Navigating the world of student loans can feel overwhelming, especially when faced with the initial hurdle of entrance counseling. This crucial step sets the stage for responsible borrowing and repayment, impacting your financial future significantly. Understanding the process, your repayment options, and available resources empowers you to make informed decisions and manage your debt effectively.

This guide provides a comprehensive overview of entrance counseling for student loans, covering everything from the initial online session to long-term financial planning strategies. We’ll explore various repayment plans, address common challenges, and delve into loan forgiveness programs, offering practical advice and resources to help you succeed.

Understanding Entrance Counseling

Entrance counseling serves as a crucial introductory step for students receiving federal student loans. It’s designed to equip borrowers with the knowledge and understanding necessary to manage their loans responsibly and avoid future financial difficulties. This session provides vital information about loan repayment, repayment options, and the overall implications of borrowing for education.

The Purpose of Entrance Counseling

The primary purpose of entrance counseling is to educate student loan borrowers about their responsibilities and rights as borrowers. This includes understanding the terms of their loan agreement, exploring various repayment options, and learning about the consequences of defaulting on their loans. The goal is to promote responsible borrowing and successful loan repayment.

Key Topics Covered During Entrance Counseling

A typical entrance counseling session covers several key areas. These include a detailed explanation of the types of federal student loans available, the terms and conditions associated with each loan, the total amount borrowed, and the repayment schedule. Borrowers also receive information on various repayment plans, including income-driven repayment options, and the potential consequences of default, such as damage to credit score and wage garnishment. Finally, borrowers are often given information on resources available to help them manage their loans and avoid default.

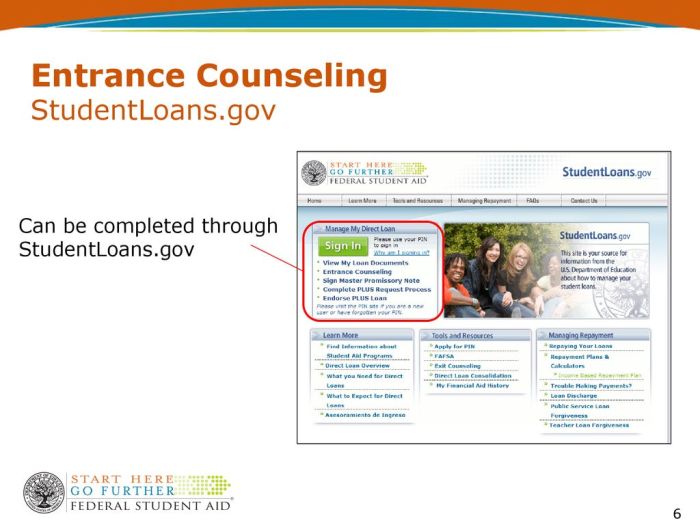

Completing the Online Entrance Counseling Process

Completing online entrance counseling is a straightforward process. First, the borrower needs to access the official website of the U.S. Department of Education’s Federal Student Aid (FSA) website. Next, they will need to log in using their FSA ID. Once logged in, they should navigate to the entrance counseling section. The process involves reviewing informational modules and answering a series of questions to confirm understanding. Upon successful completion of all modules and questions, a confirmation page will be generated, confirming the completion of entrance counseling. This confirmation should be printed or saved for future reference.

Entrance Counseling Requirements: Federal vs. Private Loans

Entrance counseling is mandatory for federal student loans, but not typically required for private student loans. Federal loans require completion of entrance counseling before funds are disbursed. Private lenders, on the other hand, may offer their own educational materials or counseling sessions, but these are not federally mandated. This difference highlights the greater regulatory oversight of federal student loan programs compared to private student loan programs.

Flowchart Illustrating the Entrance Counseling Process

Imagine a flowchart with the following steps:

1. Start: The process begins when a student is approved for federal student loans.

2. Access FSA Website: The student logs into the Federal Student Aid website using their FSA ID.

3. Locate Entrance Counseling: The student navigates to the online entrance counseling section.

4. Review Modules: The student reviews the provided educational modules.

5. Answer Questions: The student answers a series of questions to test their understanding.

6. Completion Confirmation: Upon successful completion, the student receives a confirmation of completion.

7. End: The entrance counseling process is complete. The student can now receive their loan funds.

Loan Repayment Options Explained

Understanding your repayment options is crucial for successfully managing your student loans. Choosing the right plan can significantly impact your monthly payments and overall loan cost. Several plans cater to different financial situations and priorities.

Federal student loans offer a variety of repayment plans, each with its own set of terms and conditions. These plans differ in their repayment periods, monthly payment amounts, and total interest paid over the life of the loan. The best option for you will depend on your individual circumstances, such as your income, your debt load, and your financial goals.

Standard Repayment Plan

The Standard Repayment Plan is the most common option. Under this plan, you make fixed monthly payments over a 10-year period. The payment amount is calculated based on your loan amount, interest rate, and loan term. This plan is straightforward and offers the shortest repayment period, leading to less interest paid overall compared to longer-term plans. However, the monthly payments may be higher than other plans.

Example: A $30,000 loan with a 5% interest rate would have a monthly payment of approximately $317 under a standard 10-year repayment plan. The total interest paid over the life of the loan would be approximately $7,000.

Extended Repayment Plan

If the monthly payments under the Standard Repayment Plan are too high, you may qualify for an Extended Repayment Plan. This plan stretches your repayment period to up to 25 years, resulting in lower monthly payments. However, this will increase the total amount of interest you pay over the life of the loan.

Example: The same $30,000 loan with a 5% interest rate would have a significantly lower monthly payment under a 25-year extended plan, but the total interest paid would likely exceed $15,000.

Graduated Repayment Plan

With the Graduated Repayment Plan, your monthly payments start low and gradually increase over time. This plan can be helpful for borrowers who expect their income to increase in the future. Like the extended plan, it results in a longer repayment period and higher total interest paid than the standard plan.

Example: Initial payments might be considerably lower than the standard plan, but they will increase annually, eventually exceeding the standard plan’s payment in later years.

Income-Driven Repayment Plans

Income-driven repayment plans tie your monthly payment to your income and family size. These plans typically offer lower monthly payments than other plans, but they often extend the repayment period to 20 or 25 years, leading to potentially higher total interest paid. There are several types of income-driven repayment plans, including:

| Plan Name | Payment Calculation | Maximum Repayment Period | Loan Forgiveness Eligibility |

|---|---|---|---|

| Income-Based Repayment (IBR) | Based on discretionary income and family size | 20 or 25 years | Yes, after 20 or 25 years |

| Pay As You Earn (PAYE) | Based on discretionary income and family size | 20 years | Yes, after 20 years |

| Revised Pay As You Earn (REPAYE) | Based on discretionary income and family size; includes both undergraduate and graduate loans | 20 or 25 years | Yes, after 20 or 25 years |

| Income-Contingent Repayment (ICR) | Based on income and loan amount | 25 years | Yes, after 25 years |

Important Note: Loan forgiveness under income-driven repayment plans is subject to tax implications. The forgiven amount may be considered taxable income.

Sample Repayment Schedule (Standard Repayment Plan)

This is a hypothetical example and actual payments may vary based on interest rates and loan amounts.

Loan Amount: $20,000

Interest Rate: 6%

Repayment Period: 10 years

A sample repayment schedule would show a series of monthly payments, beginning with the first month and continuing for 120 months (10 years). Each payment would consist of a portion going towards principal and a portion towards interest. The principal portion would gradually increase over time, while the interest portion would decrease.

Managing Student Loan Debt

Successfully navigating student loan repayment requires proactive planning and a clear understanding of potential challenges. This section will equip you with the knowledge and strategies to effectively manage your debt and achieve financial stability.

Common Challenges Faced by Student Loan Borrowers

Many borrowers encounter difficulties in managing their student loan debt. These challenges often stem from a combination of factors, including unexpected life events, insufficient budgeting, and a lack of understanding of repayment options. For example, job loss, unexpected medical expenses, or family emergencies can significantly impact a borrower’s ability to make timely payments. Additionally, underestimating the total cost of repayment or failing to adequately factor loan payments into a monthly budget can lead to financial strain and potential default. Finally, a lack of awareness regarding available repayment plans and assistance programs can leave borrowers feeling overwhelmed and unprepared.

Strategies for Effective Budgeting and Financial Planning for Loan Repayment

Creating a realistic budget is crucial for successful loan repayment. This involves tracking all income and expenses to identify areas where spending can be reduced. Prioritize essential expenses like housing, food, and transportation, then allocate funds towards loan payments. Consider using budgeting apps or spreadsheets to monitor your progress and ensure you stay on track. A comprehensive financial plan should also include short-term and long-term goals, such as saving for emergencies and planning for future expenses like a down payment on a house. For instance, setting a goal of paying off your loans within a specific timeframe and adjusting your budget accordingly can create a clear path to financial freedom.

Tips for Avoiding Late Payments and Managing Unexpected Financial Difficulties

Preventing late payments requires proactive planning and establishing a system for consistent repayment. Setting up automatic payments can eliminate the risk of missed payments due to oversight. Creating a buffer in your budget specifically for loan payments can provide a safety net for unexpected expenses. If you anticipate difficulty making a payment, contact your loan servicer immediately to explore options like forbearance or deferment. These programs offer temporary relief from payments but should be used judiciously, as they may result in increased interest charges. For example, a sudden job loss might necessitate a temporary forbearance, allowing time to find new employment and resume payments without defaulting on the loan.

Calculating Total Interest Paid Over the Life of a Student Loan

Calculating the total interest paid is crucial for understanding the true cost of your loan. While precise calculations require loan-specific details, a general understanding can be gained. The total interest paid depends on factors such as the loan’s principal amount, interest rate, and repayment term. A simple, though not perfectly accurate, calculation can be performed using an amortization schedule provided by your loan servicer. This schedule will detail each payment’s allocation between principal and interest. Alternatively, many online loan calculators allow you to input your loan details to estimate the total interest paid. For example, a $20,000 loan with a 5% interest rate over 10 years could result in several thousand dollars in interest paid, significantly increasing the overall cost.

The total interest paid will be the difference between the total amount paid and the principal amount of the loan.

Resources Available to Student Loan Borrowers Seeking Financial Assistance

Numerous resources exist to assist student loan borrowers facing financial hardship. The federal government offers programs like income-driven repayment plans that adjust monthly payments based on income and family size. Non-profit organizations and credit counseling agencies provide free or low-cost financial guidance and assistance with debt management strategies. Your loan servicer can also provide information on available repayment options and hardship programs. Finally, exploring options such as loan consolidation or refinancing might reduce your monthly payments or lower your overall interest rate. Knowing where to find help is critical, and these resources can provide support and guidance during challenging times.

Understanding Loan Forgiveness Programs

Student loan forgiveness programs offer the potential for significant debt reduction, but understanding their complexities is crucial before relying on them. These programs vary widely in eligibility requirements, application processes, and the amount of debt forgiven. Careful consideration of both the benefits and drawbacks is essential for informed decision-making.

Eligibility Requirements for Loan Forgiveness Programs

Eligibility for student loan forgiveness programs hinges on several factors, primarily the type of loan, your occupation, and your income. For example, the Public Service Loan Forgiveness (PSLF) program requires borrowers to make 120 qualifying monthly payments under an income-driven repayment plan while working full-time for a qualifying government or non-profit organization. Other programs, like the Teacher Loan Forgiveness program, have specific requirements related to teaching in low-income schools. Income-based repayment plans often factor into eligibility, limiting forgiveness to borrowers meeting specific income thresholds. Detailed eligibility criteria are available on the Federal Student Aid website.

The Application Process for Loan Forgiveness Programs

Applying for loan forgiveness involves a multi-step process requiring meticulous attention to detail. Borrowers must typically complete a comprehensive application form, providing documentation such as proof of employment, tax returns, and loan disbursement records. The specific documents required vary depending on the program. The application process can be lengthy, and careful record-keeping is essential to avoid delays or denials. It’s often beneficial to consult with a financial advisor or student loan counselor to navigate the complexities of the application process.

Comparison of Loan Forgiveness Programs

Several federal student loan forgiveness programs exist, each with its unique features. The PSLF program, for instance, forgives the remaining balance of federal Direct Loans after 120 qualifying payments, while the Teacher Loan Forgiveness program forgives up to $17,500 in federal student loans for teachers who meet specific requirements. Income-Driven Repayment (IDR) plans, such as ICR, PAYE, REPAYE, and IBR, can lead to loan forgiveness after a certain number of years, but the amount forgiven depends on the borrower’s income and loan balance. A thorough comparison of these programs should consider the eligibility criteria, the length of time required to qualify, and the potential amount of loan forgiveness.

Potential Benefits and Drawbacks of Loan Forgiveness

The primary benefit of loan forgiveness is the elimination of a significant financial burden. This can free up resources for other financial goals, such as saving for retirement or purchasing a home. However, loan forgiveness programs often have strict eligibility requirements and may take many years to complete. Furthermore, some programs may result in a higher tax liability on the forgiven amount, offsetting some of the financial benefits. It’s important to weigh these potential drawbacks against the long-term financial benefits before pursuing loan forgiveness.

Common Misconceptions About Loan Forgiveness Programs

Understanding the realities of loan forgiveness programs is critical to avoid disappointment. Here are some common misconceptions:

- Misconception: All federal student loans are eligible for forgiveness programs. Reality: Eligibility varies by loan type and program. Federal Direct Loans are typically eligible for most programs, but Federal Family Education Loans (FFEL) and Perkins Loans often have limited or no forgiveness options.

- Misconception: The application process is simple and straightforward. Reality: Applications often require extensive documentation and careful adherence to program guidelines. Errors can lead to significant delays or denials.

- Misconception: Loan forgiveness eliminates all tax implications. Reality: Forgiven loan amounts are often considered taxable income, potentially resulting in a tax liability.

- Misconception: Loan forgiveness is guaranteed. Reality: Eligibility requirements must be meticulously met, and approval is not guaranteed.

The Impact of Student Loans on Future Financial Planning

Student loan debt can significantly influence your long-term financial well-being, impacting major life decisions and requiring careful planning to mitigate its effects. Understanding these implications is crucial for navigating your financial future successfully. This section explores the long-term financial ramifications of student loan debt and offers strategies for minimizing its impact.

Long-Term Financial Implications of Student Loan Debt

Student loan debt extends beyond graduation. Monthly payments can consume a substantial portion of your income for many years, potentially delaying other financial goals. High debt levels can affect your credit score, making it harder to secure loans for a home, car, or even a business in the future. Furthermore, the interest accrued over time can significantly increase the total amount you repay, compounding the financial burden. The opportunity cost of paying down loans is also considerable; the money used for loan repayments could have been invested, generating returns or used for other important financial objectives.

Impact on Major Life Decisions

Student loan debt can significantly influence major life decisions. Buying a home might be delayed or require a smaller, less desirable property due to limited borrowing capacity. Starting a family may be postponed due to financial constraints. Even seemingly smaller decisions, such as choosing a career path, may be affected by the need to prioritize higher-paying jobs to manage loan repayments, potentially sacrificing personal fulfillment.

Strategies for Minimizing the Impact of Student Loan Debt

Several strategies can help minimize the impact of student loan debt on long-term financial goals. Creating a realistic budget that prioritizes loan repayments is essential. Exploring different repayment plans, such as income-driven repayment or refinancing, can lower monthly payments and potentially reduce the overall amount paid. Prioritizing high-interest loans first and actively paying more than the minimum payment whenever possible can significantly reduce the total interest paid and shorten the repayment period. Building a strong emergency fund can help mitigate unexpected financial setbacks that could otherwise jeopardize repayment plans. Finally, focusing on consistent and responsible financial habits, such as saving and investing, can help build financial stability despite the presence of student loan debt.

Hypothetical Scenario: Long-Term Impact of Repayment Strategies

Let’s consider two hypothetical graduates, both with $50,000 in student loan debt at a 6% interest rate. Sarah opts for the standard 10-year repayment plan, while Mark chooses an income-driven repayment plan that extends the repayment period to 20 years. Over the 10 years, Sarah pays approximately $60,000 in total (including interest). Mark pays approximately $75,000 over 20 years. While Mark’s monthly payments are lower, he pays significantly more in interest over the longer repayment period. This illustrates the importance of considering the trade-offs between lower monthly payments and overall repayment costs.

Visual Representation: Student Loan Debt and Long-Term Financial Stability

Imagine a graph with “Years After Graduation” on the x-axis and “Net Worth” on the y-axis. Two lines represent the net worth of individuals with and without significant student loan debt. The line representing the individual with student loan debt starts lower than the other and initially increases more slowly due to loan repayments. However, once the loans are repaid, the line’s slope increases, eventually converging with or even surpassing the line of the individual without debt, demonstrating the long-term potential for financial recovery and stability after successfully managing student loan repayment. The gap between the lines represents the opportunity cost of carrying the debt, highlighting the importance of proactive financial planning.

Last Point

Successfully completing entrance counseling is the first step toward responsible student loan management. By understanding your repayment options, budgeting effectively, and exploring available resources, you can navigate the complexities of student loan debt and build a strong financial foundation for the future. Remember, proactive planning and informed decision-making are key to achieving long-term financial stability.

FAQ Explained

What happens if I don’t complete entrance counseling?

You may not be able to receive your student loan funds. It’s a mandatory step for federal loans.

Can I complete entrance counseling anytime?

Yes, you can typically complete it at any time before your loans disburse.

Is entrance counseling the same for all types of student loans?

No, the requirements and process may vary slightly between federal and private loans. Federal loans usually require mandatory entrance counseling.

What if I have questions after completing entrance counseling?

Most lenders provide contact information and resources to answer your questions. You can also seek help from your school’s financial aid office.