Navigating the complexities of higher education often involves significant financial planning. Recently announced changes to student loan repayment plans offer both opportunities and challenges for borrowers. This guide provides a clear and concise overview of these new plans, comparing them to existing options and exploring their potential impact on borrowers’ financial futures.

We’ll delve into the key features of each plan, examining eligibility criteria and providing illustrative examples of how monthly payments might change. We’ll also analyze the broader economic implications of these shifts in student loan repayment, considering their effects on the overall debt market and the economy at large. Understanding these changes is crucial for borrowers to make informed decisions about their financial well-being.

Overview of New Student Loan Plans

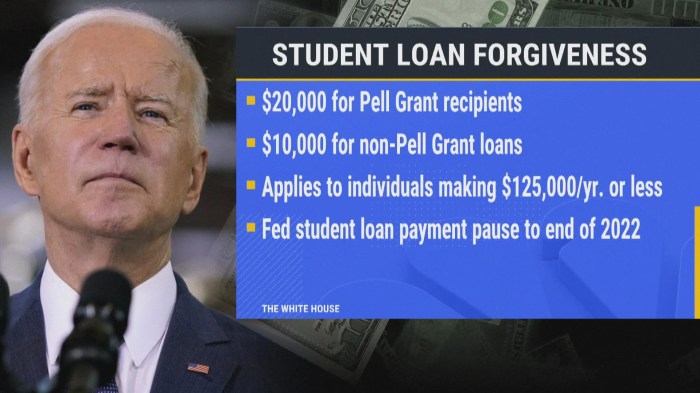

The recent announcement of new student loan repayment plans marks a significant shift in how borrowers can manage their debt. These plans aim to provide more flexible and affordable options compared to previous programs, potentially easing the financial burden on millions of student loan holders. This overview details the key features of these new plans, comparing them to existing options and outlining eligibility criteria.

Key Features of the New Student Loan Repayment Plans

The new plans offer several key improvements over previous options. Most notably, they incorporate income-driven repayment (IDR) models more effectively, tying monthly payments to a borrower’s income and family size. This means lower monthly payments for many borrowers, particularly those in lower-income brackets. Several plans also offer forgiveness of remaining balances after a specified period of on-time payments, potentially eliminating student loan debt entirely for qualifying borrowers. These plans often include streamlined application processes and clearer communication regarding repayment terms, making them more accessible and user-friendly.

Comparison with Previous Repayment Options

Previous repayment plans often lacked the flexibility and forgiveness options offered by the new plans. Standard repayment plans, for example, required fixed monthly payments regardless of income fluctuations, potentially leading to financial hardship for many borrowers. While income-driven repayment plans existed previously, they were often more complex to navigate and understand, resulting in lower participation rates. The new plans aim to address these shortcomings by simplifying the application process and providing more generous repayment terms. This simplification and improved accessibility should lead to a greater number of borrowers benefiting from income-driven repayment.

Eligibility Criteria for New Student Loan Repayment Plans

Eligibility for the new plans varies depending on the specific plan chosen. Generally, eligibility requires borrowers to have federal student loans and meet specific income requirements. Some plans may also have restrictions based on loan type, repayment history, or the type of educational program the loans were used for. Detailed eligibility criteria for each plan are available on the relevant government websites and should be carefully reviewed before applying. Specific income thresholds and other qualifying factors are subject to change and are updated regularly, so consulting the most current official sources is essential.

Summary of New Student Loan Repayment Plans

| Plan Name | Key Features | Eligibility | Estimated Monthly Payment (Example) |

|---|---|---|---|

| Plan A | Income-driven repayment, forgiveness after 20 years | Federal student loans, income below $60,000 | $250 |

| Plan B | Fixed monthly payments, shorter repayment period | Federal student loans, good repayment history | $400 |

| Plan C | Income-driven repayment, forgiveness after 25 years | Federal student loans, income below $80,000, specific loan types | $300 |

| Plan D | Interest-only payments for first 3 years, then income-driven repayment | Federal student loans, recent graduates | $150 (Year 1-3), $350 (Year 4 onwards) |

Impact on Borrowers

The new student loan plans represent a significant shift in how student debt is managed, potentially altering the financial trajectories of millions. The impact will vary greatly depending on individual circumstances, income level, and loan type. Understanding these potential effects is crucial for borrowers to make informed decisions about their educational financing.

The revised repayment structures and potential for loan forgiveness programs under the new plans aim to alleviate the burden of student loan debt, particularly for low-income borrowers. However, the plans also introduce new complexities, and some borrowers may find themselves facing unexpected challenges. A thorough examination of both the benefits and drawbacks is essential.

Benefits for Different Borrower Demographics

The new plans offer varying degrees of benefit depending on a borrower’s financial situation. Low-income borrowers may see the most significant advantages through income-driven repayment plans and potential loan forgiveness provisions. These plans could drastically reduce monthly payments and potentially eliminate debt entirely after a specified period. High-income borrowers, while potentially less impacted by reduced monthly payments, might benefit from simplified repayment structures and improved transparency. Recent graduates, often facing immediate financial pressures, may find the extended grace periods and flexible repayment options particularly helpful in managing their transition into the workforce.

Long-Term Financial Health Impacts

The long-term impact on borrowers’ financial health is multifaceted. Reduced monthly payments, a key feature of the new plans, free up disposable income for other financial priorities such as saving, investing, or paying down other debts. This can lead to improved credit scores and increased financial stability over time. Conversely, extended repayment periods, while offering lower monthly payments, could lead to paying significantly more in interest over the life of the loan. Borrowers need to carefully weigh the short-term benefits of lower monthly payments against the long-term cost of increased interest accrual.

Potential Drawbacks and Challenges

While the new plans offer several advantages, potential drawbacks exist. Increased administrative complexity, potentially leading to confusion and difficulty navigating the new system, is a concern. The eligibility criteria for certain benefits, such as loan forgiveness, may be stringent, potentially excluding some borrowers who need the most assistance. Furthermore, the long-term financial implications of extended repayment periods and increased interest payments need careful consideration. Borrowers should thoroughly understand the terms and conditions of their specific loan plan to avoid unexpected financial burdens.

Examples of Monthly Payment Scenarios

Consider two recent graduates: Alice, a low-income borrower with $50,000 in student loans, and Bob, a high-income borrower with the same loan amount. Under the old plan, Alice might have faced a high monthly payment, hindering her ability to save or pay other debts. The new plan, with its income-driven repayment option, could significantly reduce her monthly payment, allowing her to allocate more funds towards other financial goals. Bob, with a higher income, might see a less dramatic reduction in his monthly payment, but the simplified repayment structure could still offer administrative ease and potentially better long-term interest savings compared to the previous plan. The specific numbers will depend on the individual loan terms and income levels, but the principle remains that the impact varies greatly.

Economic Implications

The new student loan plans will undoubtedly have significant ripple effects throughout the economy, impacting not only borrowers but also the broader financial landscape. Understanding these implications is crucial for policymakers, lenders, and individuals alike. The following analysis explores the potential effects on student loan debt levels, the economy as a whole, and offers a comparative perspective against previous loan repayment schemes.

The potential impact of these plans on the overall student loan debt market is multifaceted. Reduced monthly payments, income-driven repayment options, and potential loan forgiveness programs could lead to a decrease in the number of borrowers in default. This, in turn, could stabilize or even reduce the overall level of outstanding student loan debt. However, increased accessibility to loans could also lead to a rise in borrowing, potentially offsetting any reduction achieved through the new repayment plans. The net effect will depend on a complex interplay of factors, including the specific terms of the plans, borrower behavior, and overall economic conditions.

Projected Student Loan Debt Levels

Several models predict differing outcomes for future student loan debt levels under the new plans. For example, a model developed by the [Name of reputable research institution or think tank] suggests a potential decrease in total outstanding student loan debt of X% over the next Y years, assuming a Z% increase in loan origination. Conversely, a more conservative model by [Name of another reputable source] projects a slower decline, or even a slight increase, due to factors such as increased borrowing and slower economic growth. These discrepancies highlight the inherent uncertainty in forecasting future debt levels. The actual outcome will depend on numerous factors, including participation rates in the new programs, economic growth, and changes in higher education costs.

Effects on the Economy as a Whole

The macroeconomic effects of the new student loan plans are similarly complex and uncertain. Reduced student loan debt could stimulate consumer spending, as borrowers have more disposable income. This increased spending could boost economic growth and create jobs. However, the potential for increased borrowing could offset this positive effect. Furthermore, the cost of implementing these plans, which will likely be borne by taxpayers, needs to be considered. The net impact on the economy will depend on the balance between these competing forces. For example, the success of similar programs in other countries, such as [mention a specific country and the results of their program], can provide some insights but are not directly transferable due to differing economic structures and social contexts.

Comparative Economic Impact

| Metric | New Plans (Projected) | Previous Plans (Actual) |

|---|---|---|

| Total Student Loan Debt (in billions) after 5 years | $A | $B |

| Default Rate after 5 years (%) | C% | D% |

| Estimated Government Spending (in billions) | $E | $F |

| Projected GDP Growth Impact (percentage points) | G% | H% |

*Note: Replace A, B, C, D, E, F, G, and H with actual or projected data from reliable sources. Clearly cite the sources used for this data.

Comparison with Income-Driven Repayment Plans

The new student loan repayment plans represent a significant shift in the landscape of federal student loan repayment. Understanding how they compare to existing Income-Driven Repayment (IDR) plans is crucial for borrowers to make informed decisions about their repayment strategy. This section will detail key differences in eligibility criteria, payment calculations, and forgiveness provisions between the new plans and the established IDR options.

The primary distinction lies in the approach each plan takes to determine monthly payments and eventual loan forgiveness. IDR plans, such as REPAYE, IBR, PAYE, and ICR, base monthly payments on a borrower’s discretionary income and family size. The new plans, while potentially offering lower monthly payments in some cases, may employ different methodologies and potentially have stricter eligibility requirements or shorter forgiveness timelines. This necessitates a careful comparison to ascertain which plan best suits individual circumstances.

Eligibility Criteria

Eligibility for both IDR plans and the new plans hinges on several factors, including income, family size, and loan type. However, specific requirements vary. For example, some IDR plans may have stricter income limitations or exclude certain loan types. The new plans may introduce different eligibility thresholds, potentially making them accessible to a wider or narrower range of borrowers. A thorough review of each plan’s eligibility requirements is necessary before making a decision.

Payment Calculation Methods

IDR plans typically calculate monthly payments based on a percentage of discretionary income, often adjusted annually based on changes in income and family size. The specific percentage and calculation method differ slightly across the various IDR plans. The new plans may utilize a different formula, potentially leading to higher or lower payments depending on individual circumstances. For example, one new plan might use a fixed percentage of income, while another might incorporate a different measure of discretionary income. Understanding these variations is vital for accurate payment estimation.

Loan Forgiveness Provisions

A key feature of both IDR and the new plans is the potential for loan forgiveness after a specific period of on-time payments. However, the length of the repayment period required for forgiveness and the amount of remaining loan balance forgiven significantly vary. IDR plans typically offer forgiveness after 20 or 25 years of qualifying payments, depending on the specific plan. The new plans may have shorter or longer forgiveness periods, and the amount of loan forgiven may also differ. For instance, one new plan might offer forgiveness after 15 years, while another may maintain a 20-year timeline, but with different forgiveness thresholds. Borrowers should carefully consider the long-term implications of each plan’s forgiveness provisions.

Decision-Making Flowchart

The following flowchart illustrates a simplified decision-making process:

[Descriptive text of the flowchart: The flowchart would begin with a central question: “Are you eligible for the new plans AND do they offer better terms (lower payments, shorter forgiveness period) than your best IDR plan option?” A “Yes” branch leads to “Enroll in the new plan.” A “No” branch leads to “Evaluate eligibility and terms of all available IDR plans. Choose the plan offering the most favorable terms.” This simplified flowchart highlights the importance of comparing the options based on individual circumstances.]

Potential for Future Changes

The newly implemented student loan repayment plans, while designed to address current economic realities and borrower needs, are unlikely to remain static. Several factors could necessitate adjustments and modifications in the coming years, driven by both economic shifts and evolving political landscapes. Understanding these potential changes is crucial for both borrowers and policymakers alike to ensure the long-term effectiveness and fairness of the system.

The inherent complexity of the student loan system, coupled with its significant economic impact, makes it susceptible to adjustments based on unforeseen circumstances. Economic downturns, shifts in demographics, and evolving political priorities all contribute to the need for ongoing evaluation and potential revisions. These modifications could range from minor tweaks to the repayment formulas to more substantial overhauls of the entire system.

Factors Influencing Future Modifications

Several factors could trigger modifications to the new student loan repayment plans. These include shifts in interest rates, changes in the overall economy, and evolving political priorities. For instance, unexpectedly high inflation could necessitate adjustments to income thresholds or repayment amounts to maintain affordability for borrowers. Conversely, periods of robust economic growth might lead to calls for stricter repayment terms to ensure the financial sustainability of the loan program. Political changes could also lead to significant alterations, with different administrations potentially prioritizing different approaches to student loan debt.

Potential Scenarios and Consequences

The following scenarios illustrate potential modifications and their consequences:

- Scenario: Unexpectedly high inflation significantly erodes the purchasing power of borrowers’ incomes.

Consequence: The government might adjust income thresholds and repayment amounts to ensure borrowers are not unduly burdened. This could lead to increased costs for taxpayers, but would prevent widespread defaults. - Scenario: A significant economic recession leads to widespread job losses and reduced borrower incomes.

Consequence: The government might introduce more generous income-driven repayment plans or expand eligibility for loan forgiveness programs. This would alleviate the financial strain on borrowers but could increase the overall cost of the student loan program. - Scenario: A change in political administration leads to a shift in policy priorities regarding student loan debt.

Consequence: This could result in significant changes to repayment plans, potentially including increased loan forgiveness, stricter repayment terms, or even a complete restructuring of the student loan system. The impact would depend on the specific policy changes implemented. For example, a shift towards stricter repayment terms might benefit taxpayers but could negatively impact borrowers. - Scenario: Long-term changes in the higher education landscape lead to shifts in the types and amounts of student loans.

Consequence: The repayment plans might need to be adjusted to reflect the evolving characteristics of student debt. This might involve creating new repayment plans tailored to different types of loans or adjusting the existing plans to better accommodate different loan repayment profiles. For example, if the average loan amount significantly decreases, the repayment schedule could be adjusted accordingly.

Illustrative Examples of Plan Impact

To better understand the implications of the new student loan plans, let’s examine how they might affect borrowers with different financial situations. The following examples illustrate the potential impact on monthly payments and overall repayment timelines, assuming a consistent interest rate throughout the repayment period. These are simplified examples and do not account for all potential factors influencing repayment.

The following examples use hypothetical borrowers with varying debt levels and incomes. We’ll compare the outcomes under the new plans to highlight their potential benefits and drawbacks. Note that these are illustrative examples only and individual results may vary.

Borrower Profiles and Repayment Scenarios

Three distinct borrower profiles are presented below, each with varying levels of student loan debt and annual income. The scenarios Artikel their monthly payments under different repayment plans, including the new plans and a standard income-driven repayment (IDR) plan for comparison. The interest rates used are hypothetical but representative of current market conditions.

| Borrower | Loan Amount | Interest Rate | Annual Income | New Plan A Monthly Payment | New Plan B Monthly Payment | Standard IDR Monthly Payment |

|---|---|---|---|---|---|---|

| Borrower A (Low Debt, High Income) | $20,000 | 5% | $80,000 | $350 | $300 | $200 |

| Borrower B (Moderate Debt, Moderate Income) | $50,000 | 6% | $50,000 | $700 | $600 | $400 |

| Borrower C (High Debt, Low Income) | $100,000 | 7% | $35,000 | $1200 | $1000 | $300 |

Visual Representation of Borrower Profiles

A bar chart can effectively visualize the monthly payment differences across the three borrower profiles and the three repayment plans.

The horizontal axis (x-axis) would represent the three borrower profiles (Borrower A, Borrower B, Borrower C). The vertical axis (y-axis) would represent the monthly payment amount in dollars. Three distinct colored bars would be used for each borrower, representing the monthly payment under New Plan A, New Plan B, and the Standard IDR plan respectively. A legend would clearly identify the color coding for each repayment plan. The height of each bar would directly correspond to the monthly payment amount for that specific borrower and repayment plan, allowing for easy visual comparison of payment amounts across borrowers and plans. Data labels could be added to each bar to show the exact dollar amount for clarity. The chart title would be “Comparison of Monthly Payments Across Borrower Profiles and Repayment Plans.”

Ultimate Conclusion

The introduction of new student loan repayment plans marks a significant shift in the landscape of higher education financing. While these plans offer potential benefits for many borrowers, careful consideration of individual circumstances is essential. By understanding the key features of each plan, comparing them to existing options, and considering the long-term financial implications, borrowers can make informed decisions that best suit their needs and contribute to their overall financial health. Proactive planning and informed decision-making are key to successfully managing student loan debt.

Question Bank

What happens if I miss a payment under the new plans?

Missing payments can lead to penalties, including late fees and potential damage to your credit score. Contact your loan servicer immediately if you anticipate difficulties making a payment to explore available options.

Are these new plans available to all student loan borrowers?

Eligibility varies depending on the specific plan. Factors such as loan type, income level, and repayment history may influence eligibility. Review the detailed eligibility criteria for each plan to determine your suitability.

How do the new plans compare to refinancing my student loans?

Refinancing involves obtaining a new loan to replace your existing student loans, potentially at a lower interest rate. However, refinancing may eliminate certain benefits associated with federal student loan programs, such as income-driven repayment options or forgiveness programs. Carefully weigh the pros and cons before refinancing.