Navigating the world of student loans can feel overwhelming, but understanding your options is crucial for a successful academic journey. This guide provides a comprehensive overview of student loan types, eligibility requirements, repayment plans, and strategies for effective debt management. We’ll explore both federal and private loans, highlighting key differences and helping you make informed decisions about financing your education.

From understanding FAFSA applications to exploring loan forgiveness programs and alternative funding sources like scholarships and grants, this resource aims to equip you with the knowledge needed to secure funding and plan for your financial future. We’ll delve into the long-term implications of student loan debt, offering practical advice on budgeting and responsible borrowing.

Types of Student Loans

Choosing the right student loan is crucial for financing your education. Understanding the differences between federal and private loans, and the various types of federal loans available, will help you make an informed decision and avoid potential financial pitfalls. This section will Artikel the key features of each type of loan to aid in your selection process.

Federal and private student loans offer different benefits and drawbacks. Federal loans generally offer more borrower protections, while private loans may have more stringent eligibility requirements.

Federal vs. Private Student Loans

The following table compares federal and private student loans across key characteristics. Remember that specific terms and conditions can vary depending on the lender and the year.

| Feature | Federal Student Loans | Private Student Loans | Notes |

|---|---|---|---|

| Eligibility | Generally available to US citizens and eligible non-citizens who meet certain academic requirements. | Based on creditworthiness, income, and debt-to-income ratio. Co-signer may be required. | Federal loans have broader eligibility. |

| Interest Rates | Fixed rates set by the government; generally lower than private loans. | Variable or fixed rates; typically higher than federal loan rates. | Interest rates fluctuate based on market conditions for private loans. |

| Repayment Options | Variety of repayment plans available, including income-driven repayment plans. | Fewer repayment options compared to federal loans; often less flexible. | Income-driven repayment plans can significantly lower monthly payments for federal loans. |

| Loan Forgiveness Programs | Eligibility for certain loan forgiveness programs (e.g., Public Service Loan Forgiveness). | Generally not eligible for federal loan forgiveness programs. | Federal loan forgiveness programs can reduce or eliminate loan debt under specific circumstances. |

Types of Federal Student Loans

The federal government offers several types of student loans, each with its own set of features and eligibility criteria. Understanding these differences is key to selecting the most appropriate loan for your financial situation.

- Subsidized Loans: The government pays the interest while you are in school at least half-time, during grace periods, and during periods of deferment. Eligibility is based on financial need.

- Unsubsidized Loans: Interest accrues from the time the loan is disbursed, regardless of your enrollment status. You are responsible for paying this interest. Eligibility is not based on financial need.

- PLUS Loans: Loans available to graduate and professional students, as well as parents of undergraduate students. Credit checks are required, and borrowers must meet certain creditworthiness standards. Interest rates are typically higher than subsidized and unsubsidized loans.

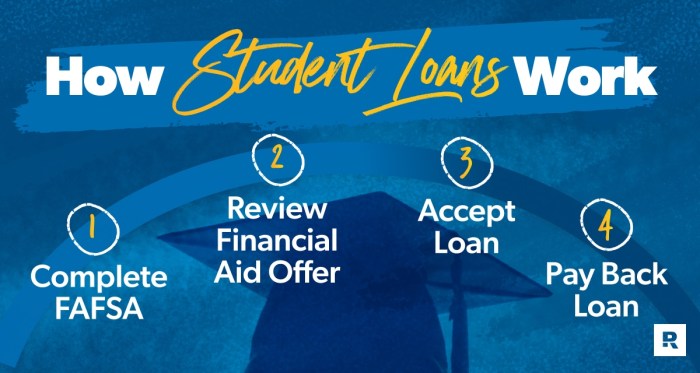

Federal Student Loan Application Process

The application process for federal student loans involves several key steps. This flowchart illustrates a simplified version of the process.

Flowchart: The process begins with completing the Free Application for Federal Student Aid (FAFSA). This form determines your eligibility for federal aid. Upon completion and submission, the FAFSA is processed, and you receive a Student Aid Report (SAR). Next, you select a loan and complete the Master Promissory Note (MPN). Finally, the loan funds are disbursed to your educational institution. Any discrepancies or additional information requests will necessitate revisiting prior steps in the process. This is a simplified representation; the actual process may involve additional steps or complexities depending on individual circumstances.

Interest Rates and Repayment Plans

Understanding interest rates and repayment options is crucial for managing your student loan debt effectively. Choosing the right loan and repayment plan can significantly impact your overall cost and long-term financial health. This section will clarify the complexities of interest rates and repayment plans to help you make informed decisions.

Interest Rates for Student Loans

Several factors influence the interest rate you’ll receive on a student loan. These include your credit score (if applicable), the type of loan (federal or private), and the lender. Generally, federal student loans offer lower, fixed interest rates than private loans, which often have variable rates that can fluctuate over time. A higher credit score typically qualifies you for a lower interest rate on private loans. The following table provides a comparison, though these rates are subject to change and should be verified with the respective lenders.

| Loan Type | Interest Rate Range (Example) |

|---|---|

| Federal Subsidized Loan | 4.5% – 7.5% |

| Federal Unsubsidized Loan | 4.5% – 7.5% |

| Private Student Loan (Good Credit) | 5% – 10% |

| Private Student Loan (Fair Credit) | 10% – 15% |

Note: The interest rate ranges provided are examples and may not reflect current rates. Always check with individual lenders for the most up-to-date information.

Student Loan Repayment Plans

Several repayment plans are available to help borrowers manage their student loan debt. The best option depends on individual financial circumstances and repayment preferences.

Standard Repayment

This plan involves fixed monthly payments over a 10-year period. It’s a straightforward approach, but payments can be substantial, especially for large loan amounts.

Graduated Repayment

Payments start low and gradually increase over time, typically over a 10-year period. This option may provide relief in the early years, but payments become larger later.

Income-Driven Repayment (IDR) Plans

These plans base your monthly payment on your income and family size. Several IDR plans exist, each with different eligibility criteria and payment calculation methods. These plans generally extend the repayment period beyond 10 years, potentially resulting in higher total interest paid. Examples include Income-Based Repayment (IBR), Pay As You Earn (PAYE), and Revised Pay As You Earn (REPAYE).

Interest Capitalization

Interest capitalization occurs when unpaid interest is added to your principal loan balance. This increases the total amount you owe, leading to higher overall interest payments. For example, if you have a $10,000 loan with a 5% interest rate and don’t make payments for a year, $500 in interest would be capitalized, increasing your principal to $10,500. This process can significantly impact your total loan cost over the life of the loan, especially if you defer or forbear payments. Understanding this process is vital for effective debt management.

Managing Student Loan Debt

Successfully navigating student loan repayment requires proactive planning and consistent effort. Understanding your loan terms, developing a realistic budget, and establishing good financial habits are crucial for avoiding the potential negative consequences of loan default. This section provides strategies for effectively managing your student loan debt and highlights the serious implications of failing to meet your repayment obligations.

Strategies for Budgeting and Managing Student Loan Debt

Effective student loan management hinges on creating and adhering to a comprehensive budget. This involves carefully tracking income and expenses to identify areas for potential savings and allocate sufficient funds for loan repayment. Failing to plan can lead to missed payments, accumulating interest, and ultimately, financial distress.

- Create a Detailed Budget: Track all income sources and meticulously list every expense, categorizing them (housing, food, transportation, entertainment, etc.). This provides a clear picture of your current financial situation.

- Prioritize Loan Repayment: Treat your student loan payments as a non-negotiable expense, similar to rent or utilities. Automate payments whenever possible to ensure consistent repayment.

- Explore Repayment Plans: Investigate different repayment options offered by your loan servicer, such as income-driven repayment plans, which adjust your monthly payment based on your income and family size. This can make repayment more manageable during periods of lower income.

- Reduce Unnecessary Expenses: Identify areas where you can cut back on spending. This might involve reducing dining out, limiting entertainment expenses, or finding more affordable transportation options.

- Build an Emergency Fund: Having 3-6 months’ worth of living expenses saved can provide a financial buffer in case of unexpected job loss or medical emergencies, preventing loan payment disruptions.

- Consider Refinancing: If interest rates have fallen since you took out your loans, refinancing could lower your monthly payments and save you money in the long run. However, carefully compare offers and fees before making a decision.

Consequences of Defaulting on Student Loans

Defaulting on student loans has severe and long-lasting financial consequences. It’s crucial to understand these implications to emphasize the importance of responsible repayment.

- Damaged Credit Score: Defaulting significantly lowers your credit score, making it difficult to obtain loans, credit cards, or even rent an apartment in the future.

- Wage Garnishment: The government can garnish your wages to recover the debt, leaving you with significantly reduced income.

- Tax Refund Offset: Your tax refund can be seized to pay off your defaulted loans.

- Difficulty Obtaining Future Loans: A history of loan default will make it extremely challenging to secure future loans for major purchases like a car or a house.

- Collection Agency Involvement: Your debt may be sold to a collection agency, which will aggressively pursue repayment, potentially leading to further financial stress.

Sample Budget for Student Loan Repayment

This sample budget illustrates how to allocate funds for student loan repayment alongside other essential expenses. Remember that this is a template; your specific budget will depend on your individual income and expenses.

| Income | Expense | Amount |

|---|---|---|

| Monthly Salary | Student Loan Payment | $500 |

| Part-time Job Income | Rent/Mortgage | $1000 |

| Total Income: $3500 | Utilities (Electricity, Water, Gas) | $200 |

| Groceries | $300 | |

| Transportation | $150 | |

| Health Insurance | $100 | |

| Savings | $250 | |

| Other Expenses (Entertainment, etc.) | $500 | |

| Total Expenses: $2500 | ||

| Net Income: $1000 |

Loan Forgiveness and Consolidation

Navigating the complexities of student loan repayment can feel daunting, but understanding options like loan forgiveness and consolidation can significantly impact your financial future. These strategies offer potential relief from the burden of student loan debt, allowing for more manageable repayment schedules or even complete debt elimination under specific circumstances.

Loan forgiveness and consolidation represent two distinct yet sometimes complementary approaches to managing student loan debt. Understanding the nuances of each can empower you to make informed decisions about your repayment strategy.

Loan Forgiveness Programs

Several federal and state programs offer loan forgiveness for individuals working in specific public service sectors or meeting certain criteria. These programs typically require a period of qualifying employment and adherence to specific repayment plans. The amount of loan forgiveness varies depending on the program and the borrower’s circumstances.

For example, the Public Service Loan Forgiveness (PSLF) program forgives the remaining balance on Direct Loans after 120 qualifying monthly payments under an income-driven repayment plan while working full-time for a qualifying government or non-profit organization. Teacher Loan Forgiveness programs offer partial loan forgiveness to teachers who meet specific requirements, such as teaching in low-income schools for a certain number of years. Other programs may exist at the state level, offering incentives for professionals in high-demand fields like healthcare or education. It’s crucial to research the specific eligibility requirements for each program as they can be complex and vary over time.

Student Loan Consolidation

Consolidating multiple student loans involves combining them into a single loan with a new interest rate and repayment plan. This simplifies repayment by reducing the number of monthly payments and potentially lowering the monthly payment amount. The process typically involves applying through a federal student loan consolidation program or a private lender.

Understanding the advantages and disadvantages is crucial before making a decision.

- Advantages:

- Simplified repayment: One monthly payment instead of multiple payments.

- Potentially lower monthly payments (though this depends on the new interest rate and repayment term).

- Fixed interest rate: Avoids fluctuating interest rates if you have variable-rate loans.

- Streamlined communication: Dealing with only one lender.

- Disadvantages:

- Potentially higher total interest paid over the life of the loan: A longer repayment term may result in paying more interest overall.

- Loss of benefits from certain repayment plans: Consolidating loans may eliminate eligibility for income-driven repayment plans or loan forgiveness programs.

- Higher interest rate: The new interest rate may be higher than the lowest rate on your existing loans.

- Lengthier repayment period: Extending the repayment term might result in longer debt repayment.

The Impact of Student Loans on Future Finances

Navigating the complexities of student loan debt requires a clear understanding of its long-term financial ramifications. The decisions made today regarding borrowing and repayment will significantly shape your financial future, influencing everything from your creditworthiness to your ability to achieve major life goals. Understanding these implications is crucial for making informed choices.

Student loan debt can exert a considerable influence on your financial trajectory for years to come. The amount borrowed, the interest rate, and the chosen repayment plan all play significant roles in determining the overall cost and the impact on your financial well-being. Failure to manage this debt effectively can lead to serious consequences, impacting your credit score, limiting future borrowing opportunities, and delaying the achievement of significant financial milestones.

Credit Scores and Future Borrowing Capacity

Student loan debt directly affects your credit score. Consistent on-time payments demonstrate responsible borrowing behavior, positively impacting your credit score. Conversely, missed or late payments can severely damage your creditworthiness, making it more difficult to secure loans or credit cards in the future, at potentially higher interest rates. A low credit score can also limit access to favorable terms on mortgages, auto loans, and even insurance policies. For example, a borrower with a consistently poor payment history might face significantly higher interest rates on a mortgage, increasing the overall cost of homeownership.

Impact on Major Life Decisions

The burden of student loan debt can significantly impact major life decisions. For instance, the monthly payments required to repay student loans can reduce the amount of money available for a down payment on a house, potentially delaying homeownership or requiring a smaller, less desirable property. Similarly, the financial strain of loan repayments might postpone starting a family, impacting family planning decisions. A young couple might delay having children because of the substantial financial responsibility of student loan repayment, preferring to prioritize debt reduction before taking on the significant expenses of raising a family.

Hypothetical Scenario: Loan Repayment Strategies

Consider two hypothetical graduates, both with $50,000 in student loan debt at a 6% interest rate. Graduate A chooses a standard repayment plan with a 10-year term, while Graduate B opts for an income-driven repayment plan. Graduate A will have higher monthly payments but will pay off the loan quicker, minimizing the total interest paid. Graduate B will have lower monthly payments, but the loan will take longer to repay, resulting in significantly more interest paid over the loan’s lifetime. After 10 years, Graduate A may be debt-free, while Graduate B might still have a substantial balance remaining. This illustrates how different repayment strategies can dramatically affect long-term financial well-being, impacting savings, investment opportunities, and overall financial security.

Alternative Funding Options for Students

Securing funding for higher education can be a significant challenge, but thankfully, student loans aren’t the only avenue. A range of alternative funding options exist, offering students diverse ways to finance their studies and potentially reduce their reliance on loans with their associated interest and repayment burdens. Exploring these alternatives can lead to significant long-term financial benefits.

Many students successfully fund their education through a combination of loans and alternative sources. Understanding the various options available and their respective advantages and disadvantages is crucial for making informed financial decisions.

Scholarships, Grants, and Work-Study Programs

Scholarships, grants, and work-study programs represent valuable alternative funding sources that don’t require repayment. These options can significantly reduce the need for student loans, lessening the financial burden after graduation. Each option offers unique benefits and eligibility criteria.

- Scholarships: Merit-based or need-based awards offered by various organizations, including colleges, universities, private foundations, and corporations. These often require applications and may consider academic achievement, extracurricular activities, or demonstrated financial need.

- Grants: Need-based financial aid provided by the government (e.g., Pell Grants) or private organizations. Eligibility is typically determined by factors such as family income and assets. Grants do not need to be repaid.

- Work-Study Programs: Federally funded programs that provide part-time jobs to students with financial need. Earnings can help cover educational expenses, reducing the need for loans.

Comparison of Student Loans and Alternative Funding Options

A direct comparison highlights the key differences between student loans and alternative funding options, enabling students to make informed decisions about how to finance their education.

| Feature | Student Loans | Alternative Funding (Scholarships, Grants, Work-Study) |

|---|---|---|

| Source of Funds | Financial institutions, government programs | Colleges, universities, private organizations, government programs |

| Repayment | Required, with interest accruing over time | Generally not required |

| Eligibility | Generally based on creditworthiness (sometimes co-signer needed) | Based on academic merit, financial need, or employment availability |

| Impact on Future Finances | Can lead to significant debt and affect credit score | Minimizes debt and improves long-term financial health |

| Application Process | Often involves credit checks and extensive paperwork | Can involve applications, essays, and documentation of financial need or merit |

Visual Representation of Financial Aid Options

Imagine a large circle representing total educational costs. Within this circle, several smaller, overlapping circles represent different funding sources. One large segment is labeled “Student Loans,” showing a significant portion of the total cost. Smaller, overlapping segments represent “Scholarships,” “Grants,” and “Work-Study,” illustrating how these options can reduce the reliance on loans. A smaller segment might also represent “Savings/Family Contributions.” The overlapping areas show that students often use a combination of funding sources to cover their educational expenses. The size of each segment could be adjusted to reflect the relative contribution of each funding source for a typical student, or even for specific examples of student funding plans.

Final Thoughts

Securing funding for higher education is a significant step, and understanding the nuances of student loans is paramount. By carefully considering the various loan types, eligibility criteria, and repayment options, you can create a financial plan that supports your academic goals without compromising your long-term financial well-being. Remember to explore alternative funding options and prioritize responsible debt management to build a secure financial future.

Questions Often Asked

What is the difference between subsidized and unsubsidized federal student loans?

Subsidized loans don’t accrue interest while you’re in school, grace periods, or deferment. Unsubsidized loans accrue interest from the time the loan is disbursed.

Can I refinance my student loans?

Yes, refinancing can lower your interest rate and monthly payment, but it often involves private lenders and may affect your eligibility for federal loan forgiveness programs.

What happens if I default on my student loans?

Defaulting can severely damage your credit score, leading to difficulty securing loans, credit cards, or even renting an apartment. Wage garnishment and tax refund offset are also possible consequences.

How long does it take to repay student loans?

The repayment period varies depending on the loan type and repayment plan chosen. Standard plans typically last 10 years, but income-driven plans can extend repayment over a longer period.

Where can I find more information about loan forgiveness programs?

The Federal Student Aid website (studentaid.gov) and your loan servicer are excellent resources for information on loan forgiveness programs.