Navigating the complexities of student loan repayment can feel overwhelming, but understanding the available options and developing a strategic plan can significantly ease the process. This guide provides a comprehensive overview of the steps involved, from identifying your loan servicer and exploring various repayment plans to managing your budget effectively and considering loan forgiveness programs. We’ll demystify key terms, compare different repayment strategies, and offer practical advice to help you embark on your repayment journey with confidence.

Successfully managing student loan debt requires a proactive approach. This involves not only understanding the intricacies of your loan agreements but also aligning your repayment strategy with your overall financial goals. By carefully considering your income, expenses, and long-term financial aspirations, you can create a personalized repayment plan that minimizes stress and maximizes your chances of timely repayment.

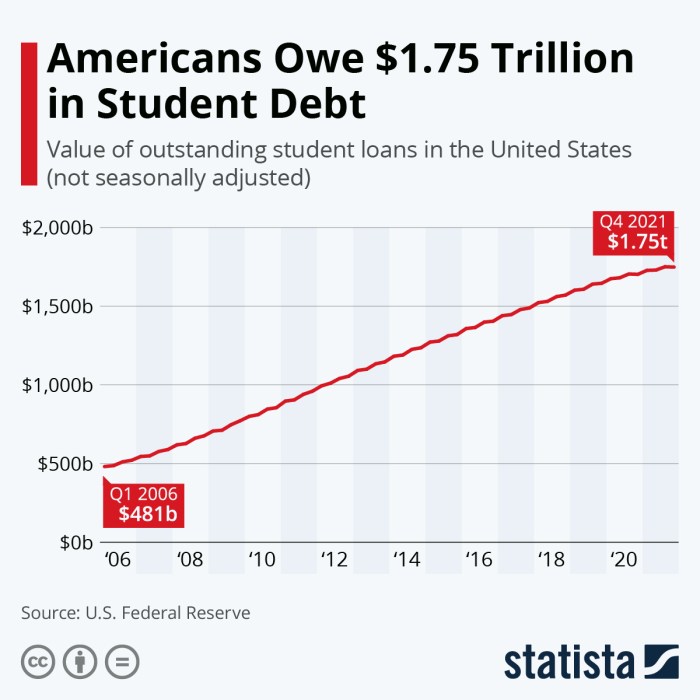

Understanding Your Student Loans

Navigating the world of student loan repayment can feel overwhelming, but understanding the basics is the first step towards effective management. This section will clarify the different types of loans, key terminology, and how to access your loan information. Armed with this knowledge, you can confidently begin your repayment journey.

Types of Student Loans

Student loans are broadly categorized into federal and private loans. Federal loans are offered by the U.S. government and generally offer more borrower protections and repayment options than private loans. Private loans, on the other hand, are provided by banks, credit unions, or other private lenders. Understanding these distinctions is crucial for making informed financial decisions.

- Federal Student Loans: These include subsidized and unsubsidized loans, PLUS loans (for parents and graduate students), and Perkins Loans (a need-based loan program). Subsidized loans don’t accrue interest while you’re in school, grace periods, or deferment, while unsubsidized loans accrue interest from the time the loan is disbursed. PLUS loans typically have higher interest rates than subsidized and unsubsidized loans. Perkins loans are generally offered at lower interest rates and have specific eligibility requirements.

- Private Student Loans: These loans are offered by private lenders and typically have variable interest rates, meaning the interest rate can change over the life of the loan. They often require a creditworthy co-signer, especially for students with limited or no credit history. Borrower protections may be less extensive than with federal loans.

Key Loan Repayment Terms

Several key terms are essential to understanding your student loan repayment. Familiarity with these terms will empower you to make informed decisions about your repayment strategy.

- Principal: The original amount of money borrowed.

- Interest Rate: The percentage of the principal that you pay as interest. This is usually expressed as an annual percentage rate (APR).

- Amortization: The process of paying off a loan over time through regular payments. Each payment typically covers a portion of the principal and the accrued interest. A standard amortization schedule details the amount of principal and interest paid in each installment.

- Interest Capitalization: The process of adding unpaid interest to the principal balance of your loan. This increases the total amount you owe.

Locating Your Loan Servicer and Accessing Loan Details

Knowing who your loan servicer is and how to access your loan information online is vital for managing your student loans effectively. This involves a straightforward process, typically involving the following steps:

- Identify your loan servicer: You can usually find this information on your student loan documents or through the National Student Loan Data System (NSLDS) website. The NSLDS is a centralized database of federal student aid information.

- Visit your servicer’s website: Once you know your servicer, navigate to their website. Most servicers provide online portals where you can access your loan details, make payments, and explore repayment options.

- Log in or create an account: You’ll likely need to create an online account using your personal information and loan details. Follow the instructions provided by your servicer.

- Review your loan information: Once logged in, you can view your loan balance, interest rate, payment due date, and repayment plan details.

Exploring Repayment Plans

Choosing the right student loan repayment plan is crucial for managing your debt effectively and achieving your long-term financial goals. Different plans offer varying monthly payment amounts, total interest paid, and loan forgiveness opportunities. Understanding these differences is key to making an informed decision.

Several repayment plans are available, each with its own set of advantages and disadvantages. The best option for you will depend on your individual financial situation, income, and long-term objectives. Let’s examine the most common plans.

Standard Repayment Plan

The Standard Repayment Plan is a fixed monthly payment plan typically spread over 10 years. It offers predictable payments but often results in higher monthly payments compared to other plans. This plan is suitable for borrowers with stable income and a strong desire to pay off their loans quickly.

Extended Repayment Plan

The Extended Repayment Plan stretches payments over a longer period, usually up to 25 years. This significantly lowers your monthly payments, making it more manageable for borrowers with limited income. However, you’ll pay considerably more interest over the life of the loan. This plan is best for borrowers prioritizing lower monthly payments over faster repayment.

Graduated Repayment Plan

The Graduated Repayment Plan starts with lower monthly payments that gradually increase over time. This option can be helpful for borrowers anticipating income growth. While initially manageable, the payments can become significantly higher later in the repayment period. Careful budgeting is crucial to ensure affordability as payments rise.

Income-Driven Repayment Plans (IDR Plans)

Income-Driven Repayment Plans, such as ICR, PAYE, REPAYE, andIBR, base your monthly payment on your income and family size. These plans generally result in lower monthly payments, and some offer loan forgiveness after a set number of qualifying payments. However, IDR plans often extend the repayment period significantly, leading to higher total interest paid. They are ideal for borrowers with lower incomes or unpredictable financial situations.

Comparison of Repayment Plans

The following table provides a simplified comparison of the four repayment plans. Note that the monthly payment example, total interest paid, and loan forgiveness eligibility are estimates and will vary significantly based on individual loan amounts, interest rates, and income levels. Consult your loan servicer for personalized estimates.

| Plan Name | Monthly Payment Example | Total Interest Paid (Estimate) | Loan Forgiveness Eligibility |

|---|---|---|---|

| Standard | $500 | $20,000 | No |

| Extended | $250 | $40,000 | No |

| Graduated | $300 (increasing) | $35,000 | No |

| Income-Driven | $200 (variable) | $45,000 | Yes, after 20-25 years (depending on plan and income) |

Managing Your Budget and Finances

Successfully managing your finances is crucial for tackling student loan repayment. A well-structured budget allows you to visualize your income and expenses, identify areas for savings, and allocate funds specifically for your loan payments. This process ensures that loan repayment becomes a manageable part of your overall financial picture, preventing overwhelming debt and promoting financial well-being.

Creating a realistic budget is the first step towards effective student loan repayment. This involves accurately tracking your income and expenses to understand your current financial situation. From there, you can strategically allocate funds towards your loan payments while ensuring you meet your other financial obligations.

Sample Budget Template

A comprehensive budget should include all sources of income and all expenses. The following template provides a framework:

| Income | Amount |

|---|---|

| Net Salary (After Taxes) | $ |

| Other Income (e.g., part-time job, side hustle) | $ |

| Total Monthly Income | $ |

| Expenses | Amount |

| Housing (Rent/Mortgage) | $ |

| Utilities (Electricity, Water, Gas) | $ |

| Transportation (Car Payment, Gas, Public Transport) | $ |

| Food (Groceries, Eating Out) | $ |

| Student Loan Payment | $ |

| Healthcare (Insurance, Medical Expenses) | $ |

| Debt Payments (Other Loans, Credit Cards) | $ |

| Personal Care | $ |

| Entertainment | $ |

| Savings | $ |

| Total Monthly Expenses | $ |

| Remaining Balance | $ |

Remember to replace the “$” with your actual amounts. Tracking your spending for a month before creating your budget will provide a realistic picture of your expenses.

Strategies for Reducing Expenses and Increasing Income

Reducing unnecessary expenses and exploring opportunities to increase income are vital for freeing up funds for loan repayment. This requires a conscious effort to identify areas where spending can be cut back and actively seek additional income streams.

Effective strategies include identifying areas of overspending, such as dining out or entertainment, and finding more affordable alternatives. For example, cooking at home more often and opting for free or low-cost entertainment options can significantly reduce monthly expenses. Increasing income can involve seeking a higher-paying job, taking on a part-time job, or exploring freelance opportunities. Negotiating a higher salary in your current role is another avenue to explore.

Prioritizing Debt Repayment

Prioritizing student loan repayment alongside other financial obligations requires a strategic approach. Several methods exist, including the debt avalanche method (paying off the highest interest debt first) and the debt snowball method (paying off the smallest debt first for motivation). Regardless of the chosen method, consistently making at least the minimum payment on all debts is crucial to avoid late fees and negative impacts on your credit score. Building an emergency fund is also essential to handle unexpected expenses without jeopardizing your loan repayment plan. A well-defined budget, combined with disciplined spending habits and a proactive approach to income generation, will facilitate successful student loan repayment while maintaining financial stability.

Exploring Loan Forgiveness Programs

Navigating the complexities of student loan repayment can be daunting, but understanding the potential for loan forgiveness programs can offer a significant pathway to debt reduction. Several federal programs exist designed to alleviate the burden of student loan debt for individuals working in specific public service roles or meeting certain criteria. These programs offer varying degrees of forgiveness, but all require careful consideration of eligibility requirements and application processes.

Public Service Loan Forgiveness (PSLF) Program

The Public Service Loan Forgiveness (PSLF) program is designed to forgive the remaining balance on your Direct Loans after you’ve made 120 qualifying monthly payments under a qualifying repayment plan while working full-time for a qualifying employer.

Eligibility for PSLF hinges on several key factors:

- Employment: You must be employed full-time by a government organization or a 501(c)(3) non-profit organization.

- Loan Type: Only Direct Loans qualify for PSLF. Federal Family Education Loans (FFEL) and Perkins Loans are not eligible unless they’ve been consolidated into a Direct Consolidation Loan.

- Repayment Plan: You must be enrolled in an income-driven repayment (IDR) plan, such as Income-Based Repayment (IBR), Pay As You Earn (PAYE), Revised Pay As You Earn (REPAYE), or Income-Contingent Repayment (ICR).

The application process involves certifying your employment and repayment history through the PSLF Help Tool. It’s crucial to maintain accurate records and proactively monitor your progress toward forgiveness.

Teacher Loan Forgiveness Program

This program offers forgiveness of up to $17,500 on your federal student loans if you meet specific requirements related to teaching in a low-income school or educational service agency.

Key eligibility criteria for Teacher Loan Forgiveness include:

- Employment: You must teach full-time for at least five complete and consecutive academic years in a low-income school or educational service agency.

- Loan Type: The program covers Direct Subsidized and Unsubsidized Loans, as well as Stafford Loans.

- Repayment Plan: There is no specific repayment plan requirement for this program.

The application process involves submitting documentation verifying your employment and loan information to the Department of Education. Careful record-keeping is essential to demonstrate eligibility.

Other Loan Forgiveness Programs

Beyond PSLF and Teacher Loan Forgiveness, other programs may offer partial or complete loan forgiveness depending on your specific circumstances and profession. These often have more niche requirements and may be tied to specific professions or geographic locations. Examples include programs focused on specific medical professions or those working in underserved communities. It is essential to research these programs thoroughly and consult the Department of Education website for the most up-to-date information.

Seeking Professional Advice

Navigating the complexities of student loan repayment can feel overwhelming. Many borrowers find themselves struggling to understand the various repayment plans, forgiveness programs, and financial strategies available to them. Seeking professional guidance can significantly simplify this process and help you develop a personalized repayment strategy that aligns with your financial goals.

A financial advisor specializing in student loan debt can provide invaluable support throughout your repayment journey. Their expertise extends beyond simply choosing a repayment plan; they can offer holistic financial planning that incorporates your student loans into a broader financial strategy. This includes considering your income, expenses, savings goals, and overall financial health.

Financial Advisor’s Role in Student Loan Repayment

Financial advisors play a crucial role in helping borrowers create effective student loan repayment strategies. They analyze your individual financial situation, considering factors like your income, expenses, loan types, and interest rates. Based on this analysis, they can recommend the most suitable repayment plan, explore potential avenues for loan forgiveness or consolidation, and help you budget effectively to ensure timely payments. They also act as a valuable resource, answering questions and providing ongoing support throughout the repayment process. This personalized approach can save borrowers time, money, and a significant amount of stress. For example, a financial advisor could identify opportunities to refinance loans at lower interest rates, potentially saving thousands of dollars over the life of the loan. They could also help you create a realistic budget that accounts for loan payments while still allowing you to meet other financial goals, such as saving for a down payment on a house or investing for retirement.

Resources for Finding Reputable Financial Advisors

Finding a reputable financial advisor specializing in student loan debt requires careful research. Several resources can assist in this process.

It’s crucial to verify the advisor’s credentials and experience. Look for advisors with certifications such as Certified Financial Planner (CFP) or Chartered Financial Consultant (ChFC). These designations indicate a commitment to professional standards and ethical conduct. You can also check the advisor’s background and any disciplinary actions through resources like the Financial Industry Regulatory Authority (FINRA) BrokerCheck website. Additionally, seeking recommendations from trusted sources like family, friends, or colleagues can be helpful. Online platforms, such as those offered by professional financial organizations, often provide directories of advisors with their qualifications and areas of expertise.

Benefits of Seeking Professional Guidance

The benefits of seeking professional guidance in managing student loan debt are substantial. A financial advisor can provide a personalized strategy tailored to your specific circumstances, potentially saving you money and time in the long run. They can navigate the complexities of loan repayment options, ensuring you choose the plan that best aligns with your financial goals and risk tolerance. Moreover, they offer ongoing support and guidance, providing reassurance and helping you stay on track with your repayment plan. This support is particularly valuable during challenging financial periods, as a financial advisor can help you adjust your strategy as needed. For instance, if you experience a job loss or unexpected medical expenses, they can help you explore options like forbearance or deferment to avoid defaulting on your loans. The peace of mind and reduced stress associated with having a professional guide you through this process are also significant benefits.

Understanding Deferment and Forbearance

Deferment and forbearance are two options available to student loan borrowers who are experiencing temporary financial hardship and are unable to make their scheduled payments. While both provide temporary relief from loan payments, they differ significantly in their implications and requirements. Understanding the nuances of each is crucial for making informed decisions about your student loan repayment strategy.

Deferment and forbearance both temporarily postpone your student loan payments, preventing late payment penalties and defaults. However, they differ in their eligibility requirements and the impact on your loan balance. Deferment is typically granted based on specific qualifying circumstances, while forbearance is generally more broadly available but may come with different terms.

Comparison of Deferment and Forbearance

Deferment and forbearance offer temporary relief from student loan payments, but they have distinct differences. Deferment is generally considered more favorable as interest may not accrue on subsidized federal loans during the deferment period. In contrast, interest typically continues to accrue on loans during forbearance, increasing the total loan balance.

| Feature | Deferment | Forbearance |

|---|---|---|

| Eligibility | Based on specific qualifying circumstances (e.g., unemployment, graduate school enrollment) | Generally more broadly available, often based on demonstrated financial hardship |

| Interest Accrual (Federal Subsidized Loans) | May not accrue | Usually accrues |

| Interest Accrual (Federal Unsubsidized Loans & Private Loans) | Usually accrues | Usually accrues |

| Length | Limited to specific periods defined by the loan program | Can vary depending on the lender and the borrower’s situation, potentially up to a year |

| Impact on Credit Score | Generally less negative impact than forbearance, as payments are officially paused | Can negatively impact credit score due to missed payments, even if temporary |

Implications for Loan Balances and Credit Scores

The impact of deferment and forbearance on your loan balance and credit score varies depending on the type of loan and the terms of the deferment or forbearance agreement. With deferment, interest may not accrue on subsidized federal loans, keeping your loan balance the same. However, interest will typically continue to accrue on unsubsidized federal loans and private student loans during both deferment and forbearance. This means your total loan balance will increase over time.

Forbearance, because it involves missed payments, can negatively affect your credit score. Lenders view missed payments, even temporary ones, as a sign of potential financial instability. The severity of the impact depends on factors like your credit history, the length of the forbearance period, and the number of times you’ve used forbearance. It’s crucial to carefully consider the potential long-term effects on your creditworthiness before opting for forbearance.

Examples of Appropriate Use

Deferment might be appropriate for a borrower who is enrolled in graduate school or is experiencing unemployment due to a job loss. Forbearance might be a suitable option for a borrower facing a temporary financial setback such as a medical emergency or a period of reduced income. However, it is vital to weigh the long-term consequences of accruing interest and potential credit score damage before choosing forbearance. A borrower should explore all available options and seek professional financial advice before making a decision.

Preventing Future Student Loan Debt

Navigating the complexities of higher education financing requires a proactive approach to responsible borrowing. By understanding the implications of student loans and implementing effective strategies, you can minimize future debt and pave the way for a more financially secure future. This involves careful planning, budgeting, and a thorough understanding of loan terms.

Preventing excessive student loan debt necessitates a multifaceted strategy encompassing responsible borrowing practices, effective budgeting, and a clear understanding of loan agreements. Failure to address these aspects can lead to significant financial burdens that extend far beyond graduation.

Responsible Borrowing During College

Prioritize minimizing loan amounts by exploring all available financial aid options. This includes grants, scholarships, and work-study programs, which don’t require repayment. A thorough application process for these non-loan options can significantly reduce the reliance on loans. Consider attending a community college for the first two years to lower overall tuition costs before transferring to a four-year university. This strategy allows you to acquire foundational courses at a lower cost, potentially saving thousands of dollars. Furthermore, carefully consider the cost of attendance versus the potential return on investment (ROI) of your chosen degree program. Some career paths offer higher earning potential, justifying a larger investment in education, while others may not warrant the same level of debt.

Effective Budgeting for Educational Expenses

Creating a realistic budget is crucial for managing educational expenses effectively. Track all income sources, including part-time jobs, scholarships, and financial aid. Categorize expenses, including tuition, fees, books, housing, transportation, and living expenses. Prioritize essential expenses and identify areas where spending can be reduced. For example, explore affordable housing options, utilize public transportation, or find cost-effective ways to purchase textbooks. Utilize budgeting apps or spreadsheets to monitor spending and ensure you stay within your allocated budget. A sample budget might allocate 50% of income to essential needs (housing, food), 30% to wants (entertainment, dining out), and 20% to savings and debt repayment. Regularly review and adjust your budget as needed to reflect changes in income or expenses.

Understanding Loan Terms Before Signing

Before signing any loan agreement, thoroughly review all terms and conditions. Understand the interest rate, repayment terms, and any associated fees. Compare loan offers from different lenders to find the most favorable terms. Pay close attention to the loan’s interest rate – a lower interest rate will result in less overall interest paid over the life of the loan. Also, understand the repayment schedule – will it be a fixed payment or variable payment? Understanding the loan’s terms empowers you to make informed decisions and avoid unexpected financial surprises. If any aspect of the loan agreement is unclear, seek clarification from the lender before signing. Avoid signing any loan agreement without a complete understanding of its implications.

Dealing with Delinquency or Default

Falling behind on your student loan payments can have serious consequences, impacting your credit score and financial well-being. Understanding the potential ramifications and available options is crucial for navigating this challenging situation. This section Artikels the consequences of delinquency and default, steps to take if you’re struggling, and the options available to help you regain control of your student loan debt.

Delinquency and default significantly damage your credit history. A delinquent loan is one where payments are missed, typically after 30 days. This immediately negatively impacts your credit score, making it harder to secure loans, rent an apartment, or even get a job in some cases. Default, which usually occurs after 9 months of non-payment, leads to even more severe consequences. These consequences can include wage garnishment, tax refund offset, and even legal action. The damage to your credit score can last for years, making future borrowing significantly more expensive.

Consequences of Delinquency and Default

Delinquency results in negative marks on your credit report, lowering your credit score and potentially impacting your ability to obtain credit in the future. Default, a more severe stage of delinquency, can lead to wage garnishment (a portion of your paycheck being seized to pay the debt), tax refund offset (the government intercepting your tax refund to pay the debt), and even lawsuits. Furthermore, default can make it difficult to rent an apartment, purchase a car, or obtain other financial products. The negative impact on your credit score can persist for seven years or longer.

Steps to Take When Facing Payment Difficulties

If you anticipate difficulty making your student loan payments, immediate action is vital. First, contact your loan servicer as soon as possible. Explain your situation honestly and explore available options. Many servicers offer hardship programs, which might include temporary reduced payments, deferment, or forbearance. Creating a detailed budget to identify areas for potential savings can help free up funds for loan payments. Consider exploring additional income sources, such as a part-time job or freelance work. Finally, seeking professional financial advice can provide valuable guidance and support in developing a sustainable repayment plan.

Options for Borrowers Struggling with Repayment

Several options exist to assist borrowers facing repayment challenges. Deferment temporarily postpones payments, but interest may still accrue on unsubsidized loans. Forbearance also postpones payments, but interest typically accrues. Income-driven repayment plans (IDR) adjust your monthly payments based on your income and family size. These plans can significantly lower monthly payments, but they may extend the repayment period and increase the total interest paid over the life of the loan. Loan consolidation combines multiple loans into a single loan with a potentially lower monthly payment. However, it might not always lower the total interest paid. Finally, exploring loan forgiveness programs, such as Public Service Loan Forgiveness (PSLF), may be an option for certain borrowers who meet specific eligibility requirements. Each option has its own eligibility criteria and potential implications, so careful consideration is essential.

Final Review

Repaying student loans is a significant financial undertaking, but with careful planning and a proactive approach, it’s entirely manageable. By understanding your loan details, exploring different repayment options, budgeting effectively, and seeking professional guidance when needed, you can create a path toward financial freedom. Remember, proactive management, coupled with a realistic budget and a long-term perspective, will significantly improve your chances of successful and timely repayment. Don’t hesitate to utilize the available resources and seek professional advice to navigate this important financial journey.

FAQ

What happens if I miss a student loan payment?

Missing payments can lead to late fees, negatively impact your credit score, and potentially result in your loan going into default.

Can I consolidate my student loans?

Yes, consolidating multiple loans into a single loan can simplify repayment, potentially lowering your monthly payment. However, it might extend your repayment period and increase total interest paid.

What if I can’t afford my student loan payments?

Contact your loan servicer immediately to explore options like deferment, forbearance, or income-driven repayment plans. They can help you create a more manageable payment plan.

How do I find my loan servicer?

Your loan servicer’s contact information should be available on your loan documents or through the National Student Loan Data System (NSLDS).