-Contingent Repayment (ICR). Eligibility generally requires federal student loans and submission of income and family size information annually. These plans often lead to lower monthly payments than standard repayment plans, but the total amount repaid over the life of the loan may be higher due to extended repayment periods. It’s important to understand the implications of each plan, particularly the potential for loan forgiveness after a specified period (typically 20 or 25 years), and the impact on your credit score if you consistently make the minimum payments.

Comparison of Loan Repayment Programs

Different loan repayment programs cater to varying financial situations and career paths. For instance, PSLF targets public service employees, while IDR plans offer flexibility based on income. Standard repayment plans offer fixed monthly payments over a set period (typically 10 years), while extended repayment plans stretch the repayment period, reducing monthly payments but increasing the total interest paid. Borrowers should carefully weigh the advantages and disadvantages of each program to determine the best fit for their individual circumstances. Factors to consider include the length of the repayment period, the total interest paid, and the potential for loan forgiveness.

Loan Forgiveness and Repayment Programs Summary

| Program Name | Eligibility Requirements | Benefits | Application Process |

|---|---|---|---|

| Public Service Loan Forgiveness (PSLF) | Full-time employment with qualifying employer, 120 qualifying monthly payments under an income-driven repayment plan, Direct Loans | Complete loan forgiveness after 120 qualifying payments | Online application through studentaid.gov |

| Income-Based Repayment (IBR) | Federal student loans, annual income and family size verification | Lower monthly payments based on income | Online application through your loan servicer |

| Pay As You Earn (PAYE) | Federal student loans, annual income and family size verification | Lower monthly payments based on income, potential for loan forgiveness after 20 years | Online application through your loan servicer |

| Revised Pay As You Earn (REPAYE) | Federal student loans, annual income and family size verification | Lower monthly payments based on income, potential for loan forgiveness after 20 or 25 years | Online application through your loan servicer |

| Income-Contingent Repayment (ICR) | Federal student loans, annual income and family size verification | Lower monthly payments based on income | Online application through your loan servicer |

| Standard Repayment Plan | Federal student loans | Fixed monthly payments over 10 years | Automatic enrollment upon loan disbursement, or you can choose it online |

| Extended Repayment Plan | Federal student loans | Lower monthly payments over a longer period (up to 25 years) | Online application through your loan servicer |

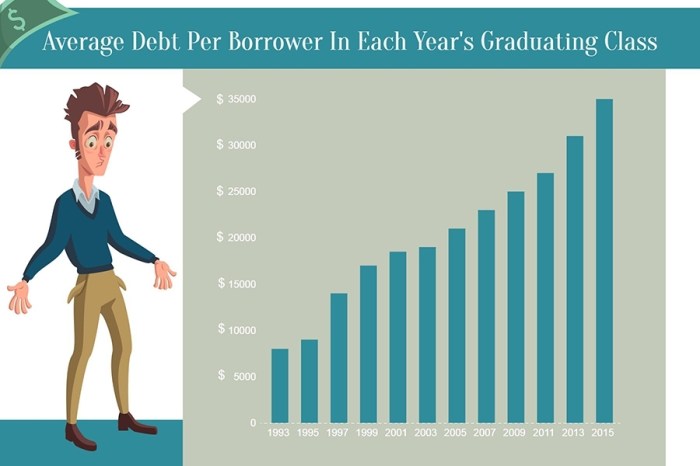

The Impact of Student Loans on Personal Finances

Student loan debt can significantly impact your financial well-being for years, even decades, after graduation. Understanding the long-term implications and proactively managing your debt is crucial for achieving your financial goals. Failing to plan effectively can lead to missed opportunities and financial stress.

The long-term financial implications of student loan debt extend far beyond the monthly payment. High levels of debt can restrict your ability to save for retirement, purchase a home, or even start a family. The interest accrued over the life of the loan can dramatically increase the total amount you repay, potentially delaying major life milestones. This debt can also affect your credit score, impacting your ability to secure loans or credit cards with favorable terms in the future. Careful planning and strategic management are key to mitigating these potential negative consequences.

Minimizing the Impact of Student Loan Debt on Future Financial Goals

Careful budgeting and a strategic approach to debt repayment are vital for minimizing the impact of student loans on future financial goals. Prioritizing high-interest loans and exploring options like income-driven repayment plans can help manage your debt more effectively. Simultaneously, building a strong savings plan, even with limited funds, is essential. This could involve prioritizing emergency savings and gradually increasing contributions to retirement accounts and other long-term savings vehicles. For example, allocating a small portion of your income each month, even if it’s just a small amount, towards savings can significantly impact your future financial security. By consistently saving and strategically managing debt, you can create a solid financial foundation despite the presence of student loans.

Student Loan Consolidation

Consolidating student loans involves combining multiple loans into a single loan with a new interest rate and repayment schedule. The potential benefits include simplifying payments with a single monthly payment and potentially lowering your monthly payment amount (though this might extend the repayment period and increase total interest paid). However, drawbacks include potentially locking in a higher interest rate than some of your existing loans, particularly if you had loans with low interest rates, and potentially losing benefits associated with specific loan programs, such as loan forgiveness options for public service employees. For example, a borrower with multiple federal loans at varying interest rates might consolidate to simplify payments, but this could lead to a higher total interest paid over the life of the loan if the new consolidated rate is higher than the lowest rate of the individual loans. Careful consideration of both benefits and drawbacks is essential before deciding to consolidate.

The Effect of Different Repayment Plans on Total Interest Paid

Different repayment plans significantly affect the total interest paid over the life of the loan. Consider this hypothetical example: Suppose a borrower has a $30,000 student loan with a 6% interest rate. Under a standard 10-year repayment plan, the monthly payment would be approximately $330, and the total interest paid would be around $10,000. However, under an extended 20-year repayment plan, the monthly payment would be reduced to approximately $200, but the total interest paid would increase to approximately $19,000. This demonstrates that while a longer repayment plan lowers the monthly payment, it increases the total interest paid. Choosing a repayment plan requires balancing affordability with the long-term cost of interest.

Choosing the right repayment plan depends on your individual financial situation and priorities.

Understanding Interest Rates and Loan Terms

Navigating the complexities of student loan repayment requires a solid understanding of interest rates and loan terms. These factors significantly influence the total cost of your education and the length of your repayment journey. Failing to grasp these concepts can lead to unexpected expenses and prolonged debt.

Understanding how interest accrues and the various types of loan terms available is crucial for making informed decisions and developing an effective repayment strategy.

Compound Interest and its Impact

Compound interest is the interest calculated not only on the principal amount of the loan but also on the accumulated interest from previous periods. This means that your interest grows exponentially over time, significantly increasing the total amount you owe. For example, imagine a $10,000 loan with a 5% annual interest rate. In the first year, you’ll owe $500 in interest. However, in the second year, the interest is calculated on the $10,500 (principal + interest), resulting in a higher interest payment. This compounding effect accelerates debt growth, making it essential to understand and address it early in the repayment process. The longer you take to repay, the more substantial the impact of compound interest becomes.

Interest Rate Calculation Methods

Several methods exist for calculating interest on student loans. The most common is the simple interest method, where interest is calculated only on the principal amount. However, most student loans use compound interest, as explained above. The frequency of compounding (daily, monthly, annually) also affects the total interest paid. Daily compounding, for instance, leads to slightly higher interest charges compared to annual compounding, as interest is calculated and added to the principal more frequently. Understanding the specific compounding frequency of your loan is crucial for accurate repayment planning.

Fixed vs. Variable Interest Rates

Student loans typically come with either fixed or variable interest rates. A fixed interest rate remains constant throughout the loan’s life, providing predictability in your monthly payments. A variable interest rate, on the other hand, fluctuates based on market conditions. While a variable rate might start lower than a fixed rate, it can increase over time, potentially leading to higher monthly payments and a larger total repayment amount. Choosing between a fixed and variable rate depends on your risk tolerance and financial outlook. A fixed rate offers stability, while a variable rate might offer initial savings but carries the risk of future increases.

Illustrative Representation of Debt Growth

Imagine two scenarios: one with a $20,000 loan at a 4% fixed interest rate and another with the same loan amount but at a 7% fixed interest rate. Over ten years, the loan with the 4% interest rate would accumulate significantly less interest than the loan with the 7% interest rate. Visually, this could be represented as two upward-sloping lines on a graph. The line representing the 7% interest rate would have a steeper slope, showing a much faster increase in the total amount owed compared to the line representing the 4% interest rate. This difference in slope visually demonstrates the substantial impact of even a small difference in interest rates over an extended repayment period. After ten years, the total amount owed on the 7% loan would be considerably higher, highlighting the importance of securing the lowest possible interest rate when taking out student loans.

Closing Summary

Successfully managing student loan debt requires careful planning, proactive budgeting, and a thorough understanding of available resources. By understanding the different types of loans, eligibility requirements, repayment options, and loan forgiveness programs, you can create a personalized financial strategy that aligns with your long-term goals. Remember to utilize the available financial tools and resources to monitor your progress and make informed decisions throughout the repayment process. Taking a proactive approach to student loan management will contribute significantly to your overall financial health and future success.

Quick FAQs

What happens if I miss a student loan payment?

Missing payments can lead to late fees, damage your credit score, and potentially result in loan default, with serious financial consequences.

Can I consolidate my student loans?

Yes, consolidating multiple loans into a single loan can simplify payments and potentially lower your monthly payment, but carefully consider the potential impact on your overall interest paid.

What is the difference between a fixed and variable interest rate?

A fixed interest rate remains constant throughout the loan term, while a variable rate fluctuates based on market conditions.

Are there any tax benefits associated with student loan interest?

You may be able to deduct a portion of the interest you pay on your student loans from your federal income tax. Consult a tax professional for details.