Securing a federal student loan can be a pivotal step towards higher education, but navigating the process can feel overwhelming. Understanding eligibility requirements, the FAFSA application, loan types, repayment options, and potential scams is crucial for a smooth and successful experience. This guide aims to demystify the process, providing clear and concise information to empower you in your pursuit of financial aid.

From exploring different federal student aid programs and understanding income limitations to mastering the FAFSA application and choosing the right repayment plan, we’ll cover all the essential aspects. We’ll also highlight potential pitfalls, like common scams, and equip you with the knowledge to avoid them. By the end, you’ll have a comprehensive understanding of how to obtain and manage a federal student loan effectively.

Eligibility Requirements for Federal Student Loans

Securing federal student loans involves meeting specific eligibility criteria. Understanding these requirements is crucial for successfully navigating the application process and obtaining the financial assistance needed for higher education. This section details the various federal student aid programs, income limitations, and a step-by-step guide to determine your eligibility.

Types of Federal Student Aid Programs

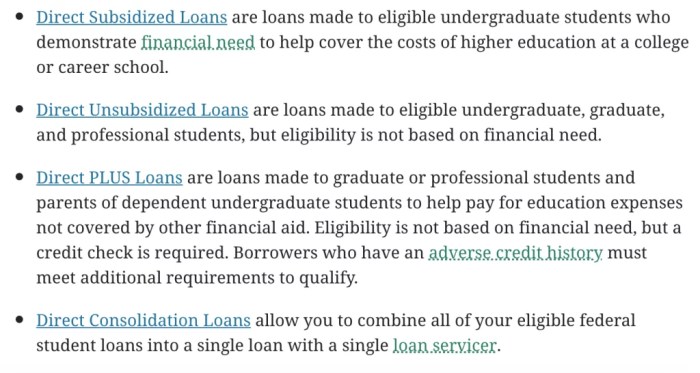

Federal student aid encompasses several programs, each with its own eligibility requirements and disbursement methods. These programs are designed to assist students from various backgrounds and financial situations. The primary programs include Federal Pell Grants, Federal Subsidized Loans, Federal Unsubsidized Loans, and Federal PLUS Loans (for parents and graduate students). Pell Grants are need-based and do not need to be repaid, while loans require repayment after graduation or leaving school. Subsidized loans accrue interest only after the grace period, whereas unsubsidized loans accrue interest during the entire loan period. PLUS loans are available to parents of undergraduate students and to graduate students.

Income Requirements and Limitations

Eligibility for federal student aid, particularly Pell Grants and subsidized loans, is often tied to the student’s and their family’s demonstrated financial need. The Free Application for Federal Student Aid (FAFSA) assesses this need using the prior year’s tax information. There are no strict income limits for unsubsidized loans or PLUS loans, but the amount you can borrow might be affected by your credit history (for PLUS loans). A higher income generally translates to a lower amount of need-based aid, potentially reducing the amount of Pell Grants or subsidized loans received. For example, a family with an annual income exceeding $200,000 might receive minimal or no Pell Grant funding.

Determining Eligibility: A Step-by-Step Guide

1. Complete the FAFSA: This application is the cornerstone of the federal student aid process. Accurate and timely completion is crucial.

2. Provide Required Documentation: Gather tax returns, W-2 forms, and other requested financial information. Inaccurate information can delay or prevent the disbursement of funds.

3. Review Your Student Aid Report (SAR): The SAR summarizes your financial information and provides an estimate of your eligibility for federal aid. Review it carefully for accuracy.

4. Accept Your Award: Once you receive your award notification, accept the aid you wish to receive.

5. Complete Loan Entrance Counseling: This is mandatory for federal student loans and covers important information about repayment responsibilities.

Comparison of Eligibility Criteria for Federal Student Loan Programs

| Program | Credit Check Required? | Income-Based Eligibility? | Borrower Type |

|---|---|---|---|

| Federal Pell Grant | No | Yes (need-based) | Undergraduate students |

| Federal Subsidized Loan | No | Yes (need-based) | Undergraduate students |

| Federal Unsubsidized Loan | No | No | Undergraduate and graduate students |

| Federal PLUS Loan | Yes (for parents and graduate students) | No | Parents of undergraduate students and graduate students |

The FAFSA Application Process

The Free Application for Federal Student Aid (FAFSA) is the gateway to federal student financial aid. Completing this form accurately and thoroughly is crucial for determining your eligibility for grants, loans, and work-study programs. The FAFSA collects information about your family’s financial situation to calculate your Expected Family Contribution (EFC), a key factor in determining your financial aid package.

The FAFSA form itself is a comprehensive document requesting detailed information about your family’s income, assets, and household size. It’s designed to provide a standardized assessment of your financial need, allowing colleges and universities to distribute limited aid resources fairly. The information provided on the FAFSA is used by the federal government, as well as individual colleges and universities, to determine the type and amount of financial aid you may receive.

Required Documents for FAFSA Completion

Gathering the necessary documents before starting the FAFSA application will streamline the process significantly. Having this information readily available will prevent delays and ensure a smoother application experience. These documents provide the data points needed to accurately assess your financial need.

- Social Security Numbers (SSNs): Your SSN and the SSNs of your parents (if you are a dependent student) are required.

- Federal Tax Returns (IRS Tax Transcripts): Your tax information, and your parents’ tax information (if you are a dependent student), including W-2s, is essential for accurate income reporting.

- Driver’s Licenses or State IDs: These documents are helpful for verifying your identity.

- Bank Statements and Investment Records: Information on your assets, and your parents’ assets (if you are a dependent student), is required to complete the asset section of the FAFSA.

- Records of Untaxed Income: This includes income such as child support, alimony, and other sources of untaxed income.

Creating an FSA ID and Accessing the FAFSA Website

To access and complete the FAFSA, both you and at least one of your parents (if you are a dependent student) will need an FSA ID. The FSA ID is a username and password that serves as your electronic signature. It allows you to access and manage your FAFSA data securely.

To create an FSA ID, visit the Federal Student Aid website (studentaid.gov). You will need to provide personal information such as your name, date of birth, and social security number to verify your identity. Once verified, you can create a unique username and password. This FSA ID is then used to sign your FAFSA application electronically, and provides access to other financial aid related websites.

The FAFSA Verification Process

Some applicants are selected for verification after submitting their FAFSA. This process involves providing additional documentation to confirm the accuracy of the information reported on your FAFSA. Verification helps ensure the integrity of the financial aid system and accurate allocation of funds.

If selected for verification, you will receive a notification from your college or the Federal Student Aid office. This notification will specify the additional documents you need to submit. Common documents requested during verification include tax returns, W-2s, and bank statements. Failure to respond to the verification request can delay or prevent the disbursement of your financial aid. It is crucial to respond promptly and completely to avoid any potential issues.

Types of Federal Student Loans

Navigating the world of federal student loans can seem daunting, but understanding the different types available is crucial for making informed financial decisions. This section will clarify the distinctions between subsidized and unsubsidized loans, Direct Loans and other federal loan programs, and will Artikel the interest rates and repayment terms associated with each.

Subsidized and Unsubsidized Federal Student Loans

The primary difference between subsidized and unsubsidized federal student loans lies in whether the government pays the interest while you’re in school. Subsidized loans are need-based; the government pays the interest during periods of deferment (e.g., while you’re enrolled at least half-time or during grace periods). Unsubsidized loans, on the other hand, accrue interest from the time the loan is disbursed, regardless of your enrollment status. This means you’ll owe more on an unsubsidized loan by the time you begin repayment. Eligibility for subsidized loans is determined by your financial need as assessed through the FAFSA.

Direct Loans and Other Federal Loan Programs

The most common type of federal student loan is a Direct Loan. These loans are disbursed directly by the Department of Education. While there have been other federal loan programs in the past (such as the Stafford Loan program, which was replaced by the Direct Loan program), Direct Loans currently represent the primary avenue for federal student loan funding. The simplification of the loan process under the Direct Loan program has streamlined the application and disbursement procedures for students.

Interest Rates and Repayment Terms for Federal Student Loans

Interest rates for federal student loans are set annually by the government and vary depending on the loan type (subsidized vs. unsubsidized) and the loan disbursement date. These rates are generally lower than private loan interest rates. Repayment typically begins six months after graduation or leaving school (the grace period), and several repayment plans are available, including standard, graduated, extended, and income-driven repayment plans. Income-driven repayment plans, in particular, tie monthly payments to your income and family size, making them more manageable for borrowers with lower incomes. The length of the repayment period depends on the repayment plan chosen, ranging from 10 years to 25 or more years for certain income-driven plans. Failure to repay loans can result in serious consequences, including damage to credit score and potential wage garnishment.

Key Features of Different Federal Student Loan Types

| Loan Type | Interest Accrual | Eligibility | Repayment Options |

|---|---|---|---|

| Subsidized Direct Loan | Interest subsidized during deferment | Demonstrated financial need | Standard, graduated, extended, income-driven |

| Unsubsidized Direct Loan | Interest accrues from disbursement | No financial need requirement | Standard, graduated, extended, income-driven |

| Direct PLUS Loan (Graduate/Parent) | Interest accrues from disbursement | Credit check required (with exceptions for adverse credit) | Standard, graduated, extended, income-driven |

Loan Repayment Options

Understanding your repayment options is crucial after graduating and starting to repay your federal student loans. The federal government offers a variety of repayment plans designed to accommodate different financial situations and income levels. Choosing the right plan can significantly impact your monthly payments and overall repayment timeline. Careful consideration of your individual circumstances is key to selecting the most suitable option.

Choosing a repayment plan involves balancing affordability with the total amount of interest paid over the life of the loan. Some plans offer lower monthly payments but extend the repayment period, leading to higher overall interest costs. Conversely, plans with higher monthly payments can shorten the repayment period and minimize overall interest.

Standard Repayment Plan

The Standard Repayment Plan is the default plan for most federal student loans. It typically involves fixed monthly payments over a 10-year period. This plan provides a predictable payment schedule and is generally the quickest way to repay your loans. However, monthly payments can be relatively high, potentially straining borrowers’ budgets, especially in the early stages of their careers. For example, a $30,000 loan at a 5% interest rate would result in approximate monthly payments of around $317.

Graduated Repayment Plan

The Graduated Repayment Plan offers lower monthly payments initially, gradually increasing over time. This plan can be more manageable in the early years after graduation when income is typically lower. However, the increasing payments can become challenging later on. Using the same $30,000 loan example at 5% interest, the initial monthly payment might be around $200, rising steadily over the 10-year repayment period.

Extended Repayment Plan

This plan extends the repayment period to up to 25 years, significantly reducing monthly payments. This can be beneficial for borrowers with high loan balances or limited income. However, extending the repayment period will result in paying significantly more interest over the life of the loan. For instance, the $30,000 loan at 5% interest spread over 25 years could result in monthly payments of approximately $167, but the total interest paid would be considerably higher than under the Standard Repayment Plan.

Income-Driven Repayment Plans

Income-driven repayment plans (IDRs) link your monthly payment to your income and family size. These plans are designed to make repayment more manageable for borrowers with lower incomes. Eligibility generally requires completing the FAFSA and demonstrating financial need. There are several types of IDRs, including Income-Based Repayment (IBR), Pay As You Earn (PAYE), Revised Pay As You Earn (REPAYE), and Income-Contingent Repayment (ICR). Each plan has slightly different eligibility criteria and payment calculation formulas. Monthly payments under IDRs can be significantly lower than under standard plans, but repayment periods are often longer, resulting in higher total interest paid. The exact monthly payment will depend on individual income and family size, varying greatly from borrower to borrower.

Repayment Plan Comparison

The following table summarizes the pros and cons of the repayment plans discussed:

| Repayment Plan | Pros | Cons |

|---|---|---|

| Standard Repayment | Predictable payments, shortest repayment period | High monthly payments |

| Graduated Repayment | Lower initial payments | Payments increase over time, potentially becoming unaffordable |

| Extended Repayment | Low monthly payments | Longest repayment period, high total interest paid |

| Income-Driven Repayment | Payments based on income and family size, more affordable for low-income borrowers | Longer repayment period, high total interest paid |

Understanding Loan Forgiveness and Deferment

Navigating the complexities of federal student loans often involves understanding the possibilities of loan forgiveness and deferment. These options can provide crucial relief during periods of financial hardship or in specific circumstances. This section will clarify the conditions under which these options are available and Artikel the application processes.

Loan forgiveness programs eliminate a portion or all of your student loan debt. Deferment and forbearance, on the other hand, temporarily postpone or reduce your loan payments. It’s important to note that while they offer temporary relief, they don’t erase the debt; it simply delays repayment.

Federal Student Loan Forgiveness Programs

Several federal programs offer loan forgiveness, each with specific eligibility requirements. For example, the Public Service Loan Forgiveness (PSLF) program forgives the remaining balance on Direct Loans after 120 qualifying monthly payments while working full-time for a qualifying government or non-profit organization. Teacher Loan Forgiveness offers partial loan forgiveness to teachers who meet specific requirements, such as teaching in a low-income school for five consecutive academic years. Income-Driven Repayment (IDR) plans can lead to loan forgiveness after a set number of years, depending on the plan and your income. Eligibility for these programs varies significantly based on the type of loan, employment history, and income. Careful review of the specific program requirements is crucial before applying.

Applying for Loan Deferment or Forbearance

The process for applying for deferment or forbearance typically involves submitting an application to your loan servicer. You will need to provide documentation supporting your request, such as proof of unemployment, enrollment in school, or medical documentation. The approval process and the length of the deferment or forbearance period vary depending on your circumstances and the type of loan. It’s essential to contact your loan servicer directly to understand the specific requirements and timelines for your situation.

Examples of Qualifying Situations

Several situations may qualify for loan deferment, forbearance, or forgiveness. For example, unemployment due to job loss, a medical emergency requiring significant expenses, or enrollment in school may qualify for deferment. Working for a qualifying non-profit organization could lead to eligibility for Public Service Loan Forgiveness. Experiencing significant financial hardship, documented through income verification, may qualify for an income-driven repayment plan that could eventually lead to forgiveness. It is crucial to carefully review the specific requirements for each program and situation.

Steps to Apply for Loan Forgiveness or Deferment

Applying for loan forgiveness or deferment involves several key steps:

- Identify the appropriate program: Determine which loan forgiveness program or deferment/forbearance option best suits your situation.

- Gather necessary documentation: Collect all required documentation, such as proof of employment, income verification, or medical records.

- Contact your loan servicer: Reach out to your loan servicer to obtain the application and understand the specific requirements.

- Complete and submit the application: Carefully fill out the application and submit it with all supporting documentation.

- Monitor the application status: Track the progress of your application and follow up with your loan servicer if needed.

Potential Scams and Avoiding Them

Navigating the world of federal student loans can be complex, and unfortunately, this complexity makes it a breeding ground for scams targeting unsuspecting students and families. Understanding common scams and implementing preventative measures is crucial to protecting your financial well-being. This section Artikels common scams, warning signs, and verification methods to help you avoid becoming a victim.

Scammers often prey on the urgency and stress associated with securing funding for education. They leverage misinformation and deceptive tactics to gain access to your personal and financial information. It’s vital to remain vigilant and approach any loan-related communication with a healthy dose of skepticism.

Common Student Loan Scams

Several types of scams target students seeking federal student loans. These scams can range from phishing emails and fake websites to fraudulent loan modification schemes and upfront fee demands.

- Phishing Emails and Text Messages: These often appear to be from the Department of Education or a legitimate lender, requesting personal information or login credentials. They may create a sense of urgency, claiming immediate action is required to avoid penalties or missed payments.

- Fake Websites: Scammers create websites that mimic the official websites of federal student aid programs, enticing users to submit their sensitive information. These sites may look incredibly realistic, making it difficult to spot the differences.

- Loan Modification Scams: These scams promise to reduce your loan payments or interest rates in exchange for an upfront fee. Legitimate loan modification programs do not require upfront payments.

- Upfront Fee Scams: Some scammers demand fees for processing your loan application or guaranteeing loan approval. Federal student loans never require upfront payments.

Warning Signs of Student Loan Scams

Several warning signs can help you identify potential scams. Paying close attention to these indicators can prevent you from falling victim to fraudulent schemes.

- Unsolicited Communication: Be wary of any unsolicited emails, phone calls, or text messages offering student loan assistance. Legitimate lenders will not typically contact you unless you have initiated contact with them.

- Requests for Personal Information: Never provide your Social Security number, bank account details, or other sensitive information unless you are certain you are interacting with a legitimate source.

- High-Pressure Tactics: Legitimate lenders will not pressure you into making quick decisions. If someone is pressuring you to act immediately, it’s a major red flag.

- Guarantees of Approval: No lender can guarantee loan approval. Be skeptical of anyone making such a promise.

- Unexplained Fees: Federal student loans do not involve upfront fees. Any request for payment before loan disbursement is a significant red flag.

Verifying the Legitimacy of Loan Providers

Taking steps to verify the legitimacy of any loan provider is essential. Here are some ways to ensure you are dealing with a trustworthy source.

- Check the Website’s URL: Look closely at the website address for any misspellings or unusual characters. Legitimate lenders will have secure and official-looking websites.

- Contact the Lender Directly: If you receive unsolicited communication, contact the lender directly using information found on their official website to verify the communication’s authenticity.

- Verify the Lender’s Credentials: Check if the lender is licensed and registered with the appropriate regulatory bodies.

- Read Reviews and Testimonials: Look for online reviews and testimonials from other borrowers to gauge the lender’s reputation.

- Consult with a Financial Advisor: Seeking advice from a trusted financial advisor can provide an extra layer of security.

Visual Representation of Common Scam Tactics and Avoidance Strategies

Imagine a flowchart. The central element is a large, irregular red octagon labeled “Student Loan Scam.” Emanating from it are several pathways, each representing a common scam tactic (phishing email, fake website, etc.). Each pathway is depicted with a jagged, dark grey line. At the end of each pathway is a smaller, light blue circle representing the scam’s outcome (identity theft, financial loss, etc.). These circles contain concise descriptions of the negative consequences. From the central octagon, another set of pathways, depicted with clean, straight green lines, leads to a large green circle labeled “Safe Practices.” These green pathways are labeled with actions to avoid scams (verify website, ignore unsolicited emails, etc.). The green circle contains bullet points listing actions to take, such as contacting the official website directly, verifying the URL, and reporting suspicious activity. The overall color scheme uses contrasting colors to highlight the dangers of scams and the importance of safe practices.

Resources for Further Assistance

Navigating the world of federal student loans can be complex. Fortunately, numerous resources are available to provide guidance and support throughout the entire process, from application to repayment. Understanding where to find reliable information and assistance is crucial for a successful and stress-free experience. This section details key resources and steps to take if you encounter difficulties.

Reliable Websites and Organizations Offering Student Loan Assistance

Several reputable organizations offer comprehensive information and support regarding federal student loans. These resources can provide clarity on loan types, repayment plans, and potential hardship options. Accessing these resources proactively can significantly improve your understanding and management of your student loan debt.

- Federal Student Aid (FSA): The official website for the U.S. Department of Education’s Federal Student Aid program. This site provides comprehensive information on all aspects of federal student loans, including eligibility, application, repayment, and forgiveness programs. It’s the primary source for accurate and up-to-date information.

- National Student Loan Data System (NSLDS): NSLDS is a central database that allows you to access your federal student loan information from multiple sources. You can view your loan history, repayment schedules, and contact information for your loan servicers through this system.

- Consumer Financial Protection Bureau (CFPB): The CFPB offers resources and tools to help consumers understand and manage their debt, including student loans. They provide information on avoiding scams and navigating the complexities of loan repayment.

- Student Loan Borrower Assistance Programs: Many non-profit organizations offer free or low-cost assistance to student loan borrowers. These organizations can provide guidance on repayment options, loan consolidation, and income-driven repayment plans. It is recommended to research organizations in your area or nationally that specialize in student loan assistance.

Government Agency Contact Information

Direct contact with relevant government agencies can be essential for resolving specific issues or obtaining clarification on your student loan situation. Keeping these contact details readily available is highly recommended.

- Federal Student Aid (FSA): You can find contact information, including phone numbers and email addresses, on the official FSA website (studentaid.gov).

- National Student Loan Data System (NSLDS): Contact information for NSLDS is also available on their website (nslds.ed.gov).

- U.S. Department of Education: For broader inquiries related to federal student aid, you can contact the U.S. Department of Education directly through their website (education.gov).

Steps to Take When Experiencing Repayment Difficulties

Facing challenges with student loan repayment is not uncommon. However, proactive steps can help mitigate potential negative consequences. Understanding the available options and seeking assistance promptly is crucial.

If you are experiencing difficulties repaying your federal student loans, you should immediately contact your loan servicer. Explain your situation and explore options such as:

- Deferment or Forbearance: These options temporarily postpone your payments. Eligibility requirements vary depending on your circumstances.

- Income-Driven Repayment Plans: These plans base your monthly payments on your income and family size, making them more manageable for borrowers with lower incomes.

- Loan Consolidation: Combining multiple loans into a single loan can simplify repayment and potentially lower your monthly payments.

- Loan Forgiveness Programs: Certain professions, such as teaching and public service, may qualify for loan forgiveness programs after meeting specific requirements.

Remember, seeking help early is key. Don’t wait until you are significantly behind on payments before contacting your loan servicer or exploring available resources.

Epilogue

Successfully navigating the federal student loan process requires careful planning and a thorough understanding of the available options. By carefully reviewing your eligibility, completing the FAFSA accurately, selecting the appropriate loan type, and understanding repayment plans, you can confidently secure the financial aid you need to pursue your educational goals. Remember to be vigilant against scams and utilize the available resources to ensure a positive and successful experience. With careful preparation and informed decision-making, the path to higher education becomes significantly more manageable.

Expert Answers

What if I don’t qualify for federal student loans?

Explore alternative options like private student loans, scholarships, grants, or part-time employment.

How long does the FAFSA application process take?

The application itself is relatively quick, but processing times can vary. Allow several weeks for processing.

Can I change my repayment plan after I start repaying my loans?

Yes, you can often switch to a different repayment plan, but there may be restrictions or fees depending on the plan.

What happens if I miss a student loan payment?

Missing payments can negatively impact your credit score and may lead to late fees and collection actions.

Where can I find more detailed information about specific loan programs?

The official website of the Federal Student Aid (FSA) provides comprehensive details on all federal student loan programs.