Navigating the complexities of student loan debt can feel overwhelming, but understanding refinancing options can significantly impact your financial future. This guide explores current refinance rates for student loans, outlining key factors influencing costs, eligibility criteria, and the process itself. We’ll delve into the benefits and drawbacks of refinancing, comparing various lenders and highlighting potential pitfalls to avoid. Ultimately, the goal is to empower you with the knowledge to make informed decisions about managing your student loan debt.

We will examine the interplay between credit scores, loan amounts, and co-signers in determining your interest rate. The differences between fixed and variable rates will be clarified, alongside a detailed comparison of various lenders, their fees, and customer service. We’ll also explore the potential loss of federal loan benefits upon refinancing, offering alternative strategies for debt management if refinancing isn’t the optimal choice. By the end, you’ll have a clear understanding of whether refinancing is right for you and how to proceed.

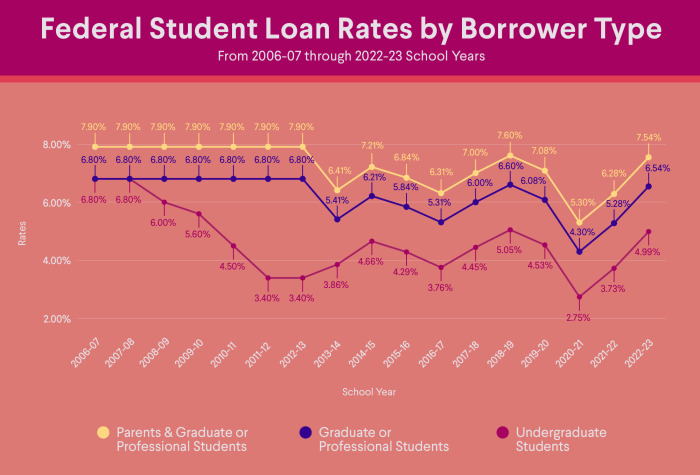

Current Student Loan Refinancing Rates

Student loan refinancing can significantly reduce your monthly payments and save you money over the life of your loan. However, securing the best rates requires understanding the current market and the factors influencing lender decisions. This section will provide an overview of current refinancing rates from several major lenders, along with a detailed explanation of the key factors affecting your eligibility and interest rate.

Understanding the nuances of student loan refinancing is crucial for making informed financial decisions. Careful consideration of various lenders, interest rates, and loan terms is vital to securing the best possible outcome.

Student Loan Refinancing Rates from Major Lenders

The following table presents a snapshot of current refinancing rates offered by five major lenders. It’s crucial to remember that these rates are subject to change and are based on specific criteria. Always check the lender’s website for the most up-to-date information.

| Lender | APR Range | Loan Terms (Years) | Eligibility Requirements (Summary) |

|---|---|---|---|

| SoFi | 6.99% – 18.99% | 5-20 | Good credit, minimum credit score (varies), income verification. |

| Earnest | 6.49% – 18.99% | 5-15 | Good credit, minimum credit score (varies), income verification. Co-signer may be available. |

| LendKey | 7.49% – 18.99% | 5-15 | Credit score, income verification, loan amount, debt-to-income ratio. |

| CommonBond | 6.99% – 18.99% | 5-15 | Good to excellent credit, income verification, employment history. |

| Splash Financial | 7.99% – 18.99% | 5-15 | Creditworthiness, income, debt-to-income ratio, loan amount. |

Note: APR (Annual Percentage Rate) includes interest and fees. Specific rates depend on creditworthiness, loan amount, and other factors. These are examples and may not reflect current offerings. Always consult the lender’s website for the most current information.

Factors Influencing Student Loan Refinance Rates

Several factors significantly impact the interest rate you qualify for when refinancing student loans. Understanding these factors can help you improve your chances of securing a lower rate.

Your credit score is a primary determinant. Lenders use your credit history to assess your risk. A higher credit score (generally above 700) typically translates to a lower interest rate. Your credit utilization (the amount of credit you’re using compared to your total available credit) also plays a role. Keeping your credit utilization low is beneficial.

The amount you’re refinancing also matters. Larger loan amounts may be associated with slightly higher rates due to increased risk for the lender. The type of loans you are refinancing (federal vs. private) can also influence rates. Federal loans may have different eligibility requirements compared to private loans.

Having a co-signer with strong credit can significantly improve your chances of approval and securing a lower rate. A co-signer shares the responsibility for repayment, reducing the lender’s risk. However, this also means the co-signer’s credit will be impacted if payments are missed.

Your income and debt-to-income ratio are other critical factors. Lenders want to ensure you can comfortably afford the monthly payments. A stable income and a low debt-to-income ratio generally lead to more favorable interest rates. Your employment history is also often considered, demonstrating financial stability.

Fixed vs. Variable Interest Rates

Refinanced student loans typically come with either a fixed or variable interest rate. Understanding the differences is crucial for choosing the right option for your financial situation.

A fixed interest rate remains constant throughout the loan’s term. This predictability makes budgeting easier, as your monthly payments will not change. However, fixed rates are usually slightly higher than variable rates initially.

A variable interest rate fluctuates based on market conditions. This means your monthly payments can increase or decrease over time. While variable rates may start lower than fixed rates, the potential for increases introduces uncertainty into your budget. Variable rates are typically tied to an index, such as the LIBOR or SOFR.

The best choice depends on your risk tolerance and financial outlook. If you prefer stability and predictability, a fixed rate is generally recommended. If you’re comfortable with some uncertainty and believe interest rates may decrease, a variable rate might be considered, but with careful monitoring of market conditions.

Eligibility Criteria for Refinancing

Successfully refinancing your student loans hinges on meeting specific eligibility requirements set by lenders. These criteria are designed to assess your creditworthiness and ensure you can manage the new loan terms. Factors like credit score, debt-to-income ratio, and the type of student loan you possess all play a crucial role in the approval process.

Understanding these criteria is vital before applying, as failing to meet them can lead to rejection and wasted time. This section will detail the common requirements and provide insights into why applications might be denied.

Credit Score Requirements

Lenders use credit scores as a primary indicator of your creditworthiness. A higher credit score generally translates to better loan terms and a higher likelihood of approval. While specific requirements vary among lenders, a general guideline is that a credit score of at least 670 is often preferred for favorable interest rates. Lenders with more stringent requirements might demand scores above 700, while some may accept applicants with scores as low as 600, but typically with higher interest rates and stricter terms. For example, a lender like SoFi might target borrowers with higher credit scores for their most competitive rates, while another lender might offer options for those with slightly lower scores, albeit at a higher cost.

Debt-to-Income Ratio’s Impact

Your debt-to-income (DTI) ratio, which compares your monthly debt payments to your gross monthly income, is another critical factor. A lower DTI ratio indicates a greater capacity to manage additional debt. Lenders generally prefer applicants with a DTI ratio below 43%, though this can vary depending on the lender and the overall risk assessment. A high DTI ratio suggests that you are already heavily burdened with debt, making it riskier for lenders to approve a refinance. For instance, an applicant with a DTI ratio of 55% is significantly less likely to be approved than someone with a DTI ratio of 30%, even if their credit score is comparable.

Eligible Student Loan Types

Not all student loans are eligible for refinancing. Most lenders refinance private student loans, while federal student loans are generally not eligible for private refinancing. However, some lenders might offer options for consolidating federal loans into a private refinance loan, but this often comes with the loss of federal protections and benefits associated with federal student loan programs. It’s crucial to carefully consider the implications of losing federal protections before choosing a private refinance option. Understanding which type of loan you have is therefore a critical first step.

Reasons for Refinance Application Rejection

Several factors can lead to a refinance application being rejected. Understanding these common reasons can help you prepare a stronger application in the future.

- Insufficient Credit Score: A credit score below the lender’s minimum requirement is a frequent cause for rejection.

- High Debt-to-Income Ratio: A DTI ratio exceeding the lender’s acceptable limit significantly reduces the chances of approval.

- Limited Income Verification: Inability to provide sufficient proof of income can lead to rejection.

- Negative Credit History: Bankruptcies, foreclosures, or a history of late payments can negatively impact your application.

- Insufficient Loan Amount: Some lenders have minimum loan amounts for refinancing, and applications with loans below that threshold may be rejected.

- Ineligible Loan Type: Attempting to refinance ineligible federal student loans through private lenders will result in rejection.

Comparison of Refinancing Lenders

Choosing the right lender for student loan refinancing is crucial, as fees and interest rates can significantly impact your overall cost savings. This section compares several prominent lenders, focusing on their fees, customer service, loan options, and any special offers they may provide. Understanding these differences will help you make an informed decision.

Lender Fee Comparison

Different lenders employ varying fee structures. These fees can include application fees, origination fees (a percentage of the loan amount), and prepayment penalties (charges for paying off the loan early). It’s essential to compare these fees across lenders to determine the true cost of refinancing. Some lenders may advertise low interest rates, but high fees could negate any savings. Always review the loan documents carefully to understand all associated costs.

Lender Comparison Table

The following table compares three hypothetical lenders – Lender A, Lender B, and Lender C – based on customer service ratings (from a hypothetical independent survey), loan options, and any current special offers. Note that these are examples and actual lender offerings may vary.

| Lender | Customer Service Rating (out of 5) | Loan Options | Special Offers | Application Fee | Origination Fee | Prepayment Penalty |

|---|---|---|---|---|---|---|

| Lender A | 4.2 | Fixed & Variable Rate, 5-15 year terms | 0% APR for the first 3 months | $0 | 1% | None |

| Lender B | 3.8 | Fixed Rate only, 10-20 year terms | Cash back reward program | $50 | 0.75% | 2% of remaining balance |

| Lender C | 4.5 | Fixed & Variable Rate, 5-10 year terms | Rate discount for autopay | $25 | 0.5% | None |

Hypothetical Refinancing Scenario

Let’s consider a hypothetical scenario: John has $50,000 in student loan debt with a 7% interest rate. He’s considering refinancing with each of the lenders above. Assuming a 10-year repayment period and the fees Artikeld in the table, we can estimate the total cost for each lender. This example simplifies calculations by not including compounding interest and only considers the listed fees. Actual costs may vary based on individual loan terms and interest rate fluctuations.

For Lender A: Total cost would include the origination fee (1% of $50,000 = $500) plus interest payments based on their offered interest rate.

For Lender B: Total cost would include the application fee ($50), origination fee (0.75% of $50,000 = $375), and potential prepayment penalty depending on when John pays off the loan.

For Lender C: Total cost would include the application fee ($25) and origination fee (0.5% of $50,000 = $250) plus interest payments based on their offered interest rate.

By comparing the total cost (including fees and interest) across the three lenders, John can determine which option offers the greatest long-term savings. This illustrates the importance of considering all associated costs when comparing refinancing offers. Remember to obtain personalized quotes from each lender for an accurate comparison.

Impact of Refinancing on Federal Loan Benefits

Refinancing your federal student loans can offer lower interest rates and potentially save you money over the life of your loan. However, it’s crucial to understand that this decision comes with significant trade-offs. By refinancing, you’re essentially trading the protections and benefits afforded by federal student loan programs for a potentially lower monthly payment from a private lender. This decision should not be taken lightly, as the loss of these benefits can have long-term financial repercussions.

Refinancing federal student loans typically means giving up several key advantages associated with federal loan programs. These benefits, often overlooked until needed, can significantly impact your ability to manage your debt, especially during periods of financial hardship. Understanding these implications is paramount before making the decision to refinance.

Loss of Federal Student Loan Benefits

Refinancing your federal student loans with a private lender will eliminate access to federal repayment programs designed to help borrowers manage their debt. This includes income-driven repayment (IDR) plans, which base your monthly payment on your income and family size. These plans often lead to loan forgiveness after a certain number of qualifying payments. You will also lose access to federal forbearance and deferment options, which provide temporary pauses in payments during times of financial difficulty, such as unemployment or illness. For example, a borrower struggling with unemployment might find themselves unable to make payments on a refinanced loan, leading to delinquency and potential damage to their credit score, unlike if they still held a federal loan with access to forbearance. The potential for negative consequences underscores the importance of careful consideration before refinancing.

Impact on Loan Forgiveness Programs

Many federal student loan programs offer loan forgiveness after a certain number of qualifying payments, often tied to public service employment or specific career fields. Refinancing your federal loans eliminates your eligibility for these forgiveness programs. Consider, for example, a teacher who has made 10 years of payments on their federal student loans and is on track for Public Service Loan Forgiveness (PSLF). If they refinance, they forfeit the potential for loan forgiveness, even if they continue to work in public service. The financial implications of losing this forgiveness could amount to tens of thousands of dollars, depending on the loan amount. This loss can significantly affect long-term financial planning.

Financial Consequences of Losing Federal Loan Benefits

The financial consequences of losing federal loan benefits can be substantial and far-reaching. For instance, a borrower who refinances a $50,000 federal loan and loses access to an IDR plan might find their monthly payments significantly higher than if they had kept their federal loans. This could lead to financial strain, potentially impacting their ability to save for retirement, purchase a home, or handle unexpected expenses. Furthermore, if they experience a period of unemployment and are unable to make payments on their refinanced loan, they risk default and the associated negative impacts on their credit score. The long-term consequences of default could include difficulty securing loans, credit cards, or even renting an apartment. This illustrates the potential severity of the financial risks associated with refinancing federal student loans.

The Refinancing Process Step-by-Step

Refinancing your student loans can be a complex process, but understanding the steps involved can make it significantly less daunting. This section Artikels the key stages, from initial application to receiving your new loan disbursement, providing a clear roadmap for navigating the refinance journey. Careful planning and preparation are essential for a smooth and successful refinancing experience.

The student loan refinancing process generally follows these steps:

- Check your credit score and financial health. Before applying, review your credit report for any errors and ensure your finances are in order. A higher credit score generally qualifies you for better interest rates.

- Research and compare lenders. Explore various lenders offering student loan refinancing, comparing interest rates, fees, and repayment terms. Consider factors such as your creditworthiness and the loan amount.

- Complete the application. Once you’ve chosen a lender, carefully fill out their application form, providing accurate and complete information.

- Provide necessary documentation. Lenders will require specific documents to verify your identity, income, and student loan debt. This typically includes pay stubs, tax returns, and student loan statements.

- Await lender approval. The lender will review your application and supporting documentation. The approval process can take several days or weeks.

- Review loan terms and conditions. Carefully examine the loan agreement, paying close attention to interest rates, fees, repayment schedules, and any other terms.

- Sign the loan documents. Once you’ve reviewed and understood the terms, sign the loan documents electronically or physically, as required by the lender.

- Receive loan disbursement. After signing the documents, the lender will disburse the refinanced loan funds, typically directly to your previous student loan servicer(s).

Required Documentation for Refinancing

Gathering the necessary documentation upfront significantly streamlines the application process. Incomplete applications can lead to delays. It is advisable to organize all required documents before starting the application.

Typical documentation required includes:

- Government-issued photo ID: This verifies your identity.

- Social Security number: Necessary for verification purposes.

- Proof of income: Pay stubs, W-2 forms, or tax returns are commonly accepted.

- Student loan statements: These provide details of your existing student loan debt.

- Bank statements: These can help lenders assess your financial stability.

- Employment verification: Some lenders may require verification of your employment status.

Comparing Loan Offers from Multiple Lenders

Comparing loan offers is crucial for securing the best possible terms. This involves a thorough analysis of several key factors to determine which lender provides the most advantageous refinancing option. Don’t rush this step; a little extra time can save you considerable money over the life of your loan.

Key factors to consider when comparing loan offers include:

- Interest rate: The annual percentage rate (APR) is a crucial factor, as it directly impacts the total cost of your loan.

- Fees: Origination fees, prepayment penalties, and other fees can add to the overall cost. Compare these fees across different lenders.

- Repayment terms: Consider the loan term length and its impact on your monthly payments and total interest paid.

- Customer service: Look for lenders with a strong reputation for responsive and helpful customer service.

- Loan forgiveness options (if applicable): Some lenders may offer loan forgiveness programs under specific circumstances.

Alternatives to Refinancing

Refinancing your student loans isn’t the only path to managing your debt. Several alternative strategies can help you lower your monthly payments or pay off your loans faster, depending on your individual financial situation and loan types. These options often involve working directly with your loan servicer and may offer benefits not available through refinancing, such as government protections.

Exploring these alternatives before refinancing is crucial, as refinancing often involves forfeiting certain federal loan benefits. Careful consideration of your long-term financial goals and the implications of each approach is essential.

Income-Driven Repayment Plans

Income-driven repayment (IDR) plans adjust your monthly student loan payments based on your income and family size. This can significantly lower your monthly payment, making your debt more manageable, especially during periods of lower income. Several IDR plans exist, each with its own eligibility criteria and payment calculation method. These plans typically lead to loan forgiveness after a set number of years, usually 20 or 25, depending on the plan and your loan type. However, the forgiven amount is considered taxable income.

For example, let’s say your monthly payment on a $50,000 loan is $600 under a standard repayment plan. An IDR plan might reduce this to $300 per month, freeing up $300 monthly for other expenses or debt reduction. Over the life of the loan, this could lead to significant savings, although the ultimate cost may be higher due to the interest accruing over a longer period. The forgiveness aspect, while appealing, should be carefully weighed against the potential tax implications.

Student Loan Consolidation

Consolidation combines multiple federal student loans into a single loan with a new interest rate and repayment schedule. While this doesn’t lower your interest rate (the new rate is a weighted average of your existing rates), it simplifies repayment by dealing with only one monthly payment. It can also be a stepping stone to an IDR plan, offering a more manageable payment schedule before pursuing forgiveness.

Consider this scenario: You have three federal loans with interest rates of 4%, 5%, and 6%, and monthly payments of $200, $150, and $250 respectively. Consolidating these loans might result in a single loan with a weighted average interest rate (around 5%), and a potentially simplified monthly payment schedule. While this won’t reduce the total interest paid, it streamlines the repayment process. This makes it easier to track payments and budget effectively.

Comparison of Refinancing vs. Alternatives

| Feature | Refinancing | Income-Driven Repayment | Consolidation |

|---|---|---|---|

| Interest Rate | Potentially lower (but may be higher) | No change | Weighted average of existing rates |

| Monthly Payment | Potentially lower | Lower based on income | Potentially simplified, but not necessarily lower |

| Loan Forgiveness | None | Possible after 20-25 years (taxable) | None |

| Federal Loan Benefits | Lost | Retained | Retained |

Note: The potential savings from each method depend heavily on individual circumstances, including interest rates, loan amounts, income, and chosen repayment plan. It’s crucial to perform your own calculations using your specific loan details.

Illustrative Examples of Refinancing Scenarios

Refinancing your student loans can significantly impact your monthly payments and the total interest you pay over the life of the loan. The optimal outcome depends heavily on factors such as your credit score, the size of your loan, and the prevailing interest rates. The following examples illustrate how these factors interact to influence your refinancing decision.

Understanding these scenarios helps you make an informed choice that aligns with your long-term financial goals. Remember that these are illustrative examples and your specific situation may vary.

Impact of Credit Score on Refinancing Outcomes

A higher credit score typically qualifies you for lower interest rates. Consider two borrowers, both seeking to refinance a $50,000 student loan over a 10-year term. Borrower A has an excellent credit score (750+), securing a 5% interest rate. Borrower B has a fair credit score (660), resulting in a 7% interest rate. Borrower A’s monthly payment would be approximately $530, and their total interest paid would be around $13,600. Borrower B’s monthly payment would be approximately $580, and their total interest paid would be around $17,600. This demonstrates a substantial difference in overall cost driven solely by credit score.

Impact of Loan Amount on Refinancing Outcomes

The size of your loan significantly affects the total interest paid, even with the same interest rate. Let’s assume two borrowers, both with excellent credit scores (750+), refinancing over a 10-year term at a 5% interest rate. Borrower C refinances a $30,000 loan, resulting in a monthly payment of approximately $315 and total interest paid of roughly $7,800. Borrower D refinances a $70,000 loan, leading to a monthly payment of approximately $745 and total interest paid of around $22,200. This highlights the substantial impact of loan size on the overall cost of refinancing.

Impact of Interest Rate and Loan Term on Refinancing Outcomes

Interest rates and loan terms are interconnected. Imagine Borrower E refinancing a $50,000 loan. Scenario 1: A 5% interest rate over 10 years results in a monthly payment of approximately $530 and total interest paid of around $13,600. Scenario 2: A 6% interest rate over the same 10-year term increases the monthly payment to approximately $560 and the total interest paid to around $16,000. Scenario 3: Keeping the 5% interest rate but extending the term to 15 years reduces the monthly payment to approximately $390, but increases the total interest paid to approximately $18,500. This demonstrates the trade-off between lower monthly payments and increased total interest.

Long-Term Financial Implications of Refinancing Decisions

The long-term financial implications of refinancing are significant. Lower monthly payments provide immediate relief, but extending the loan term can lead to paying significantly more interest over the life of the loan. Conversely, choosing a shorter loan term with higher monthly payments will result in less interest paid overall, but could strain your budget in the short-term. Careful consideration of your financial situation and long-term goals is crucial before making a refinancing decision. For example, if you anticipate a significant increase in income in the near future, a shorter-term loan with higher monthly payments might be a better option to minimize long-term interest costs. Conversely, if your income is relatively stable, a longer-term loan with lower monthly payments might provide more financial flexibility.

Final Wrap-Up

Refinancing student loans can offer substantial long-term savings, but it’s crucial to carefully weigh the pros and cons. Understanding the factors influencing interest rates, eligibility requirements, and potential loss of federal benefits is paramount. By comparing lenders, exploring alternative debt management strategies, and meticulously evaluating your individual financial situation, you can make an informed decision that aligns with your long-term financial goals. Remember to thoroughly research and compare offers before committing to a refinance plan.

Expert Answers

What is the average interest rate for student loan refinancing?

Average interest rates vary greatly depending on credit score, loan amount, and lender. It’s best to check current rates from multiple lenders for a personalized estimate.

Can I refinance federal student loans?

Yes, but be aware that refinancing federal loans often means losing access to federal benefits like income-driven repayment plans and potential forgiveness programs.

How long does the refinancing process take?

The process typically takes several weeks, from application to loan disbursement. Processing times vary depending on the lender and the complexity of your application.

What documents are typically required for refinancing?

Lenders usually require proof of income, credit report, and details of your existing student loans.

What happens if my refinance application is rejected?

Reasons for rejection include low credit score, high debt-to-income ratio, or insufficient income. You may need to improve your credit score or explore alternative debt management options.