Navigating the complexities of student loan debt can feel overwhelming, but refinancing offers a potential pathway to lower monthly payments and faster debt repayment. This guide focuses on refinancing your student loans with Sallie Mae, a prominent player in the student loan market. We’ll explore eligibility requirements, interest rates, the application process, and crucial comparisons with other lenders to help you make an informed decision.

Understanding the nuances of Sallie Mae’s refinancing program is key to determining if it aligns with your financial goals. We will delve into the benefits and potential drawbacks, providing a comprehensive overview to empower you with the knowledge needed to confidently navigate this important financial step.

Sallie Mae Refinancing Eligibility Requirements

Sallie Mae’s student loan refinancing program offers borrowers the opportunity to consolidate their federal and private student loans into a single, potentially lower-interest loan. However, eligibility hinges on several key factors, including income, credit score, and the types of loans you possess. Understanding these requirements is crucial before applying.

Income Requirements for Sallie Mae Student Loan Refinancing

Sallie Mae requires applicants to demonstrate a stable income to ensure their ability to repay the refinanced loan. While they don’t publicly state a minimum income threshold, a higher income generally improves your chances of approval and may lead to more favorable interest rates. Lenders assess income stability through verification of employment history, pay stubs, and tax returns. A consistent income stream, demonstrating financial responsibility, significantly strengthens your application.

Credit Score Thresholds and Their Impact on Approval

Your credit score is a critical factor in Sallie Mae’s refinancing decision. A higher credit score typically results in a lower interest rate. While Sallie Mae doesn’t specify a minimum credit score, a score above 660 is generally considered favorable. Scores below this threshold may result in denial or higher interest rates. Improving your credit score before applying is advisable. Factors like payment history, credit utilization, and length of credit history significantly impact your credit score and refinancing eligibility.

Eligible Student Loan Types for Sallie Mae Refinancing

Sallie Mae refinancings typically encompass both federal and private student loans. However, it’s important to note that federal loans lose their federal protections once refinanced. This means benefits like income-driven repayment plans and potential forgiveness programs may no longer be accessible. Before refinancing federal loans, carefully weigh the pros and cons. Sallie Mae typically doesn’t refinance Parent PLUS loans.

Documentation Needed to Apply for Refinancing

To successfully apply for Sallie Mae student loan refinancing, you’ll need to provide supporting documentation. This commonly includes:

- Proof of Identity (e.g., Driver’s License, Passport)

- Social Security Number

- Current Pay Stubs or Bank Statements demonstrating income

- Tax Returns (for income verification)

- Student Loan Information (loan numbers, balances, lenders)

Providing complete and accurate documentation expedites the application process and increases your chances of approval.

Comparison of Sallie Mae’s Refinancing Eligibility Criteria with Other Major Lenders

| Lender | Minimum Credit Score (approx.) | Income Requirements | Eligible Loan Types |

|---|---|---|---|

| Sallie Mae | 660+ (unofficial) | Stable income demonstrated through documentation | Federal and Private (excluding Parent PLUS loans, generally) |

| SoFi | 680+ (approx.) | Stable income required | Federal and Private |

| Earnest | 650+ (approx.) | Stable income required | Federal and Private |

| LendKey | Variable, often lower than others | Stable income required | Federal and Private |

*Note: Minimum credit score requirements are estimates and can vary based on individual circumstances. Always check directly with the lender for the most up-to-date information.

Interest Rates and Loan Terms

Sallie Mae’s student loan refinancing program offers borrowers the opportunity to consolidate multiple federal and/or private student loans into a single, potentially lower-interest loan. Understanding the interest rates and repayment terms is crucial for making an informed decision and minimizing the overall cost of repayment. This section will detail the key factors influencing these aspects of Sallie Mae refinancing.

Sallie Mae’s interest rates are variable, meaning they fluctuate based on market conditions. Therefore, the rate you receive will depend on several factors, most notably your credit score and the loan amount. Generally, borrowers with higher credit scores and larger loan amounts may qualify for lower interest rates. Repayment terms, on the other hand, offer flexibility to borrowers, allowing them to tailor their monthly payments to their financial capacity. However, the choice of repayment term significantly impacts the total interest paid over the life of the loan.

Sallie Mae Interest Rates and Credit Scores

Sallie Mae does not publicly list a fixed rate chart correlating specific credit scores to interest rates. The rate offered is determined by a proprietary algorithm that considers a multitude of factors beyond credit score, including the borrower’s income, debt-to-income ratio, and the type and amount of loan being refinanced. While a higher credit score generally leads to a lower interest rate, the exact relationship isn’t linear and is influenced by other variables. For example, a borrower with a 750 credit score might receive a lower rate than another with a 720 credit score if the former has a significantly higher income and lower debt. To obtain a personalized rate quote, applicants must complete Sallie Mae’s online application process.

Sallie Mae Repayment Terms

Sallie Mae typically offers a range of repayment terms, usually spanning from 5 to 20 years. Choosing a shorter repayment term results in higher monthly payments but significantly reduces the total interest paid over the life of the loan. Conversely, opting for a longer repayment term lowers monthly payments but increases the overall interest paid. For instance, a $50,000 loan refinanced at 6% interest would have a monthly payment of approximately $966 for a 5-year term and $360 for a 20-year term. However, the total interest paid would be considerably less with the shorter term.

Impact of Repayment Term Length on Total Interest

The choice between a shorter and longer repayment term involves a trade-off between affordability and total cost. A shorter term leads to less interest paid overall due to less time accruing interest, while a longer term results in lower monthly payments but significantly higher total interest charges. This difference can amount to thousands of dollars over the life of the loan. Consider the example above: the 5-year loan would result in approximately $9,000 in interest paid, while the 20-year loan would accrue nearly $36,000 in interest. Therefore, carefully weighing monthly affordability against long-term cost is crucial.

Potential Fees Associated with Sallie Mae Student Loan Refinancing

While Sallie Mae generally doesn’t charge origination fees, it’s crucial to be aware of potential late payment fees. These fees can vary and are typically Artikeld in the loan agreement. It’s vital to review the terms and conditions carefully to understand all associated costs before proceeding with refinancing. Additionally, there might be penalties for early payoff, although this is less common.

Factors Influencing Sallie Mae’s Interest Rate Offerings

Several key factors influence the interest rate a borrower receives from Sallie Mae. Understanding these factors can help borrowers improve their chances of securing a favorable rate.

- Credit Score: A higher credit score generally leads to a lower interest rate.

- Debt-to-Income Ratio (DTI): A lower DTI indicates a greater capacity to repay the loan, often resulting in a better interest rate.

- Income: Higher income often correlates with a lower interest rate, demonstrating greater financial stability.

- Loan Amount: Larger loan amounts might sometimes qualify for slightly better rates.

- Type of Loan Being Refinanced: The mix of federal and private loans being refinanced can influence the final rate.

- Market Interest Rates: Prevailing market conditions significantly affect interest rates offered by lenders, including Sallie Mae.

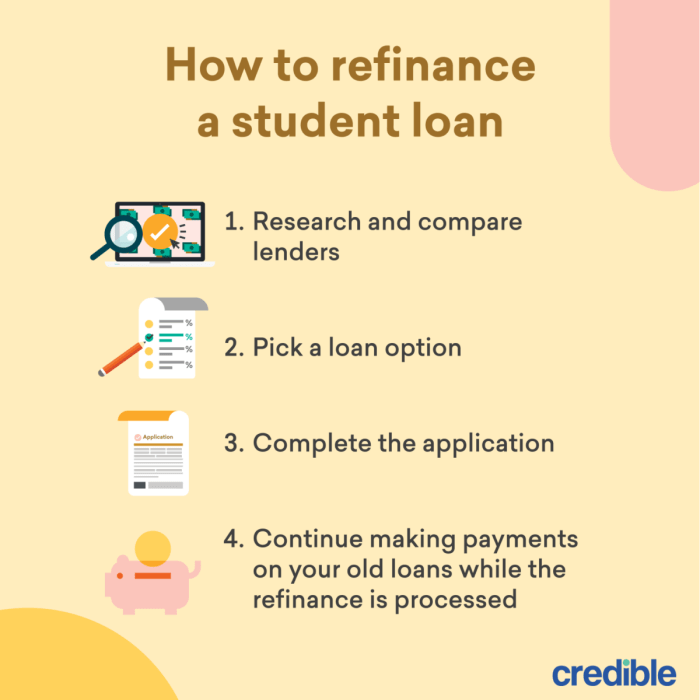

The Application Process

Applying for Sallie Mae student loan refinancing is a straightforward process, but careful preparation can significantly streamline the experience. This section details the steps involved, the information you’ll need, and tips for a smooth application.

The application process itself is largely online, making it convenient and accessible. Sallie Mae provides a user-friendly interface designed to guide you through each stage. However, gathering the necessary information beforehand is crucial for efficiency.

Step-by-Step Application Guide

The Sallie Mae refinancing application generally follows these steps:

- Create an Account or Log In: If you don’t already have a Sallie Mae account, you’ll need to create one. This involves providing basic personal information.

- Provide Personal and Financial Information: This stage requires detailed information, including your Social Security number, employment history, income details, and existing student loan information. Accuracy is paramount at this stage.

- Choose Your Loan Terms: Once your application is reviewed, you’ll be presented with various loan offers based on your eligibility. You’ll need to select the loan term and interest rate that best suits your financial situation.

- Review and Sign Your Loan Documents: Carefully review all loan documents before electronically signing them. Understand the terms and conditions before proceeding.

- Fund Your Loan: After signing, the funds will be disbursed to your existing student loan provider(s) to pay off your previous loan(s).

Comparing Sallie Mae Loan Offers

Sallie Mae may present multiple loan offers, each with varying interest rates and terms. Careful comparison is essential to select the most advantageous option.

Consider these factors when comparing offers:

- Interest Rate: The interest rate directly impacts the total cost of your loan. A lower rate will save you money over the life of the loan.

- Loan Term: A shorter loan term means higher monthly payments but lower overall interest paid. A longer term means lower monthly payments but higher total interest.

- Fees: Be aware of any origination fees or other charges associated with the loan.

Required Information for Application Completion

To ensure a smooth application, gather the following information beforehand:

- Personal Information: Full name, date of birth, Social Security number, address, and contact information.

- Employment Information: Current employer, job title, income, and employment history.

- Financial Information: Bank account information, credit score (optional but helpful), and details of existing student loans (loan amounts, interest rates, lenders).

- Education Information: Details of your education, including the institutions attended and degrees earned.

Tips for a Smooth Application Process

Following these tips will contribute to a streamlined and efficient application process:

- Complete the application in one sitting if possible: This minimizes the risk of forgetting information or encountering technical difficulties.

- Double-check all information for accuracy: Errors can delay the processing of your application.

- Keep copies of all documents: Maintain records of all submitted documents for your reference.

- Read all loan documents carefully: Understand the terms and conditions before signing.

- Contact Sallie Mae customer service if you have questions: They can assist with any queries or concerns you may have.

Application Checklist

Before you begin the application, ensure you have the following:

- Valid government-issued photo ID

- Social Security number

- Current and previous employment information

- Details of all existing student loans

- Bank account information

- Information about your education

Comparing Sallie Mae Refinancing to Other Options

Choosing the right student loan refinancing lender is crucial, as it significantly impacts your monthly payments and overall repayment costs. While Sallie Mae is a well-known name in student loans, it’s essential to compare its offerings with those of other major lenders before making a decision. This comparison will highlight the advantages and disadvantages of each, empowering you to make an informed choice.

Sallie Mae Refinancing Compared to Competitors

Several lenders compete with Sallie Mae in the student loan refinancing market. These include companies like SoFi, Earnest, and others. Each lender offers varying interest rates, loan terms, and eligibility requirements. A thorough comparison is necessary to determine which lender best suits your individual financial circumstances. Direct comparison of advertised rates is not always sufficient; a complete picture requires examining all associated fees and terms.

Advantages and Disadvantages of Different Lenders

Sallie Mae’s refinancing options often appeal to borrowers due to its established reputation and potentially competitive interest rates. However, other lenders might offer lower rates, more flexible repayment options, or additional benefits like unemployment protection. For instance, SoFi is known for its robust customer service and additional financial products, while Earnest might provide more lenient eligibility criteria. The “best” lender depends entirely on the borrower’s unique needs and financial profile. A borrower with excellent credit might find better rates elsewhere, while one with a less-than-perfect credit history might find Sallie Mae more accommodating.

Evaluating Loan Offers Based on Key Factors

When comparing loan offers, focus on several key factors. Interest rate is paramount, but equally important are loan terms (length of repayment), fees (origination fees, prepayment penalties), and eligibility requirements (credit score, debt-to-income ratio). Consider the total cost of the loan over its lifetime, not just the monthly payment. A slightly higher interest rate with a shorter loan term could result in lower overall interest paid compared to a lower rate with a longer term. Furthermore, carefully review any fine print regarding late payment fees or other potential charges.

Situations Where Sallie Mae Might Not Be the Best Option

Sallie Mae might not be the optimal choice for borrowers with lower credit scores, those seeking exceptionally long repayment terms, or those who prioritize specific features offered by other lenders (e.g., unemployment protection). Borrowers should shop around and compare offers from multiple lenders to ensure they secure the most favorable terms. The competitive landscape encourages lenders to offer attractive deals, so actively comparing options is crucial.

Comparison Table: Sallie Mae vs. Competitors

| Feature | Sallie Mae | SoFi | Earnest |

|---|---|---|---|

| Minimum Credit Score | (Insert Sallie Mae’s minimum credit score requirement) | (Insert SoFi’s minimum credit score requirement) | (Insert Earnest’s minimum credit score requirement) |

| Interest Rates (Example: 5-year fixed) | (Insert example interest rate range) | (Insert example interest rate range) | (Insert example interest rate range) |

| Fees | (Specify any fees, e.g., origination fees) | (Specify any fees) | (Specify any fees) |

| Repayment Options | (List available repayment options) | (List available repayment options) | (List available repayment options) |

Potential Benefits and Risks of Refinancing

Refinancing your student loans with Sallie Mae can offer significant advantages, but it’s crucial to carefully weigh the potential benefits against the risks before making a decision. Understanding both sides of the equation is essential to making an informed choice that aligns with your individual financial circumstances and long-term goals.

Potential Benefits of Refinancing

Refinancing your student loans can lead to substantial savings over the life of your loan. Lower interest rates are the most significant draw, translating directly into reduced monthly payments and a smaller total amount paid over time. Additionally, shorter repayment terms can help you become debt-free faster, although this often means higher monthly payments. These benefits can free up more of your income for other financial priorities like saving for a down payment on a house or investing. For example, a borrower with a $50,000 loan at 7% interest could save thousands of dollars by refinancing to a 4% interest rate.

Potential Risks of Refinancing

While refinancing can offer attractive benefits, it’s essential to acknowledge the potential drawbacks. The most significant risk is the loss of federal student loan benefits. Federal loans often come with protections like income-driven repayment plans and loan forgiveness programs for specific professions. Refinancing with a private lender like Sallie Mae typically converts your federal loans into private loans, eliminating these crucial safeguards. Another risk is the possibility of a higher interest rate if your credit score is lower than it was when you initially took out your loans. This could negate any potential savings from refinancing. Finally, there’s the risk of unforeseen circumstances, like job loss, which could make higher monthly payments difficult to manage.

Scenarios Where Refinancing is Beneficial

Refinancing can be highly advantageous for borrowers with good credit scores and stable incomes who are confident in their ability to maintain consistent payments. Those with high interest rates on their federal loans, especially those who don’t anticipate needing federal loan benefits, may see substantial savings. For instance, a borrower with multiple federal loans at varying interest rates could benefit significantly from consolidating them into a single loan with a lower, fixed interest rate.

Scenarios Where Refinancing is Not Advisable

Refinancing isn’t always the best option. Borrowers with poor credit scores or unstable incomes may face higher interest rates or be denied altogether. Individuals who anticipate needing income-driven repayment plans or loan forgiveness programs in the future should carefully consider the implications of losing these federal benefits. For example, a recent graduate unsure of their career path might regret refinancing if they later qualify for a public service loan forgiveness program.

Examples of Successful and Unsuccessful Refinancing

A successful refinancing example could be a borrower with excellent credit who consolidates multiple high-interest federal loans into a single, lower-interest private loan, significantly reducing their monthly payments and overall interest paid. Conversely, an unsuccessful example might be a borrower with a fluctuating income who refinances to a shorter repayment term with higher monthly payments, only to struggle to make payments during a period of unemployment.

Visual Representation of Long-Term Savings

The illustration would be a line graph showing the cumulative amount paid over a 10-year period for two scenarios: one where a borrower refinances their loan to a lower interest rate, and one where they do not. The x-axis would represent time (in years), and the y-axis would represent the cumulative amount paid. The “no refinance” line would show a steeper, upward-sloping curve representing the higher total cost due to higher interest. The “refinance” line would show a less steep curve, demonstrating the lower cumulative cost resulting from the lower interest rate. A clear legend would distinguish the two lines, and numerical values at key points (e.g., year 5 and year 10) would highlight the substantial difference in total cost between the two scenarios. The graph would visually demonstrate the potential long-term savings associated with refinancing, emphasizing the importance of considering this factor when making a decision. The difference between the two lines at year 10 would be prominently displayed, showcasing the total amount saved through refinancing.

Last Word

Refinancing your student loans with Sallie Mae, or any lender, requires careful consideration of your individual financial situation and long-term goals. By weighing the potential benefits of lower interest rates and shorter repayment terms against the risks of losing federal loan protections, you can make a decision that best suits your needs. Remember to thoroughly compare offers from multiple lenders before committing to a refinancing plan.

FAQ Compilation

What credit score is needed to refinance with Sallie Mae?

Sallie Mae’s minimum credit score requirement varies, but generally, a good to excellent credit score (typically 660 or higher) significantly improves your chances of approval and securing a favorable interest rate.

Can I refinance both federal and private student loans with Sallie Mae?

Yes, Sallie Mae typically allows refinancing of both federal and private student loans, but refinancing federal loans means losing potential federal benefits like income-driven repayment plans and forbearance options. Carefully consider this trade-off.

What are the potential fees associated with Sallie Mae refinancing?

Sallie Mae may charge origination fees or other processing fees. These fees vary and are usually disclosed during the application process. Be sure to review all fees before proceeding.

How long does the Sallie Mae refinancing application process take?

The application process can take several weeks, depending on factors such as your credit score, the completeness of your application, and Sallie Mae’s processing times. Be prepared for a thorough review of your financial information.