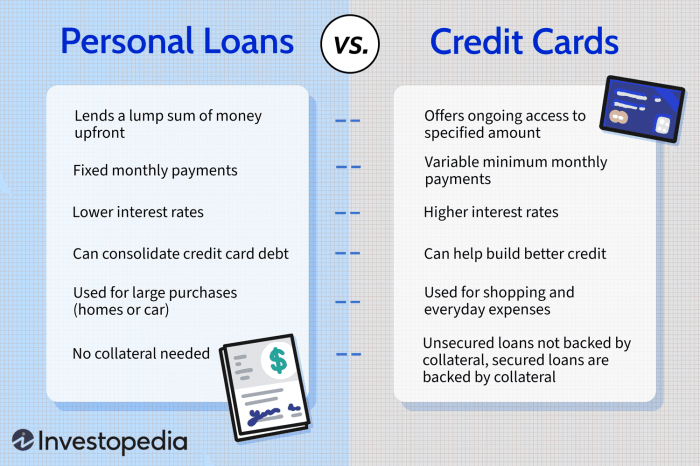

Navigating the world of loans can be daunting, especially when faced with the choice between a personal loan and a student loan. Both offer financial assistance, but their terms, eligibility criteria, and long-term implications differ significantly. Understanding these differences is crucial for making informed financial decisions that align with your individual needs and goals. This guide will delve into the key aspects of each loan type, empowering you to choose wisely.

We’ll explore interest rates, repayment options, eligibility requirements, credit score impacts, and the various fees associated with each loan. Furthermore, we’ll examine the specific uses of each loan type, discuss the potential for student loan debt consolidation using personal loans, and highlight the relevant government regulations and consumer protections. Ultimately, our aim is to provide a clear and comprehensive comparison, enabling you to make the best choice for your financial future.

Interest Rates and Repayment Terms

Understanding the interest rates and repayment terms is crucial when choosing between a personal loan and a student loan. Both loan types have distinct characteristics that significantly impact the borrower’s financial obligations. This section will compare and contrast these key aspects to help you make an informed decision.

Interest Rates for Personal and Student Loans

Personal loan interest rates are generally higher than those for federal student loans. This is because personal loans are unsecured, meaning they don’t require collateral, unlike some student loans which may be secured by assets. The interest rate on a personal loan is determined by several factors, including your credit score, income, debt-to-income ratio, and the loan amount. A higher credit score typically results in a lower interest rate. In contrast, federal student loan interest rates are often subsidized (meaning the government pays the interest while you’re in school under certain circumstances) or unsubsidized, with rates set annually by the government and generally lower than personal loan rates. Private student loans, however, can have interest rates comparable to or even higher than personal loans, depending on the borrower’s creditworthiness.

Repayment Schedules and Grace Periods

Personal loan repayment schedules typically begin immediately after the loan is disbursed. Repayment terms vary, ranging from a few months to several years, with monthly payments calculated based on the loan amount, interest rate, and repayment term. Late payments can result in penalties, such as increased interest charges or late fees. The specific terms are Artikeld in the loan agreement. Student loans, particularly federal student loans, often include a grace period, usually six months after graduation or leaving school, before repayment begins. This allows borrowers time to secure employment and adjust to their post-education financial situation. However, interest may still accrue during the grace period on unsubsidized loans. Late payments on student loans can also lead to penalties, potentially affecting your credit score and future borrowing opportunities.

Repayment Plan Options

Both personal and student loans offer various repayment plan options, tailored to individual circumstances. The choice of repayment plan significantly influences the monthly payment amount and the total interest paid over the loan’s life.

| Loan Type | Repayment Plan | Interest Rate Example | Monthly Payment Example (for a $10,000 loan) |

|---|---|---|---|

| Personal Loan | Standard | 7-18% | $200 – $350 (depending on interest rate and loan term) |

| Personal Loan | Short-Term | 8-20% | $300 – $500 (higher monthly payment due to shorter term) |

| Federal Student Loan | Standard 10-year | 4-7% (variable depending on loan type and year) | $100 – $150 (depending on interest rate) |

| Federal Student Loan | Income-Driven Repayment (IDR) | 4-7% (variable depending on loan type and year) | Variable, based on income and family size |

| Private Student Loan | Standard | 6-15% | $150 – $300 (depending on interest rate and loan term) |

| Private Student Loan | Graduated | 7-18% | Starts low, increases over time |

Credit Score Impact

Your credit score is a crucial number that lenders use to assess your creditworthiness. Both personal and student loans significantly impact this score, but in different ways. Understanding these impacts is vital for making informed borrowing decisions and maintaining a healthy credit profile. Responsible loan management can boost your score, while mismanagement can severely damage it.

Impact of Personal and Student Loans on Credit Scores

Obtaining a personal or student loan can positively or negatively affect your credit score, depending on your borrowing and repayment behavior. A personal loan is typically viewed by lenders as a reflection of your ability to manage debt responsibly in various situations, while a student loan, specifically federal student loans, may be viewed slightly differently due to the unique nature of the loan and the common understanding of financial limitations during education. However, both loan types are reported to credit bureaus and thus affect your credit score.

- Positive Impacts: Responsible management of both loan types, including consistent on-time payments, can demonstrate creditworthiness and lead to a higher credit score. Establishing a positive payment history is a significant factor in credit scoring models. Furthermore, successfully managing multiple loans, showing you can handle different repayment schedules and amounts, can positively impact your credit score.

- Negative Impacts: Missing payments, even one, can negatively affect your credit score. Late payments on both personal and student loans will significantly lower your credit score, remaining on your credit report for seven years. Defaulting on either loan type is exceptionally detrimental, leading to a drastic drop in your score and potentially impacting your ability to secure future loans or credit. This can also lead to wage garnishment or collection agency involvement. Taking on too much debt relative to your income (high debt-to-income ratio) can also negatively impact your score regardless of payment history.

Long-Term Effects of Defaults or Late Payments

The consequences of defaulting or making late payments on personal and student loans extend far beyond a simple credit score reduction. These actions can have long-term financial ramifications that significantly impact your future opportunities. For instance, a default on a student loan can lead to wage garnishment, making it difficult to manage expenses. A severely damaged credit score can make it challenging to rent an apartment, obtain a car loan, or even secure a job in certain fields. The negative impact can last for years, making it harder to rebuild your credit.

- Personal Loan Default: A personal loan default will severely damage your credit score, making it difficult to obtain credit in the future. It can also lead to legal action from the lender. The impact on your credit report will last for seven years, hindering your ability to access favorable interest rates on future loans.

- Student Loan Default: Student loan default can have even more severe consequences, including wage garnishment, tax refund offset, and potential difficulty obtaining government benefits. It can also make it extremely difficult to secure future loans, mortgages, or even certain jobs. The negative impact on your credit report will persist for seven years, affecting your financial prospects for an extended period.

Loan Purposes and Usage Restrictions

Personal and student loans, while both offering access to borrowed funds, cater to distinct needs and come with specific limitations on how the money can be used. Understanding these differences is crucial for making informed borrowing decisions. This section will clarify the typical uses and restrictions associated with each loan type.

Personal loans offer considerable flexibility in how the borrowed funds can be used, but this flexibility isn’t unlimited. Lenders generally don’t inquire about the specific purpose of the loan, allowing borrowers to use the money for various expenses, including debt consolidation, home improvements, medical bills, or even major purchases like a car. However, lenders often prohibit using the funds for illegal activities or investments deemed too high-risk. Some lenders may also have restrictions on specific uses, such as purchasing certain types of assets. For example, a lender may not approve a personal loan for speculative investments in cryptocurrency.

Personal Loan Usage Restrictions

While personal loans offer flexibility, several restrictions commonly apply. These limitations aim to protect both the lender and the borrower from potential misuse of funds. For example, using a personal loan for illegal activities is strictly prohibited. Furthermore, lenders often scrutinize the creditworthiness of the borrower before approving a loan, and borrowers with poor credit histories may face higher interest rates or loan denials. Additionally, some lenders might impose restrictions on the use of funds for specific purposes, such as purchasing highly speculative assets or financing business ventures. This is because these ventures carry inherent risks that could jeopardize the repayment of the loan.

Student Loan Usage Restrictions

Student loans, unlike personal loans, are specifically designed to finance education-related expenses. This focused purpose means that the funds are typically restricted to paying for tuition, fees, room and board, books, and other education-related supplies. Borrowers cannot generally use student loan funds for non-educational purposes, such as purchasing a car or paying off credit card debt. The specific allowable expenses may vary slightly depending on the type of student loan and the lender. Federal student loans, for instance, typically have stricter guidelines than private student loans. It’s important to consult with the lender to understand the precise terms and conditions of any student loan.

Examples of Appropriate Loan Choices

Imagine someone needs to consolidate high-interest credit card debt. A personal loan, with its flexibility and potential for lower interest rates than credit cards, would be the more suitable option. Conversely, a student pursuing a master’s degree would find a student loan more appropriate, as it directly covers tuition and other educational expenses, and often offers more favorable repayment terms for educational purposes. If an individual needs to finance home renovations, a personal loan is typically a better fit than a student loan, given the latter’s specific focus on educational expenses. A personal loan can also be a good choice for unexpected medical expenses or the purchase of a reliable used vehicle for commuting to work.

Fees and Charges

Understanding the fees associated with both personal and student loans is crucial for making informed borrowing decisions. These charges can significantly impact the overall cost of the loan, so careful comparison is essential before committing to either option. While both loan types involve fees, the types and amounts differ considerably.

Both personal and student loans can include various fees, affecting the total repayment amount. Origination fees, late payment penalties, and prepayment penalties are common examples. However, the specifics and prevalence of these fees vary between loan types and lenders. It’s vital to review the loan agreement thoroughly before signing to understand all associated costs.

Comparison of Fees for Personal and Student Loans

The following table provides a side-by-side comparison of common fees for personal and student loans. Remember that these are examples, and the specific fees and amounts can vary widely depending on the lender and the terms of the loan agreement. Always confirm the exact fees with your lender before borrowing.

| Fee Type | Personal Loan | Student Loan (Federal) | Student Loan (Private) |

|---|---|---|---|

| Origination Fee | May range from 1% to 5% of the loan amount, or may be absent. | Generally none for federal student loans. | May range from 0% to 8% of the loan amount, or may be absent. Varies greatly by lender. |

| Late Payment Fee | Typically a fixed dollar amount or a percentage of the missed payment, often $25-$50 or more. | Can vary; for federal loans, typically a percentage of the missed payment amount. | Varies greatly by lender; often a fixed dollar amount or percentage of the missed payment. |

| Prepayment Penalty | Becoming less common, but some lenders may charge a penalty for paying off the loan early. This is usually a percentage of the remaining loan balance. | Generally none for federal student loans. | May or may not be present, depending on the lender and loan terms. If present, usually a percentage of the prepayment. |

| Other Fees | Potential for additional fees such as application fees, returned check fees, or wire transfer fees. | May include fees for loan consolidation or deferment/forbearance. | May include similar fees as personal loans, plus additional fees related to loan origination or servicing. |

Debt Consolidation

Consolidating debt, particularly student loan debt, is a strategy some individuals employ to simplify their financial management. A personal loan can be used to pay off multiple student loans, resulting in a single monthly payment. This can make budgeting easier and potentially reduce overall stress related to managing multiple loans. However, it’s crucial to carefully weigh the potential benefits against the drawbacks before pursuing this approach.

Debt consolidation using a personal loan can offer several advantages, but it’s not always the optimal solution. The decision depends heavily on individual circumstances and the terms of the available personal loan.

Advantages of Consolidating Student Loan Debt with a Personal Loan

A key advantage is the simplification of repayment. Managing multiple student loans with varying interest rates and due dates can be complex. Consolidating them into a single personal loan streamlines this process, making it easier to track payments and avoid missed deadlines. Another potential benefit is a lower monthly payment, though this depends entirely on the interest rate of the personal loan and the repayment term selected. A longer repayment term will lower monthly payments, but it will ultimately cost more in interest over the life of the loan. Finally, a fixed interest rate on a personal loan offers predictability, unlike some student loan programs that may have variable interest rates.

Disadvantages of Consolidating Student Loan Debt with a Personal Loan

One major disadvantage is the potential for a higher overall interest rate. If the personal loan carries a higher interest rate than the average rate of your existing student loans, consolidating could ultimately cost you more in the long run. Furthermore, consolidating student loans might mean losing access to certain benefits associated with federal student loans, such as income-driven repayment plans or loan forgiveness programs. Lastly, consolidating through a personal loan typically requires a good credit score to secure favorable terms, making it inaccessible to borrowers with poor credit history.

Hypothetical Scenario: Beneficial Consolidation

Imagine a borrower with three federal student loans totaling $50,000, each with varying interest rates ranging from 5% to 7%. They struggle to manage the three separate payments. They qualify for a personal loan with a fixed 6% interest rate and a manageable monthly payment. In this case, consolidation simplifies repayment, provides a predictable interest rate, and offers a potentially more manageable monthly payment.

Hypothetical Scenario: Detrimental Consolidation

Consider a borrower with federal student loans totaling $30,000 at a low fixed interest rate of 3%. They are offered a personal loan with a 9% interest rate. While a single monthly payment might seem appealing, the significantly higher interest rate on the personal loan would result in paying substantially more over the life of the loan, outweighing the convenience of a single payment. Furthermore, they might lose access to federal loan forgiveness programs. In this situation, consolidation would be financially detrimental.

Government Regulations and Protections

Both personal loans and student loans fall under the purview of various government regulations designed to protect consumers. However, the specific regulations and the level of protection offered differ significantly between the two loan types. This stems from the fundamentally different nature of the loans and the perceived vulnerability of student borrowers.

Student loans, particularly federal student loans, benefit from a robust framework of consumer protections absent in the largely unregulated personal loan market. These protections aim to prevent predatory lending practices and ensure borrowers understand the terms and conditions before committing to a loan. Conversely, personal loans are subject to fewer federal regulations, leaving borrowers more vulnerable to potentially unfavorable terms and higher interest rates.

Federal Student Loan Protections

Federal student loans in the United States are subject to extensive regulations under the Higher Education Act of 1965 and subsequent amendments. These regulations establish various borrower protections, including limits on interest rates, deferment and forbearance options in times of financial hardship, and income-driven repayment plans that tie monthly payments to income levels. Furthermore, there are strong protections against abusive collection practices. Borrowers are also afforded the right to appeal loan decisions and to seek assistance from federal agencies like the Department of Education. For example, the government offers loan forgiveness programs for specific professions, like teaching or public service, further illustrating the level of protection offered.

Personal Loan Regulations

Personal loans are largely governed by state laws, with federal regulations primarily focused on aspects like fair lending practices (prohibiting discrimination based on race, religion, etc.) and truth-in-lending disclosures. These disclosures require lenders to clearly state the loan’s terms, including the Annual Percentage Rate (APR), fees, and repayment schedule. However, the level of protection is significantly less than that afforded to student loan borrowers. There is less oversight of interest rates, and fewer options for repayment flexibility during periods of financial difficulty. While state laws vary, many lack the comprehensive borrower protections found in the federal student loan system. For instance, there are no widely available income-driven repayment plans for personal loans, making them potentially more difficult to manage during economic downturns.

Key Differences in Borrower Protections

The following points highlight the key differences in borrower protections between personal and student loans:

- Interest Rate Caps: Federal student loans often have interest rate caps or limitations, whereas personal loan interest rates are largely market-driven and can be significantly higher.

- Repayment Flexibility: Federal student loans offer various repayment options, including income-driven repayment plans, deferment, and forbearance. Personal loans typically have less flexible repayment options.

- Loan Forgiveness Programs: Federal student loans may qualify for loan forgiveness programs based on specific employment or public service, a benefit rarely available for personal loans.

- Government Oversight: Federal student loans are subject to strict government oversight and regulations, while personal loans are primarily regulated at the state level, with less stringent oversight.

- Collection Practices: Stricter regulations govern the collection practices for federal student loans, offering greater protection against abusive debt collection tactics than is typically seen with personal loans.

Long-Term Financial Implications

Understanding the long-term financial consequences of both personal and student loans is crucial for responsible borrowing. While both can provide necessary funds, their impact on your future financial health differs significantly due to factors like interest rates, repayment periods, and the potential for impacting future borrowing. Failing to adequately consider these implications can lead to substantial financial strain later in life.

The long-term effects of personal and student loans diverge primarily in their impact on credit scores and future borrowing capacity. Student loans, while potentially carrying lower interest rates, often have longer repayment periods, extending their financial burden. Personal loans, conversely, may have higher interest rates but shorter repayment terms, potentially leading to faster debt elimination but potentially harming credit scores if not managed correctly. Both loan types, however, can significantly influence one’s overall financial well-being if not handled responsibly.

Impact on Future Borrowing Capacity

The presence of both personal and student loan debt can affect your ability to secure future loans, such as mortgages or auto loans. Lenders assess your debt-to-income ratio (DTI) – the proportion of your income allocated to debt repayment – when evaluating your creditworthiness. A high DTI, resulting from significant loan balances, can negatively impact your chances of loan approval or lead to less favorable loan terms (higher interest rates). For example, someone with substantial student loan debt and a high DTI might struggle to qualify for a mortgage, delaying homeownership plans. Similarly, someone with multiple personal loans and high balances might find it difficult to obtain a car loan at a competitive interest rate. Careful management of existing loans, including timely payments, is crucial for maintaining a healthy DTI and improving future borrowing prospects.

Potential Long-Term Consequences of Mismanagement

Mismanagement of either loan type can have severe long-term consequences. With personal loans, high interest rates and late payments can lead to a snowball effect of accumulating debt and negatively impacting your credit score. This could result in difficulty securing credit in the future, higher interest rates on subsequent loans, and even potential legal action from creditors. For instance, if someone consistently misses payments on a personal loan, they might face penalties, fees, and ultimately, default, resulting in a severely damaged credit report and potentially impacting their ability to rent an apartment or even secure employment.

For student loans, defaulting on payments can have equally serious repercussions. The government may garnish wages, seize tax refunds, and even impact future employment opportunities. Furthermore, a default will significantly damage your credit score, making it challenging to obtain credit for major purchases or even everyday needs in the future. For example, a graduate who defaults on their federal student loans might face significant financial hardship, with a damaged credit score preventing them from buying a home, securing a car loan, or even getting a credit card. This could severely limit their financial options for years to come.

Last Word

Choosing between a personal loan and a student loan requires careful consideration of your individual circumstances and financial goals. While both options provide access to funds, their implications on your credit score, repayment terms, and long-term financial well-being vary considerably. By understanding the nuances of each loan type – from interest rates and eligibility requirements to fees and government regulations – you can make a well-informed decision that aligns with your financial objectives and sets you on a path toward responsible borrowing and financial success.

Questions Often Asked

What happens if I default on a student loan?

Defaulting on a student loan can have severe consequences, including damage to your credit score, wage garnishment, and tax refund offset.

Can I use a personal loan to pay off credit card debt?

Yes, personal loans can be used to consolidate high-interest credit card debt, potentially lowering your monthly payments and interest rate.

Are there tax benefits associated with student loans?

Depending on your country and specific circumstances, there might be tax deductions or credits available for student loan interest payments.

What is the average interest rate for a personal loan?

The average interest rate for a personal loan varies depending on your credit score, loan amount, and lender. It’s generally higher than federal student loan interest rates.