Navigating the complexities of student loan repayment can feel overwhelming. Understanding the repayment timeline is crucial for effective financial planning and avoiding potential pitfalls. This guide explores various repayment plans, factors influencing repayment length, and the consequences of default, empowering you to make informed decisions about your student loan debt.

From standard repayment plans with fixed terms to income-driven plans that adjust payments based on your income, the options available can significantly impact how long it takes to pay off your loans. We’ll delve into the specifics of each plan, highlighting the advantages and disadvantages to help you choose the best strategy for your individual circumstances.

Standard Repayment Plans

Standard repayment plans offer a straightforward approach to repaying student loans. They typically involve fixed monthly payments over a 10-year period, although the exact timeframe can vary slightly depending on the lender and loan amount. This approach provides predictability in budgeting but may result in higher overall interest payments compared to other repayment plans with longer terms.

Standard repayment plans are calculated based on the total loan amount, the interest rate, and the repayment period. The monthly payment is determined using an amortization schedule, which distributes the loan principal and accumulated interest evenly across the repayment term. A higher loan amount or interest rate will naturally result in a larger monthly payment. Conversely, a longer repayment period will result in smaller monthly payments, but the borrower will pay significantly more in interest over the life of the loan.

Standard Repayment Plan Calculation

The precise calculation of a standard repayment plan’s monthly payment involves a complex formula, often handled by loan servicing software. However, a simplified understanding can be achieved by considering the factors involved: The formula takes into account the principal loan amount (P), the annual interest rate (r), and the loan term in months (n). The monthly payment (M) can be approximated using the following formula:

M = P [ r/12 ] / [1 – (1 + r/12)^-n]

Where:

* P = Principal loan amount

* r = Annual interest rate (expressed as a decimal)

* n = Number of months in the repayment period

This formula is complex and best left to loan calculators. However, understanding that higher interest rates and loan amounts lead to higher monthly payments, while longer repayment terms lead to lower monthly payments, is crucial for financial planning.

Examples of Standard Repayment Plans

Let’s consider a few examples to illustrate how different loan amounts and interest rates affect repayment periods under a standard plan. These are simplified examples and do not account for all possible fees or variations among lenders.

* Example 1: A $20,000 loan at a 5% annual interest rate would typically have a 10-year repayment period, resulting in a monthly payment of approximately $212.

* Example 2: A $50,000 loan at a 7% annual interest rate would likely have a 10-year repayment period, resulting in a monthly payment of approximately $560.

* Example 3: A $10,000 loan at a 4% annual interest rate would typically have a 10-year repayment period, resulting in a monthly payment of approximately $106.

These examples demonstrate the direct relationship between the loan amount, interest rate, and the resulting monthly payment.

Comparison of Standard Repayment Plans Across Loan Providers

It’s important to note that repayment terms and interest rates can vary significantly among different loan providers. The following table provides a hypothetical comparison, and actual terms should be verified directly with the lender.

| Loan Provider | Loan Amount | Interest Rate | Repayment Period (Years) |

|---|---|---|---|

| Provider A | $30,000 | 6% | 10 |

| Provider B | $30,000 | 7% | 10 |

| Provider C | $40,000 | 6.5% | 10 |

| Provider D | $25,000 | 5.5% | 10 |

Income-Driven Repayment Plans

Income-driven repayment (IDR) plans offer an alternative to the standard repayment plan, adjusting your monthly payment based on your income and family size. This makes repayment more manageable, particularly for borrowers with lower incomes or significant family responsibilities. Several different IDR plans exist, each with its own nuances regarding eligibility and payment calculations.

Types of Income-Driven Repayment Plans

The federal government offers several income-driven repayment plans. These plans typically recalculate your monthly payment annually or every two years based on your adjusted gross income (AGI) and family size. The specific plans and their features can change, so it’s crucial to check the latest information from the Department of Education or your loan servicer. Common plans include the Income-Based Repayment (IBR), Pay As You Earn (PAYE), Revised Pay As You Earn (REPAYE), and Income-Contingent Repayment (ICR) plans. Each plan employs a different formula to determine your monthly payment.

Income and Family Size’s Influence on Repayment Terms

Your adjusted gross income (AGI) directly impacts your monthly payment under an IDR plan. A lower AGI generally results in a lower monthly payment. Family size also plays a significant role; a larger family typically leads to a reduced monthly payment because the calculation considers the number of dependents. For example, a borrower with a low income and a large family might qualify for a significantly lower monthly payment than a single borrower with a higher income. The specific formulas used vary by plan, but the underlying principle remains consistent: lower income and larger family size equate to smaller monthly payments.

Interest Paid Comparison: Income-Driven vs. Standard Plans

While IDR plans offer lower monthly payments, this benefit often comes at the cost of paying significantly more interest over the life of the loan. The extended repayment period under an IDR plan allows interest to accrue for a longer duration, resulting in a higher total interest paid compared to a standard repayment plan. For instance, a borrower might have a monthly payment that is half the amount under an IDR plan versus a standard plan, but the total interest paid might be double. This trade-off is a crucial consideration when choosing a repayment plan.

Eligibility Criteria for Income-Driven Repayment Plans

Understanding the eligibility requirements for each IDR plan is crucial. These requirements can change, so it’s important to consult official sources for the most up-to-date information.

- Income-Based Repayment (IBR): Generally requires a Direct Loan and may have income limits.

- Pay As You Earn (PAYE): Requires a Direct Loan and may have income limits.

- Revised Pay As You Earn (REPAYE): Generally accepts both Direct and Federal Family Education Loan (FFEL) loans (under certain circumstances) and may have income limits.

- Income-Contingent Repayment (ICR): Generally accepts both Direct and FFEL loans (under certain circumstances) and may have income limits.

Factors Affecting Repayment Length

Understanding the factors that influence student loan repayment duration is crucial for effective financial planning. Several key variables interact to determine how long it takes to become debt-free. This section will explore these factors and their impact on your repayment timeline.

Several key factors significantly impact the length of your student loan repayment period. These factors interact in complex ways, and understanding their influence is crucial for effective repayment planning.

Interest Rates

The interest rate applied to your student loans directly affects the repayment timeline. Higher interest rates mean a larger portion of your monthly payment goes towards interest, leaving less to reduce the principal loan balance. This results in a longer repayment period. For example, a loan with a 7% interest rate will take longer to repay than an identical loan with a 5% interest rate, even with the same monthly payment. The compounding effect of interest can significantly extend the repayment period if not addressed proactively.

Loan Amount

The initial loan amount is a fundamental determinant of repayment length. Larger loan balances naturally require longer repayment periods, even with consistent monthly payments and a fixed interest rate. A borrower with a $50,000 loan will generally take longer to repay than a borrower with a $25,000 loan, assuming all other factors remain constant.

Loan Consolidation

Loan consolidation combines multiple student loans into a single loan with a new interest rate and repayment plan. While it simplifies repayment management by reducing the number of payments, the impact on the overall repayment timeline is variable. Consolidation may result in a shorter repayment period if a lower interest rate is secured. However, if the new interest rate is higher or the repayment term is extended, the overall repayment time could increase. The key is to carefully compare the terms of the consolidated loan with the original loan terms before making a decision.

Impact of Extra Payments

Making extra payments on your student loans can substantially reduce the total repayment time. Even small additional payments each month or year can significantly accelerate the payoff process. For instance, an extra $100 per month can shave years off the repayment period, depending on the loan amount and interest rate. This is because extra payments directly reduce the principal balance, lessening the impact of accruing interest. A simple calculation can illustrate the impact: Suppose you have a $30,000 loan at 6% interest with a 10-year repayment plan. Adding an extra $100 per month could reduce the repayment period by approximately 2 years.

Flowchart Illustrating Factors Interacting to Determine Repayment Length

The following flowchart visually represents how the factors discussed above interact to determine the length of your student loan repayment:

[Imagine a flowchart here. The flowchart would start with a box labeled “Loan Factors,” branching to boxes representing “Loan Amount,” “Interest Rate,” and “Repayment Plan.” Each of these would then branch to a final box labeled “Repayment Length.” Arrows would indicate the flow of influence. Extra payments would be represented as a separate input influencing the “Repayment Length” box.] The flowchart visually demonstrates that the loan amount, interest rate, and chosen repayment plan all contribute to determining the final repayment length. Extra payments would shorten the overall repayment time.

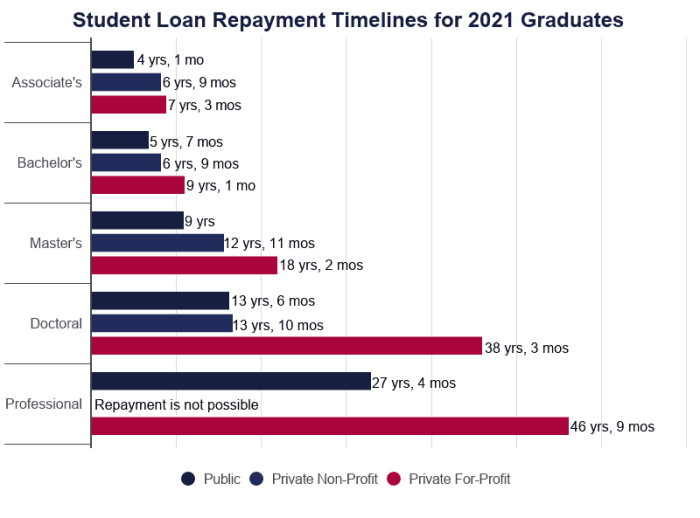

Repayment Options for Different Loan Types

Understanding the repayment options available for your student loans is crucial for effective financial planning. The repayment landscape differs significantly depending on whether your loans are federal or private, impacting your choices and long-term financial obligations. This section details these differences and explores specific repayment schedules and options for various loan types.

Federal student loans and private student loans offer distinct repayment options. Federal loans generally provide a wider range of repayment plans designed to accommodate varying financial situations, including income-driven repayment plans. Private loans, on the other hand, typically offer fewer options, often limited to standard repayment plans with fixed monthly payments. The terms and conditions, including interest rates and fees, also vary substantially.

Repayment Options for Federal Student Loans

Federal student loans, encompassing subsidized, unsubsidized, and Grad PLUS loans, offer several repayment plans. The Standard Repayment Plan involves fixed monthly payments over a 10-year period. Income-Driven Repayment (IDR) Plans, such as the Income-Based Repayment (IBR), Pay As You Earn (PAYE), and Revised Pay As You Earn (REPAYE) plans, adjust monthly payments based on your income and family size, potentially extending the repayment period beyond 10 years. For example, a borrower with a $50,000 loan on a Standard Repayment Plan would have a monthly payment significantly higher than under an IDR plan, though the total repayment period would be longer under the IDR plan. Grad PLUS loans, typically used for graduate studies, follow similar repayment options as other federal loans, though the interest rate is generally higher.

Repayment Options for Private Student Loans

Private student loans, offered by banks and other financial institutions, typically have less flexible repayment options than federal loans. These loans usually only offer a standard repayment plan with fixed monthly payments over a set period, such as 5, 10, or 15 years. Income-driven repayment plans are rarely available. Borrowers should carefully review the terms and conditions of their private loans to understand the repayment schedule and any potential penalties for late or missed payments. For instance, a private loan with a higher interest rate and a shorter repayment period will result in higher monthly payments compared to a loan with a lower interest rate and a longer repayment period.

Forbearance and Deferment

Forbearance and deferment are temporary pauses in loan repayments. Forbearance allows for a temporary suspension of payments, but interest usually continues to accrue. Deferment also suspends payments, but under certain circumstances, interest may not accrue on subsidized federal loans. Both options can extend the overall repayment period and increase the total amount paid due to accumulated interest. For example, a borrower who utilizes forbearance for two years may find their total loan repayment amount significantly higher than initially projected. The availability and terms of forbearance and deferment vary depending on the loan type and lender.

Comparison of Repayment Options

| Loan Type | Repayment Options | Interest Accrual During Deferment | Potential Penalties for Default |

|---|---|---|---|

| Federal Subsidized/Unsubsidized | Standard, Income-Driven, Extended | No (Subsidized), Yes (Unsubsidized) | Wage garnishment, tax refund offset, credit score damage |

| Federal Grad PLUS | Standard, Income-Driven, Extended | Yes | Wage garnishment, tax refund offset, credit score damage |

| Private Student Loans | Standard (Fixed Payments) | Usually Yes | Collection agency involvement, legal action, credit score damage |

Consequences of Defaulting on Student Loans

Defaulting on student loans carries significant and long-lasting negative consequences that extend far beyond simply owing the original debt. These consequences can severely impact your financial future and overall well-being. Understanding these repercussions is crucial for borrowers struggling with repayment.

Defaulting on your student loans triggers a chain reaction of negative events. The most immediate impact is often felt on your credit score, which can plummet, making it difficult to secure loans, rent an apartment, or even obtain a job in some fields. Beyond credit damage, the government can pursue aggressive collection tactics, including wage garnishment, where a portion of your paycheck is automatically seized to pay off the debt. Tax refunds can also be withheld. These actions can create significant financial hardship and severely limit your ability to improve your financial situation.

Credit Score Impact

A student loan default will dramatically lower your credit score. This negative mark remains on your credit report for seven years, hindering your ability to access credit for major purchases like a car or a house. Lenders view defaults as a high risk, leading to higher interest rates or outright loan denials. The impact extends beyond financial transactions; some employers conduct credit checks as part of their hiring process, and a low credit score resulting from a default could negatively affect your job prospects. The severity of the credit score impact depends on the amount of the defaulted loan and the borrower’s overall credit history. For example, a large default on a substantial loan will likely result in a more significant credit score drop than a small default on a smaller loan.

Wage Garnishment and Tax Refund Offset

The Department of Education and its collection agencies have the authority to garnish wages to recover defaulted student loan debt. This means a portion of your paycheck will be automatically deducted and sent to the government to pay down the debt. The amount garnished is typically limited by law, but it can still represent a significant portion of your income, making it difficult to meet your other financial obligations. Additionally, the government can offset your federal tax refund to repay the defaulted loan. This means your refund will be reduced or entirely eliminated to cover the outstanding debt. These actions can cause severe financial distress, particularly for individuals with limited income.

Loan Rehabilitation

Loan rehabilitation is a process that allows borrowers to bring their defaulted federal student loans back into good standing. To rehabilitate a loan, borrowers typically must make nine on-time payments within 20 months. Once the rehabilitation process is complete, the default is removed from the borrower’s credit report, and the loan is reinstated with new repayment terms. However, it’s important to note that the interest that accrued during the default period is still owed and will be added to the principal balance. Rehabilitation can be a positive step toward restoring credit and avoiding further negative consequences, but it requires a significant commitment to making consistent on-time payments.

Options for Borrowers Facing Financial Hardship

Borrowers facing financial hardship have several options available to them to avoid default. These options include income-driven repayment plans, which adjust monthly payments based on income and family size; deferment, which temporarily suspends payments; and forbearance, which reduces or temporarily suspends payments. Contacting your loan servicer early and explaining your situation is crucial to exploring these options. It’s also advisable to seek professional financial guidance to create a realistic budget and repayment plan.

Resources for Borrowers Struggling with Repayment

Understanding the resources available can significantly aid borrowers in managing their student loan debt effectively.

- The National Foundation for Credit Counseling (NFCC): Provides free and low-cost credit counseling services, including assistance with student loan repayment.

- StudentAid.gov: The official website of the U.S. Department of Education’s Federal Student Aid program, offering information on repayment plans, loan forgiveness programs, and other resources.

- Your Loan Servicer: Contact your loan servicer directly to discuss your repayment options and explore potential solutions for financial hardship.

- The Federal Trade Commission (FTC): Provides information on debt collection practices and consumer rights.

Visual Representation of Repayment Schedules

Understanding your student loan repayment schedule is crucial for effective financial planning. A visual representation, typically in the form of an amortization schedule, provides a clear picture of your loan’s repayment journey. This allows you to track your progress, anticipate future payments, and make informed decisions about your finances.

Amortization schedules offer a detailed breakdown of each payment, showing how much goes towards principal and interest over the life of the loan. This clarity helps borrowers understand the dynamic relationship between their payments and the loan’s reduction.

Amortization Table Components

An amortization table typically includes three key components: principal, interest, and balance. The principal represents the original loan amount borrowed. Interest is the cost of borrowing money, calculated as a percentage of the outstanding balance. The balance is the remaining amount owed on the loan after each payment. Each row in the table represents a payment period (typically monthly), detailing the payment amount, the portion allocated to interest, the portion allocated to principal, and the remaining loan balance.

Hypothetical Amortization Schedule Illustrating Payment Amount Impact

Let’s consider a hypothetical $20,000 student loan with a 5% annual interest rate. We will illustrate two scenarios: one with a higher monthly payment and one with a lower monthly payment. The chart would have two lines, one for each payment scenario.

The X-axis of the chart would represent the month of repayment (from Month 1 to Month X, where X represents the total number of months to repay the loan). The Y-axis would represent the outstanding loan balance. The chart would show two lines.

Scenario 1: Higher Monthly Payment ($400)

This scenario would result in a shorter repayment period. The line representing this scenario on the graph would start at $20,000 (Month 1) and steadily decline, reaching zero significantly faster than the second scenario. Key data points to include would be the loan balance after 12 months, 24 months, 36 months, and the final month of repayment. For example, after 12 months, the balance might be around $15,000; after 24 months, it might be around $10,000.

Scenario 2: Lower Monthly Payment ($300)

This scenario would result in a longer repayment period and a higher total interest paid. The line representing this scenario would also begin at $20,000 (Month 1), but the decline would be slower. Similar key data points (12, 24, 36 months, and final month) should be included, showing the significantly higher remaining balance compared to Scenario 1 at each point. For example, after 12 months, the balance might be around $17,000; after 24 months, around $14,000. The final month of repayment would be considerably later than in Scenario 1.

The difference between the two lines clearly illustrates how a higher monthly payment significantly reduces the total repayment time and the overall interest paid over the life of the loan. The graph would visually demonstrate this relationship, allowing for a clear comparison between the two repayment strategies.

Wrap-Up

Successfully managing student loan repayment requires a proactive approach and a thorough understanding of the available options. By carefully considering your financial situation, exploring different repayment plans, and staying informed about potential consequences, you can develop a strategic repayment plan that aligns with your long-term financial goals. Remember, seeking professional advice can provide valuable guidance in navigating this complex process.

Key Questions Answered

What happens if I miss a student loan payment?

Missing payments can lead to late fees, damage your credit score, and potentially result in default, triggering serious consequences like wage garnishment.

Can I refinance my student loans?

Yes, refinancing can potentially lower your interest rate and monthly payment, shortening your repayment period. However, it’s crucial to compare offers and understand the terms before refinancing.

What are the benefits of making extra payments on my student loans?

Extra payments reduce the principal balance faster, leading to significant interest savings and a shorter repayment period. Even small extra payments can make a substantial difference over time.

How do I apply for an income-driven repayment plan?

The application process varies depending on your loan type and lender. You typically need to complete a form and provide documentation of your income and family size. Contact your loan servicer for specific instructions.