Understanding your student loan interest rates is crucial for effective debt management. This guide delves into the intricacies of MOHELA student loan interest rates, exploring the factors that influence them, how to find this vital information, and strategies for minimizing your overall interest payments. We’ll navigate the complexities of different loan types, repayment plans, and the role of credit history in shaping your interest rate.

From deciphering MOHELA’s website to comparing their rates with other servicers, we aim to equip you with the knowledge and tools to make informed decisions about your student loan repayment journey. This comprehensive overview will empower you to take control of your financial future and strategically manage your debt.

Understanding MOHELA’s Role in Student Loan Servicing

MOHELA, the Missouri Higher Education Loan Authority, is a large student loan servicer playing a significant role in the federal student loan repayment process. It manages various aspects of borrowers’ accounts, helping them navigate repayment and ultimately achieve loan forgiveness. Understanding MOHELA’s functions is crucial for borrowers seeking clarity and efficient management of their student loan debt.

MOHELA’s primary function is to act as an intermediary between student loan borrowers and the federal government. This involves processing payments, providing customer service, managing account information, and explaining repayment options. They also handle communications regarding loan forgiveness programs and other relevant updates. In essence, they are responsible for the day-to-day management of a significant portion of the federal student loan portfolio.

Types of Student Loans Serviced by MOHELA

MOHELA services a range of federal student loans, including Direct Subsidized Loans, Direct Unsubsidized Loans, Direct PLUS Loans (for both graduate and undergraduate students), and Direct Consolidation Loans. The specific types of loans MOHELA manages can vary over time as the Department of Education reassigns loan portfolios among servicers. Borrowers should always check their loan servicer’s website or their official loan documents to confirm which servicer manages their specific loans.

MOHELA Servicing Fees

MOHELA does not charge borrowers any servicing fees. The fees associated with federal student loans are paid by the federal government, not the borrower. This is a key distinction between federal and private student loans, where private lenders may charge various fees. Therefore, borrowers should be aware that any fees charged are not directly from MOHELA, but may be related to other aspects of loan management not directly controlled by the servicer.

Comparison of MOHELA with Other Major Student Loan Servicers

The following table compares MOHELA to other prominent student loan servicers. It’s important to note that the features and contact information of these servicers can change, so it’s recommended to check their official websites for the most up-to-date information.

| Servicer Name | Loan Types Serviced | Contact Information | Notable Features |

|---|---|---|---|

| MOHELA | Direct Subsidized, Unsubsidized, PLUS, and Consolidation Loans (may vary) | (Check MOHELA’s official website for current contact information) | No servicing fees; often praised for online account management tools |

| Navient | Variety of federal and private student loans (may vary) | (Check Navient’s official website for current contact information) | Large servicer with extensive online resources; has faced past criticism regarding servicing practices |

| Nelnet | Variety of federal and private student loans (may vary) | (Check Nelnet’s official website for current contact information) | Strong online platform; offers various repayment plan options |

| Great Lakes | Variety of federal student loans (may vary) | (Check Great Lakes’ official website for current contact information) | Known for its customer service; offers various repayment plan options |

Factors Influencing MOHELA Student Loan Interest Rates

Several key factors interact to determine the interest rate you’ll receive on your MOHELA-serviced student loans. These rates aren’t set arbitrarily; they’re influenced by both your individual circumstances and broader economic conditions. Understanding these factors can help you make informed decisions about your loan options and repayment strategies.

Loan Type and Interest Rates

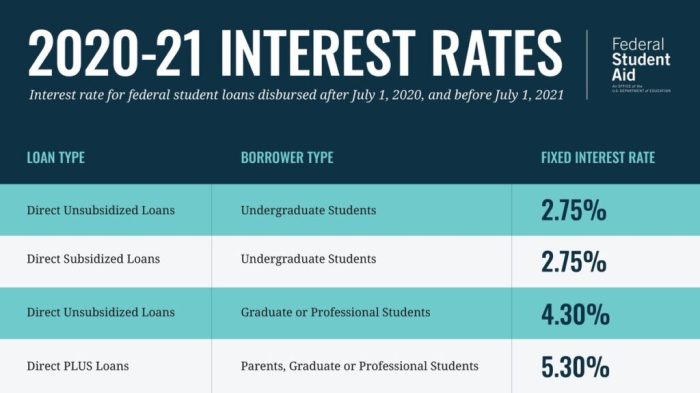

The type of federal student loan you have significantly impacts your interest rate. Subsidized loans, typically awarded based on financial need, have a unique feature: the government pays the interest while you’re in school at least half-time, during grace periods, and during periods of deferment. Unsubsidized loans, on the other hand, accrue interest from the moment the loan is disbursed, regardless of your enrollment status. This means that unsubsidized loans generally carry a higher total cost due to accumulated interest. The interest rate itself is set annually by the federal government and varies depending on the loan’s disbursement date. For example, a subsidized Direct Subsidized Loan might have a lower interest rate than an unsubsidized Direct Unsubsidized Loan disbursed in the same year.

Credit History and Interest Rates

While federal student loan interest rates aren’t directly determined by your credit history in the same way as private loans, a poor credit history can indirectly affect your borrowing experience. A low credit score might make it more challenging to secure favorable terms on future loans or refinancing options. Maintaining a good credit history is important for overall financial well-being, even if it doesn’t directly impact your initial federal student loan interest rate.

Repayment Plans and Total Interest Paid

The repayment plan you choose significantly impacts the total amount of interest you pay over the life of your loan. A shorter repayment term, such as a 10-year plan, will result in higher monthly payments but lower overall interest costs. Conversely, longer repayment terms, like the Income-Driven Repayment (IDR) plans, result in lower monthly payments but significantly higher total interest paid over the loan’s lifetime. For example, choosing a standard 10-year repayment plan for a $30,000 loan with a 5% interest rate will result in a lower total interest paid compared to a 20-year IDR plan, although the monthly payments will be substantially higher. The choice depends on individual financial priorities and long-term financial goals.

Current MOHELA Interest Rates and Their Variations

Understanding the current interest rates offered by MOHELA is crucial for borrowers to effectively manage their student loan repayment. These rates fluctuate based on several factors, including the type of loan, the repayment plan selected, and prevailing market conditions. It’s important to note that the information provided here is for illustrative purposes and may not reflect the most current rates. Always refer to the official MOHELA website for the most up-to-date information.

MOHELA’s interest rates are not publicly displayed in a single, easily accessible table. Instead, they are determined individually based on several factors including the borrower’s credit history and the loan terms. This means that a precise, comprehensive table showing every possible rate is impossible to create here. However, we can provide a representative sample of potential rate ranges and illustrate the variations that exist.

MOHELA Interest Rate Examples and Variations

The following table provides hypothetical examples to illustrate the potential range of interest rates and total interest paid under different scenarios. Remember that these are examples only and your actual interest rate will vary.

| Loan Type | Interest Rate (Example) | Repayment Plan | Total Interest Paid (Example) |

|---|---|---|---|

| Direct Subsidized Loan | 4.5% | Standard 10-year | $2,500 |

| Direct Unsubsidized Loan | 5.5% | Standard 10-year | $3,200 |

| Direct PLUS Loan | 7.0% | Standard 10-year | $4,500 |

| Direct Subsidized Loan | 4.5% | Income-Driven Repayment (IDR) | $3,000 |

| Direct Unsubsidized Loan | 5.5% | Income-Driven Repayment (IDR) | $3,800 |

It is important to note that the total interest paid is significantly influenced by the repayment plan. Income-Driven Repayment (IDR) plans, while potentially lowering monthly payments, often result in a higher total interest paid over the life of the loan due to the extended repayment period. Standard repayment plans generally have higher monthly payments but lower total interest paid.

Visual Representation of Interest Rate Range

Imagine a bar graph. The horizontal axis represents the different loan types (e.g., Direct Subsidized, Direct Unsubsidized, Direct PLUS). The vertical axis represents the interest rate percentage. Each loan type would have a bar extending upward to represent its potential interest rate range. For example, Direct Subsidized loans might have a bar ranging from 4% to 5%, while Direct PLUS loans might range from 6% to 8%. This visual would clearly illustrate the variation in interest rates across different loan types. The graph would visually show that PLUS loans generally carry the highest interest rates, followed by unsubsidized loans, with subsidized loans having the lowest rates. The visual would also emphasize that even within each loan type, a range of interest rates is possible.

Navigating MOHELA’s Interest Rate Information

Understanding your MOHELA student loan interest rate is crucial for effective repayment planning. Knowing your rate allows you to accurately project your total repayment costs and make informed decisions about your repayment strategy. This section will guide you through finding, interpreting, and calculating your interest costs.

Locating Current Interest Rate Information on the MOHELA Website

Finding your current interest rate on the official MOHELA website typically involves logging into your online account. Once logged in, navigate to your loan details section. The interest rate should be clearly displayed alongside other key loan information such as your loan balance, payment due date, and repayment plan. If you cannot locate this information, contact MOHELA’s customer service for assistance. They can provide clarification and ensure you have access to all the necessary details. Remember to regularly check your account for any updates or changes to your interest rate.

Interpreting MOHELA’s Interest Rate Information

MOHELA typically displays interest rates as an annual percentage rate (APR). This is the yearly cost of borrowing, expressed as a percentage of the principal loan amount. The APR reflects the total cost of borrowing, including any fees or other charges associated with the loan. Understanding this APR is essential to compare different loan options or to evaluate the overall cost of your student loan. It’s important to note that the interest rate may be fixed or variable, depending on the type of loan you have. A fixed rate remains constant throughout the loan’s life, while a variable rate can fluctuate based on market conditions. The type of rate will be clearly stated within your loan details.

Calculating Total Interest Paid Over the Loan’s Lifetime

Calculating the total interest paid over the life of your loan requires understanding your loan’s principal balance, interest rate, and repayment period. A simple (though not entirely precise without considering compounding) calculation can provide a reasonable estimate.

Total Interest ≈ (Monthly Payment × Number of Months) – Principal Loan Amount

For example, let’s say you have a $10,000 loan with a 5% annual interest rate and a 10-year repayment plan. Your monthly payment might be approximately $106.07. The total amount repaid over 10 years (120 months) would be approximately $12,728.40. Therefore, the estimated total interest paid would be approximately $2,728.40 ($12,728.40 – $10,000). Remember that this is a simplified calculation; the actual interest paid may vary slightly due to compounding and other factors. More precise calculations can be done using online loan calculators or financial software.

Understanding Your Individual Interest Rate

Understanding your individual interest rate is straightforward once you have access to your loan details. Here’s a step-by-step guide:

- Log in to your MOHELA account: Access your account through the official MOHELA website.

- Navigate to your loan details: Look for a section displaying your loan information, typically including loan balance, payment schedule, and interest rate.

- Locate your interest rate: The interest rate will usually be expressed as an annual percentage rate (APR) and indicated as either fixed or variable.

- Note the type of interest rate: Understand if your rate is fixed (remains constant) or variable (subject to change).

- Review your loan terms: Familiarize yourself with the loan’s terms, including the repayment period and any associated fees that may impact the overall cost.

Strategies for Managing MOHELA Student Loan Interest

Managing your MOHELA student loan interest effectively requires a proactive approach. Understanding your repayment options and exploring strategies to minimize interest payments can significantly impact your overall debt burden and long-term financial health. This section Artikels several key strategies to help you navigate this process successfully.

Minimizing Interest Payments on MOHELA Loans

Several strategies can help borrowers minimize the amount of interest paid on their MOHELA student loans. Making extra payments, even small ones, can substantially reduce the principal balance faster, leading to less interest accrued over the life of the loan. Another effective approach is to consolidate multiple loans into a single loan with a potentially lower interest rate. Careful budgeting and prioritizing loan payments can also ensure consistent and timely payments, avoiding late fees and penalties that increase the overall cost of borrowing. Finally, exploring income-driven repayment plans can lower monthly payments, although it may extend the repayment period and increase total interest paid over time. The optimal approach will depend on individual circumstances and financial goals.

Benefits and Drawbacks of Different Repayment Plans

MOHELA offers various repayment plans, each with its own benefits and drawbacks regarding interest. Standard repayment plans typically have the shortest repayment period, leading to less interest paid overall, but also higher monthly payments. Income-driven repayment (IDR) plans, such as the Income-Based Repayment (IBR), Pay As You Earn (PAYE), and Revised Pay As You Earn (REPAYE) plans, adjust monthly payments based on income and family size, resulting in lower monthly payments but potentially extending the repayment period and increasing total interest paid over time. Extended repayment plans stretch payments over a longer period, reducing monthly payments but increasing total interest paid. The best plan depends on the borrower’s financial situation and long-term goals. For example, a borrower with a low income might choose an IDR plan to manage monthly expenses, while a borrower with a higher income and stable employment might prefer a standard plan to pay off their loans faster.

Impact of Refinancing on Interest Rates

Refinancing your MOHELA student loans involves replacing your existing loans with a new loan from a private lender. This can potentially lower your interest rate, especially if current market rates are lower than your original loan rates. However, refinancing carries potential drawbacks. It might eliminate federal protections such as income-driven repayment plans or loan forgiveness programs. Additionally, refinancing often requires a good credit score, and borrowers with less-than-perfect credit may not qualify for the most favorable rates. Before refinancing, carefully compare the new interest rate and terms with your existing loan terms to determine if it is financially beneficial. For instance, a borrower with a high credit score and a significant amount of student loan debt might find refinancing advantageous, resulting in substantial interest savings over the life of the loan. Conversely, a borrower with a lower credit score and limited income might find that the benefits of refinancing are outweighed by the risks.

Resources for Managing Student Loan Debt

Several resources are available to assist borrowers in managing their student loan debt. The MOHELA website provides detailed information on repayment plans, interest rates, and other relevant information. The Federal Student Aid website (studentaid.gov) offers comprehensive resources and tools for managing federal student loans. Non-profit credit counseling agencies can provide free or low-cost guidance on debt management strategies. Finally, financial advisors can offer personalized advice based on individual circumstances. Utilizing these resources can provide borrowers with the support and information they need to effectively manage their MOHELA student loans and minimize interest payments.

Wrap-Up

Successfully navigating the world of student loan repayment requires a clear understanding of interest rates and available repayment options. By understanding the factors influencing MOHELA’s interest rates and employing effective management strategies, you can significantly reduce your overall interest burden and accelerate your path to debt freedom. Remember to utilize the resources provided and seek professional advice when needed to create a personalized repayment plan that aligns with your financial goals.

FAQ Guide

What factors besides loan type affect my MOHELA interest rate?

Your credit history, the repayment plan you choose, and the initial interest rate set at loan origination all play a role.

Can I refinance my MOHELA student loans to lower my interest rate?

Yes, refinancing is a possibility, but carefully weigh the pros and cons. Consider fees, new terms, and whether it truly benefits your financial situation.

How often does MOHELA update its interest rates?

Interest rates are typically fixed for the life of the loan, but check your loan documents for specifics. Changes might occur for specific repayment plans.

Where can I find a detailed breakdown of all MOHELA fees?

MOHELA’s official website should provide a comprehensive fee schedule, or you can contact their customer service for clarification.