Navigating the world of student loans can feel overwhelming, particularly when understanding the nuances of subsidized loans. This guide offers a clear and concise path to securing the financial aid you need to pursue higher education. We’ll demystify the application process, from determining your eligibility to understanding repayment plans, ensuring you’re well-equipped to make informed decisions about your financial future.

Securing a subsidized student loan can significantly reduce the financial burden of higher education. This guide breaks down the entire process into manageable steps, providing you with the tools and knowledge necessary to successfully apply and manage your loan effectively. We will cover eligibility requirements, the FAFSA application, loan types, and repayment options, equipping you with a comprehensive understanding of the entire process.

Eligibility Requirements for Subsidized Student Loans

Securing a subsidized federal student loan requires meeting specific eligibility criteria. These loans are advantageous because the government pays the interest while you’re in school, during grace periods, and during periods of deferment. Understanding these requirements is crucial for a successful application. This section details the necessary steps to determine your eligibility.

General Eligibility Criteria

To be eligible for a subsidized federal student loan, you must be a U.S. citizen or eligible non-citizen, enrolled at least half-time in an eligible degree or certificate program at a participating institution, demonstrate financial need, and maintain satisfactory academic progress. You also must not have a default history on any federal student loans.

Income Requirements and Limitations

The Free Application for Federal Student Aid (FAFSA) determines your financial need based on your family’s income and assets. There isn’t a specific income cutoff, but the lower your family’s income, the more likely you are to qualify for subsidized loans. The FAFSA uses a complex formula considering factors like family size, number of dependents, and untaxed income. The information you provide on the FAFSA will determine your Expected Family Contribution (EFC). A lower EFC indicates greater financial need. High income earners are less likely to qualify for subsidized loans, often receiving unsubsidized loans instead.

Determining Individual Eligibility: A Step-by-Step Process

Let’s use a hypothetical example to illustrate the process. Imagine a student, Sarah, applying for a subsidized loan. She’s a U.S. citizen, enrolled full-time at State University, and maintains satisfactory academic progress. Her parents’ adjusted gross income (AGI) is $50,000, they have $20,000 in assets, and one dependent (Sarah).

1. Complete the FAFSA: Sarah submits her FAFSA form, accurately reporting all the required financial information.

2. Calculate the EFC: The Department of Education’s formula calculates Sarah’s EFC based on the information provided. This is a complex calculation factoring in her parents’ income, assets, and family size. The result will be a numerical value.

3. Compare EFC to Cost of Attendance: State University’s cost of attendance (tuition, fees, room, board, etc.) is $25,000. The difference between the cost of attendance and Sarah’s EFC represents her financial need. If the difference is positive, it suggests she may qualify for a subsidized loan.

4. Review Award Letter: Sarah receives a financial aid award letter from State University, detailing the types and amounts of financial aid offered, including any subsidized loans.

Eligibility Requirements Summary

| Requirement | Description | Example | Documentation Needed |

|---|---|---|---|

| U.S. Citizenship or Eligible Non-Citizen Status | Must be a U.S. citizen or meet specific immigration requirements. | U.S. Passport or Birth Certificate | Passport, Birth Certificate, Permanent Resident Card |

| Enrollment Status | Enrolled at least half-time in an eligible program. | Enrolled in 12 credit hours at an accredited college. | Acceptance letter, enrollment verification |

| Financial Need | Demonstrated need based on FAFSA information. | Low family income and assets, resulting in a low EFC. | Completed FAFSA |

| Satisfactory Academic Progress | Maintaining a minimum GPA and completing courses at a reasonable pace. | Maintaining a 2.0 GPA and completing at least 67% of required credits each year. | Academic transcripts |

| No Default History | No past federal student loan defaults. | Clean credit history related to federal student loans. | Credit report |

Completing the FAFSA (Free Application for Federal Student Aid)

The FAFSA, or Free Application for Federal Student Aid, is the gateway to accessing federal student financial aid, including subsidized loans. Completing this form accurately and thoroughly is crucial for maximizing your chances of receiving aid. Inaccurate information can lead to delays in processing your application or even ineligibility for aid.

The FAFSA requires detailed information about you, your family, and your financial situation. This data is used to determine your Expected Family Contribution (EFC), which influences the amount of financial aid you may receive. The process involves gathering necessary documents, carefully entering information into the online form, and reviewing your submission for accuracy.

FAFSA Completion Process

A systematic approach is key to successfully navigating the FAFSA. The following steps Artikel the typical process:

Imagine a flowchart with these steps: 1. Gather Required Documents; 2. Create FSA ID; 3. Begin FAFSA Application; 4. Provide Student Information; 5. Provide Parent Information (if applicable); 6. Provide Tax Information; 7. Review and Submit; 8. Track Application Status.

Providing Accurate Information

Providing accurate and up-to-date information is paramount. The FAFSA uses this information to calculate your EFC, which directly impacts your eligibility for financial aid. Any discrepancies or omissions can result in delays or denial of your application. It’s essential to double-check all entries before submitting the form. For example, using last year’s tax information instead of the most current data could significantly alter the calculated EFC. Similarly, misreporting income or assets could lead to over- or underestimation of your financial need, affecting your eligibility for aid.

Common Errors to Avoid

Several common mistakes can hinder the FAFSA process. Avoiding these errors ensures a smoother and more efficient application.

For instance, many students mistakenly enter their parents’ information incorrectly, especially when dealing with separated or divorced parents. Another common error is failing to report all income sources, including part-time jobs, investments, or parental support. Lastly, many applicants neglect to review and correct errors before submitting their application. This can lead to processing delays or rejection of the application.

Utilizing the FAFSA Website and Help Resources

The official FAFSA website provides comprehensive guidance and support throughout the application process. This includes access to FAQs, tutorials, and contact information for assistance. Utilizing these resources can help prevent errors and ensure a smooth application process. For example, the website offers step-by-step instructions, videos, and a helpline to address any queries or concerns that may arise during the application process.

Understanding Loan Types and Repayment Plans

Securing a subsidized federal student loan is a significant step towards financing your education. However, understanding the different loan types and repayment options is crucial for responsible borrowing and long-term financial well-being. This section clarifies the various loan types and repayment plans available, enabling you to make informed decisions about managing your student loan debt.

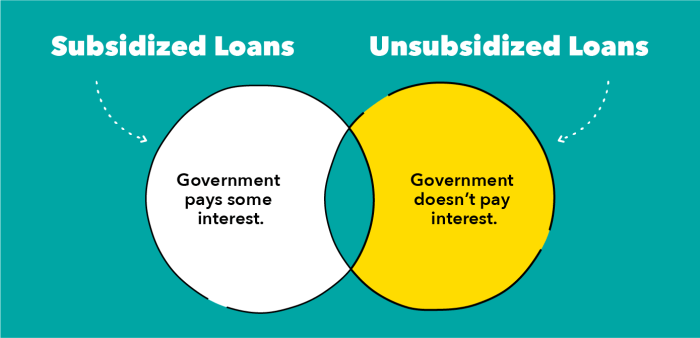

Federal Subsidized and Unsubsidized Loans

Subsidized and unsubsidized federal student loans are the primary loan types available to eligible students. The key difference lies in interest accrual. With subsidized loans, the government pays the interest while you’re in school at least half-time, during grace periods, and during deferment. Unsubsidized loans, however, accrue interest from the moment the loan is disbursed, regardless of your enrollment status. This means you’ll owe more at repayment if you don’t pay the accruing interest during your studies. Choosing between subsidized and unsubsidized loans depends on your financial need and ability to manage accruing interest. A student with demonstrated financial need will generally be offered a subsidized loan first.

Repayment Plan Options

After graduation, various repayment plans cater to different financial situations. Selecting the right plan significantly impacts your monthly payments and the total interest paid over the life of the loan. Careful consideration of your post-graduation income and financial goals is crucial.

- Standard Repayment Plan: This is the default plan, requiring fixed monthly payments over 10 years. It offers the shortest repayment period, leading to lower overall interest costs but higher monthly payments.

- Graduated Repayment Plan: Payments start low and gradually increase over time, making them more manageable initially but resulting in higher payments and total interest paid in the long run. This can be helpful for recent graduates anticipating income growth.

- Extended Repayment Plan: This plan extends the repayment period to up to 25 years, lowering monthly payments but significantly increasing total interest paid. This option is suitable for borrowers with lower incomes or high debt loads.

- Income-Driven Repayment (IDR) Plans: These plans, including Income-Based Repayment (IBR), Pay As You Earn (PAYE), Revised Pay As You Earn (REPAYE), and Income-Contingent Repayment (ICR), base monthly payments on your income and family size. Payments are typically lower than other plans, but repayment periods are longer, potentially leading to higher total interest costs. These plans often offer loan forgiveness after 20 or 25 years of payments, depending on the plan.

Implications of Repayment Plan Choices on Long-Term Financial Health

Choosing a repayment plan involves a trade-off between monthly payment affordability and total interest paid. For example, an Extended Repayment Plan will lower your monthly payments, making budgeting easier in the short term. However, this comes at the cost of paying significantly more interest over the life of the loan, impacting your long-term financial health. Conversely, a Standard Repayment Plan, while demanding higher monthly payments, minimizes total interest paid and accelerates debt elimination. Income-Driven Repayment plans offer a balance, prioritizing affordability while potentially leading to loan forgiveness after a significant period. Careful consideration of your current financial situation, income projections, and long-term financial goals is essential for selecting the most suitable repayment plan. A borrower with a high income and low debt might prefer a Standard Repayment plan to minimize interest, while someone with a lower income and higher debt might find an IDR plan more manageable.

The Loan Application Process

Submitting your subsidized student loan application is a crucial step in financing your education. This process involves several stages, from completing the necessary forms to receiving your loan disbursement. Understanding each step will help ensure a smooth and timely application.

Submitting the Loan Application

After completing the FAFSA and receiving your Student Aid Report (SAR), you’ll be notified of your eligibility for federal student aid, including subsidized loans. The actual loan application process typically happens through your chosen school’s financial aid office. They will provide you with instructions and forms specific to your institution and loan program. You will likely need to accept the offered loan amount through their online portal or by submitting a signed paper agreement. Be sure to carefully review all terms and conditions before signing.

The Verification Process

Your application may be selected for verification. This is a standard procedure to ensure the accuracy of the information you provided on your FAFSA. If selected, you will receive a notification requesting additional documentation, such as tax returns or W-2 forms. Providing these documents promptly is crucial to avoid delays in processing your loan application. Failure to respond within the specified timeframe could result in a delay or denial of your loan. The verification process is designed to protect both you and the government from errors.

Tracking Application Status

Most schools use online portals to manage student financial aid. You can usually access your application status through a student portal or the school’s financial aid website. This portal will typically show the progress of your application, including whether it’s been received, verified, and approved. Regularly checking your status updates is recommended to stay informed about the progress and address any potential issues promptly. Some systems may even send email or text notifications regarding significant changes in your application status.

Tips for a Smooth Application Process

Completing your FAFSA accurately and early is key. Submitting all required documents promptly during the verification process is also critical. Maintain open communication with your school’s financial aid office; they can answer your questions and provide assistance if you encounter any problems. Keep copies of all submitted documents for your records. Finally, carefully review all loan agreements before signing to understand the terms and conditions of your loan. Proactive communication and organization can significantly streamline the entire application process.

Understanding Loan Terms and Conditions

Securing a subsidized student loan involves understanding its specific terms and conditions. This knowledge is crucial for responsible borrowing and successful repayment. Failing to grasp these details can lead to unexpected financial burdens and potential difficulties down the line. This section will clarify key aspects to ensure a clear understanding before accepting a loan.

Interest Rates and Fees

Subsidized student loan interest rates are determined by the federal government and can vary depending on the loan type and the year the loan is disbursed. These rates are generally lower than unsubsidized loan rates. Fees associated with subsidized loans are typically minimal, but it’s essential to confirm any applicable fees with your lender. For example, the origination fee, a percentage of the loan amount, covers the administrative costs of processing the loan. It’s important to factor these costs into your overall borrowing plan. Understanding the exact interest rate and fees for your specific loan is crucial for accurate budgeting and financial planning.

Repayment Schedules and Options

Repayment for subsidized student loans typically begins six months after you cease being enrolled at least half-time in college. Several repayment plans are available, including standard repayment (fixed monthly payments over 10 years), extended repayment (longer repayment period), graduated repayment (payments start low and increase over time), and income-driven repayment (payments based on your income and family size). Choosing the right repayment plan depends on your individual financial circumstances and goals. For example, a standard repayment plan offers a shorter repayment period but higher monthly payments, while an income-driven repayment plan offers lower monthly payments but a longer repayment period.

Comparison of Loan Terms

The following table illustrates how different loan terms can impact your overall repayment. Note that these are examples and actual rates and terms can vary.

| Loan Term (Years) | Annual Interest Rate (Example) | Monthly Payment (Example, $10,000 Loan) | Total Interest Paid (Example) |

|---|---|---|---|

| 10 | 4.5% | $104 | $2,380 |

| 15 | 4.5% | $75 | $3,740 |

| 20 | 4.5% | $61 | $5,100 |

Consequences of Defaulting on a Student Loan

Defaulting on a student loan has serious financial consequences. This occurs when you fail to make payments for a certain period. The consequences can include damage to your credit score, wage garnishment, tax refund offset, and difficulty obtaining future loans or credit. In severe cases, it could even lead to legal action. For example, a damaged credit score can make it difficult to secure a mortgage, rent an apartment, or even get a job. It’s imperative to contact your loan servicer immediately if you anticipate difficulty making your payments to explore options like deferment or forbearance to avoid default.

Resources and Additional Support

Securing financial aid for higher education often involves navigating a complex system. Fortunately, numerous resources are available to assist students throughout the process, from application to repayment. Understanding these resources and knowing where to seek help can significantly ease the burden and increase your chances of securing the funding you need.

Reliable Resources for Financial Aid Assistance

Several organizations and government agencies provide comprehensive information and support for students seeking financial aid. These resources offer guidance on completing applications, understanding eligibility criteria, and exploring various funding options. Utilizing these resources can prove invaluable in the pursuit of higher education.

- Federal Student Aid (FSA): The primary source of information on federal student aid programs. Their website (studentaid.gov) provides detailed information on eligibility, application procedures, and loan repayment options. They also offer a wealth of educational materials and tools to assist students in making informed decisions.

- Your College or University’s Financial Aid Office: Each institution has a dedicated financial aid office that can provide personalized guidance based on your specific circumstances and the institution’s financial aid policies. They can answer questions about institutional aid, scholarships, and work-study opportunities.

- State Grant Agencies: Many states offer their own grant programs to supplement federal aid. Contact your state’s higher education agency to learn about available state-level financial aid opportunities.

- Nonprofit Organizations: Numerous nonprofit organizations offer scholarships and grants to students based on various criteria, such as academic merit, financial need, or specific fields of study. Examples include the Sallie Mae Foundation and the National Merit Scholarship Corporation.

Contact Information for Relevant Agencies and Institutions

Direct contact with relevant agencies and institutions can provide personalized assistance and address specific concerns. It’s important to note that contact information may vary depending on the institution or agency. Always refer to official websites for the most up-to-date details.

- Federal Student Aid (FSA): Contact information is readily available on their website, studentaid.gov.

- Your College or University’s Financial Aid Office: Contact information is typically found on the institution’s website, usually within the admissions or student services sections.

- State Grant Agencies: Contact information can be found through a web search for “[Your State] Higher Education Agency.”

Finding Scholarships and Grants

Scholarships and grants are crucial for supplementing student loans and reducing overall borrowing. A proactive search strategy is essential to maximize your chances of securing additional funding.

Numerous online databases and search engines specialize in connecting students with scholarships and grants. These resources often allow you to filter search results based on criteria such as major, academic achievement, and demographic factors. Furthermore, networking with your college’s career services office and advisors can often lead to less publicized scholarship opportunities. Remember to thoroughly research each opportunity and meet all eligibility requirements before applying.

Appealing a Loan Application Decision

If your student loan application is denied or you disagree with the terms offered, you have the right to appeal the decision. The appeal process typically involves submitting a written request to the lender or financial aid office, providing supporting documentation to justify your appeal. It’s crucial to carefully review the reasons for the denial and prepare a compelling case outlining why you believe the decision should be reconsidered. The specific procedures for appealing a loan application decision vary depending on the lender and the reasons for the denial. Detailed instructions are usually provided in the denial notification.

Visual Aid: Illustrating the Loan Process

A comprehensive infographic can significantly improve understanding of the often-complex student loan application process. By visually representing the key stages, timelines, and requirements, it simplifies navigation and reduces confusion for applicants. The infographic should aim for clarity and ease of understanding, using a clear, consistent design and readily digestible information.

Infographic Design and Content

The infographic should be designed chronologically, following the natural progression of the loan application. A clear visual pathway, perhaps using arrows or connecting lines, will guide the viewer through each step. The overall aesthetic should be clean and uncluttered, using a limited color palette for maximum impact. Consider using icons and symbols to represent key concepts, enhancing comprehension and visual appeal. The use of charts or graphs to represent data, such as average loan amounts or repayment periods, could further enhance understanding.

Key Stages and Timelines Depicted in the Infographic

The infographic will visually represent the following key stages:

- Eligibility Check: This section will illustrate the criteria for eligibility, such as enrollment status, citizenship, and credit history (where applicable). A checklist or flowchart could be used to visually represent these requirements. The timeline here would indicate the time it takes to determine eligibility, typically a few days to a few weeks depending on the application’s completeness and the processing institution’s workload.

- FAFSA Completion: This section should visually represent the FAFSA form, possibly with a simplified version or key fields highlighted. The timeline would show the typical processing time for the FAFSA, usually several weeks. A note indicating the importance of accuracy and completeness would also be included.

- Loan Application Submission: This section will visually represent the online submission process. It might show a screenshot of the application portal or a simplified representation of the steps involved. The timeline would indicate the typical processing time for the loan application itself, usually a few weeks to a month.

- Loan Approval/Disbursement: This section will show the notification process and the disbursement of funds. A timeline would indicate the typical time it takes for funds to be disbursed, usually within a few weeks of approval. A visual representation of the disbursement process, showing the transfer of funds to the student’s account, would be beneficial.

- Repayment Plan Selection: This section will visually represent the different repayment plans available, perhaps using a table or chart to compare key features. Examples of repayment plan options (e.g., Standard, Graduated, Income-Driven) will be clearly Artikeld. The section will also show how to choose the most suitable plan based on individual circumstances.

- Repayment Process: This section will visually represent the ongoing repayment process, including methods of payment (online, mail, etc.) and contact information for loan servicers. A timeline illustrating a sample repayment schedule, showing the amortization of the loan, would be beneficial.

Data Representation and Visual Cues

The infographic will use visual cues such as color-coding to differentiate stages and timelines. For example, green could indicate completion, while yellow could represent ongoing processes. Red could highlight potential delays or critical points requiring attention. Data, such as average loan amounts and interest rates, should be presented in easily digestible formats like bar graphs or pie charts, ensuring accurate representation of the information. For example, a bar graph comparing the average loan amounts for undergraduate and graduate students could provide a relevant visual representation of the data.

Closing Notes

Successfully applying for subsidized student loans requires careful planning and attention to detail. By following the steps Artikeld in this guide, understanding your eligibility, and completing the FAFSA accurately, you can significantly increase your chances of securing the financial assistance you need for your education. Remember to thoroughly review your loan terms and conditions, explore different repayment plans, and utilize available resources to make the most informed decisions for your financial well-being. Your future success begins with a solid understanding of your financial options.

Question Bank

What is the difference between subsidized and unsubsidized loans?

Subsidized loans don’t accrue interest while you’re in school, grace periods, or deferment. Unsubsidized loans accrue interest throughout the entire loan period.

What happens if I don’t complete the FAFSA accurately?

Inaccurate information can delay or prevent your loan approval. It’s crucial to provide correct and up-to-date information.

Can I appeal a loan application decision?

Yes, you can appeal a loan application decision if you believe there was an error or oversight. Contact the relevant agency for details on the appeal process.

What if I can’t afford my loan payments after graduation?

Explore repayment options like income-driven repayment plans, which adjust payments based on your income and family size. Contact your loan servicer to discuss your options.