Navigating the complexities of past-due private student loans can feel overwhelming. Millions of borrowers face this challenge annually, grappling with the consequences of missed payments and the uncertainty of their financial future. This guide offers a comprehensive overview of understanding, addressing, and preventing delinquency, providing practical strategies and resources to regain control of your student loan debt.

From exploring various repayment options and negotiating with lenders to understanding the legal implications and preventing future delinquency, we aim to equip you with the knowledge and tools necessary to navigate this difficult situation effectively. We’ll cover everything from budgeting techniques and financial planning to debt consolidation and refinancing strategies, ensuring you have a clear path forward.

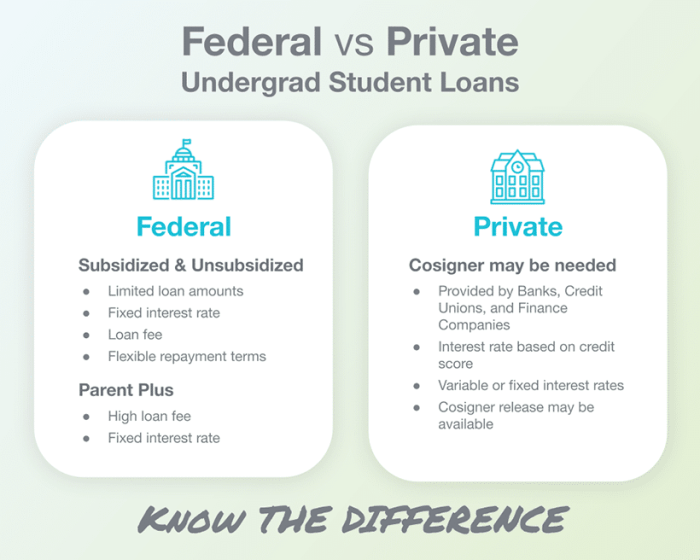

Understanding Past Due Private Student Loans

Falling behind on private student loan payments can have significant consequences. Understanding the reasons for delinquency, the potential repercussions, and the stages involved is crucial for borrowers facing this challenge. This information aims to provide clarity and help navigate this difficult situation.

Reasons for Private Student Loan Delinquency

Several factors can contribute to private student loan delinquency. These often intertwine, creating complex financial situations. Job loss, unexpected medical expenses, or a decrease in income are common triggers. Difficulty managing multiple debts, coupled with insufficient budgeting skills, can also lead to missed payments. Sometimes, unforeseen circumstances such as divorce or family emergencies create financial strain, resulting in loan delinquency. Furthermore, a lack of understanding of loan terms and repayment options can contribute to borrowers falling behind.

Consequences of Past-Due Private Student Loans

The consequences of past-due private student loans can be severe and far-reaching. Late payment fees are immediately incurred, increasing the overall debt burden. A negative impact on credit scores is almost certain, making it harder to secure loans, rent an apartment, or even get a job in some fields. Lenders may initiate collection efforts, which can include phone calls, letters, and even legal action. In extreme cases, wage garnishment or bank account levies may occur. Furthermore, the inability to obtain future loans can severely limit financial opportunities.

Stages of Private Student Loan Delinquency

Private student loan delinquency typically progresses through several stages. The first stage is usually characterized by a missed payment, resulting in a late payment fee. The second stage involves further missed payments, escalating the delinquency status and triggering more serious collection actions. The third stage often involves the loan being referred to collections agencies, leading to aggressive collection efforts and potential legal action. Finally, the lender might initiate legal proceedings, potentially resulting in a judgment against the borrower, impacting credit and potentially leading to wage garnishment or property seizure. The specific timelines and actions taken vary among lenders.

Communication Strategies Used by Lenders

Lenders employ various communication strategies to engage with borrowers facing delinquency. Initial contact often involves friendly reminders via email or mail, outlining the missed payment and the associated fees. As delinquency progresses, lenders may intensify their communication, using phone calls and certified letters to emphasize the seriousness of the situation. They may also offer repayment plans, such as forbearance or deferment, to help borrowers get back on track. In more severe cases, lenders might engage collection agencies or initiate legal proceedings. The specific communication approach is dependent on the severity of the delinquency and the borrower’s responsiveness.

Negotiating with Lenders

Negotiating with your private student loan lender regarding a past-due balance can be a stressful but potentially rewarding process. Success depends on a proactive and well-prepared approach, focusing on clear communication and a demonstrable commitment to repayment. Remember, your goal is to reach an agreement that’s manageable for you while also satisfying the lender’s need to recover their investment.

Effective strategies involve understanding your lender’s perspective and presenting a realistic plan for repayment. This requires careful preparation and a willingness to compromise. While there’s no guarantee of success, a strategic approach significantly improves your chances of reaching a favorable resolution.

Effective Negotiation Strategies

Several strategies can significantly improve your chances of a successful negotiation. These include demonstrating a genuine desire to repay the loan, offering a concrete repayment plan, and showcasing financial hardship if applicable. Gathering supporting documentation strengthens your position and builds credibility with the lender. It’s also crucial to maintain a respectful and professional tone throughout the process.

Examples of Successful Negotiation Tactics

One successful tactic involves proposing a repayment plan that aligns with your current financial capabilities. For example, if you’re facing unemployment, offering a temporary reduced payment amount or deferment may be more palatable to the lender than ignoring the debt. Another effective strategy is to consolidate multiple loans into a single payment, simplifying repayment and potentially securing a lower interest rate. A borrower facing a significant medical expense might successfully negotiate a forbearance period, temporarily suspending payments until their financial situation improves.

Sample Negotiation Letter

[Date]

[Lender Name]

[Lender Address]

Dear [Loan Officer Name],

I am writing to request a modification of my private student loan account, [Loan Account Number]. Due to [briefly explain reason for delinquency, e.g., unexpected job loss, medical expenses], I have fallen behind on my payments.

I understand the seriousness of my delinquency and am committed to resolving this matter. I propose [clearly Artikel your proposed repayment plan, including payment amount and frequency]. I have attached documentation supporting my current financial situation [mention supporting documents, e.g., pay stubs, bank statements, medical bills].

I am confident that this revised repayment plan is achievable and will allow me to repay my loan in full. I am available to discuss this proposal further at your convenience. Thank you for your time and consideration.

Sincerely,

[Your Name]

[Your Phone Number]

[Your Email Address]

Preparing for the Negotiation Process

Thorough preparation is paramount to a successful negotiation. Begin by gathering all relevant documentation, including your loan agreement, recent pay stubs, bank statements, and any other evidence supporting your financial situation. Create a realistic budget to identify your current financial capacity and determine a feasible repayment plan. Research your lender’s past practices and policies regarding loan modifications to anticipate their potential responses. Finally, practice clearly and concisely articulating your situation and proposed repayment plan. This preparation will instill confidence and allow you to effectively present your case.

Legal and Financial Implications

Failing to repay private student loans carries significant legal and financial repercussions that can impact various aspects of your life, extending far beyond the immediate debt. Understanding these implications is crucial for proactive management of your student loan debt.

Legal Consequences of Defaulting on Private Student Loans

Defaulting on a private student loan initiates a series of legal actions designed to recover the outstanding debt. These actions can vary depending on the lender and the jurisdiction, but generally include wage garnishment, bank levy (seizing funds from your bank account), and the potential for lawsuits leading to judgments against you. A judgment can result in further actions such as property liens, impacting your ability to sell or refinance your home. Furthermore, your credit score will suffer significantly, affecting your ability to secure loans, rent an apartment, or even obtain certain jobs. In some cases, lenders may pursue legal action to seize assets to satisfy the debt. The severity of these consequences emphasizes the importance of proactive communication with your lender if you anticipate difficulty in repayment.

The Role of Debt Collection Agencies

If you fall behind on your private student loan payments, your lender may eventually sell your debt to a debt collection agency. These agencies are hired to recover outstanding debts on behalf of lenders. Debt collection agencies are known for their aggressive tactics, which may include repeated phone calls, letters, and even potential legal action. While they operate within legal boundaries, their primary goal is debt recovery, and their methods can be stressful. It’s crucial to understand your rights when dealing with debt collection agencies and to document all communication. The Fair Debt Collection Practices Act (FDCPA) protects consumers from abusive, deceptive, and unfair practices by debt collectors. Familiarizing yourself with the FDCPA can empower you to navigate these interactions more effectively.

Impact on Future Borrowing Opportunities

A history of past-due private student loans significantly impacts your creditworthiness and future borrowing opportunities. Lenders use your credit report to assess your risk, and a record of missed or late payments dramatically reduces your credit score. This can make it challenging, if not impossible, to secure future loans, including mortgages, auto loans, and even credit cards. The lower your credit score, the higher the interest rates you’ll likely face on any future borrowing. This can create a vicious cycle, making it increasingly difficult to manage your finances and repay existing debts. For instance, someone with a significantly damaged credit score might be denied a mortgage, preventing them from purchasing a home.

Resources for Borrowers Facing Financial Hardship

Facing financial hardship doesn’t necessitate defaulting on your loans. Several resources can help borrowers navigate difficult financial situations and explore options for managing their student loan debt. These resources include non-profit credit counseling agencies that offer debt management plans, government programs designed to assist individuals facing financial difficulties, and the lender’s own hardship programs, which may offer temporary forbearance or loan modifications. It’s advisable to explore all available options before resorting to defaulting on your loans. Contacting your lender directly to discuss your financial situation is often the first and most effective step. They may be able to offer solutions tailored to your specific circumstances, such as temporary payment reductions or extended repayment plans.

Preventing Future Delinquency

Avoiding future delinquency on your private student loans requires a proactive approach to managing your finances. This involves understanding your spending habits, creating a realistic budget, and utilizing available financial planning tools. By implementing these strategies, you can gain control of your finances and significantly reduce the risk of future loan defaults.

Effective budgeting is crucial for preventing future loan delinquency. It allows you to track your income and expenses, identify areas where you can cut back, and ensure that you have enough money to meet your loan payments each month. Without a well-defined budget, it’s easy to overspend and find yourself struggling to make your loan payments on time.

Effective Budgeting Techniques

A well-structured budget involves carefully tracking all income and expenses. Start by listing all sources of income, including your salary, part-time jobs, or any other regular income streams. Then, meticulously track all expenses, categorizing them into essential needs (housing, food, transportation), discretionary spending (entertainment, dining out), and debt payments (student loans, credit cards). Use a budgeting app, spreadsheet, or even a simple notebook to keep accurate records. Regularly review your budget to identify areas where you can reduce spending or increase income. For example, if you find that you’re spending too much on entertainment, you might consider reducing your outings or finding more affordable alternatives. Similarly, if you have extra skills, exploring freelance work or part-time opportunities could help boost your income.

Financial Planning Tools

Several financial planning tools can assist in managing debt and preventing delinquency. Budgeting apps, such as Mint or YNAB (You Need A Budget), automate the tracking of income and expenses, providing a clear picture of your financial situation. These apps often offer features like budgeting tools, debt tracking, and financial goal setting. Spreadsheet software like Microsoft Excel or Google Sheets can also be used to create customized budgets and track financial progress. Personal finance websites and calculators provide resources and tools for debt management, budgeting, and financial planning. These tools offer valuable insights into debt repayment strategies and help borrowers create a personalized plan to manage their student loans effectively. For instance, a debt snowball or debt avalanche calculator can help determine the most efficient method for paying off multiple debts.

Strategies for Improving Financial Literacy and Responsible Debt Management

Improving financial literacy is paramount to responsible debt management. This involves educating yourself about personal finance topics, such as budgeting, saving, investing, and debt management. Numerous resources are available, including online courses, workshops, books, and financial literacy websites. These resources can help you understand the complexities of personal finance and develop effective strategies for managing your money. Consider attending workshops or seminars offered by your university, local community centers, or financial institutions. These often provide practical advice and tools for improving your financial literacy. Reading personal finance books or articles can also significantly enhance your understanding of debt management and budgeting. Finally, seeking guidance from a financial advisor can provide personalized advice tailored to your specific financial situation.

Creating a Personal Budget: A Step-by-Step Guide

Creating a personal budget is a crucial step in preventing future loan delinquency. Follow these steps to build an effective budget:

- Track your income: List all sources of income, including your salary, part-time jobs, and any other regular income streams. Be precise and include any bonuses or extra income you might receive.

- Track your expenses: For at least a month, meticulously record every expense. Categorize them into essential needs, discretionary spending, and debt payments.

- Create a budget: Based on your income and expenses, create a budget that allocates funds to each category. Ensure that your essential expenses are covered, and that you allocate sufficient funds for your loan payments.

- Identify areas for improvement: Analyze your budget to pinpoint areas where you can cut back on spending. Consider reducing discretionary spending or finding more affordable alternatives.

- Set financial goals: Set realistic financial goals, such as paying off your student loans within a specific timeframe. This will provide motivation and direction for your budgeting efforts.

- Regularly review and adjust: Regularly review your budget and make adjustments as needed. Your financial situation may change over time, so it’s important to keep your budget updated.

Debt Consolidation and Refinancing

Managing past-due private student loans can be challenging, but exploring debt consolidation and refinancing options might offer relief. These strategies aim to simplify repayment by combining multiple loans into one or securing a new loan with more favorable terms. Understanding the nuances of each is crucial for making informed decisions.

Debt consolidation involves combining multiple loans into a single loan with a new payment schedule. Refinancing, on the other hand, replaces your existing loan with a new one, potentially offering a lower interest rate, different repayment term, or both. Both options can streamline payments, but they differ significantly in their implications.

Debt Consolidation Benefits and Drawbacks

Debt consolidation can simplify repayment by reducing the number of monthly payments and potentially lowering your monthly payment amount. However, it might not always result in lower overall interest costs, especially if the new loan carries a higher interest rate than some of your existing loans. Furthermore, consolidating loans could extend the repayment period, leading to paying more interest in the long run. The benefits are primarily in the simplification of the repayment process, making it easier to manage your finances.

Refinancing Benefits and Drawbacks

Refinancing allows you to potentially secure a lower interest rate, shortening the repayment period and reducing the total interest paid. A lower interest rate can significantly decrease your overall loan cost. However, refinancing typically involves a new credit check, which could impact your credit score temporarily. Additionally, some refinancing options may have prepayment penalties, making it costly to pay off the loan early. Eligibility also depends on your creditworthiness and income.

Examples of Lenders Offering Consolidation or Refinancing Services

Several lenders specialize in student loan refinancing and consolidation. Examples include companies like SoFi, Earnest, and CommonBond. These are just a few, and many other financial institutions offer similar services. It’s important to compare offers from multiple lenders before making a decision. Note that lender availability and offered products may vary by location and eligibility criteria.

Factors Lenders Consider When Evaluating Applications

Lenders assess several factors when evaluating applications for consolidation or refinancing. These typically include your credit score, debt-to-income ratio, income stability, and educational background. A strong credit history and a low debt-to-income ratio significantly increase the likelihood of approval and favorable terms. Your loan history, including the performance of your existing student loans, also plays a crucial role. Lenders want to ensure that you have the capacity to repay the new loan responsibly.

Closing Summary

Successfully managing past-due private student loans requires proactive engagement, informed decision-making, and a commitment to long-term financial health. By understanding the available options, negotiating effectively with lenders, and implementing responsible financial practices, borrowers can mitigate the negative consequences of delinquency and pave the way for a brighter financial future. Remember, seeking professional financial advice is crucial when navigating complex debt situations.

Detailed FAQs

What happens if I can’t make my private student loan payments?

Late payments will negatively impact your credit score and may lead to collection efforts by the lender or a debt collection agency. Contact your lender immediately to explore options like deferment, forbearance, or a repayment plan.

Can I negotiate a lower payment amount with my lender?

Yes, many lenders are willing to negotiate. Prepare a detailed explanation of your financial hardship and propose a realistic repayment plan. A written letter outlining your situation is often helpful.

Will past-due loans affect my ability to get a mortgage or other loans in the future?

Yes, significantly. Past-due loans severely damage your credit score, making it difficult to qualify for future loans with favorable terms. Addressing and resolving the past-due balances is crucial for improving your creditworthiness.

What are the legal consequences of not repaying private student loans?

Lenders can take legal action, including wage garnishment or lawsuits, to recover the debt. This can significantly impact your finances and credit history. Consult with a legal professional if you are facing legal action.