Navigating the world of student loans can feel overwhelming, especially when the terms “safe” and “secure” are thrown around. This guide aims to demystify the concept of a “safe student loan,” exploring what constitutes responsible borrowing and how to protect yourself from potential pitfalls. We’ll delve into the nuances of federal versus private loans, effective debt management strategies, and the impact of economic factors on your repayment journey.

Understanding the various interpretations of “safe” within the context of student loans is crucial. Factors such as manageable interest rates, flexible repayment options, and robust borrower protections all contribute to a loan’s perceived safety. Conversely, high interest rates, predatory lending practices, and lack of government oversight can significantly increase the risks involved. This guide will provide a comprehensive overview, equipping you with the knowledge to make informed decisions and navigate the complexities of student loan debt successfully.

Understanding “Safe Student Loan”

The term “safe student loan” is relative and depends heavily on the borrower’s perspective and financial situation. While no student loan is entirely without risk, certain features and loan types offer greater protection and predictability than others, making them comparatively “safer.” Understanding these nuances is crucial for making informed borrowing decisions.

The concept of a “safe” student loan encompasses several interpretations. For some, it means a loan with manageable repayment terms and predictable interest rates. Others prioritize loan forgiveness programs or other forms of government protection. Still others might focus on the lender’s reputation and financial stability. Ultimately, a “safe” loan is one that aligns with an individual’s financial capabilities and risk tolerance.

Features Contributing to Student Loan Safety

Several features can significantly enhance the safety of a student loan for the borrower. These features help mitigate potential financial strain and ensure a smoother repayment process. A focus on these features helps borrowers make informed choices about their financing options.

For instance, fixed interest rates offer predictability, shielding borrowers from fluctuating interest rates that can significantly increase the total cost of the loan over time. Favorable repayment plans, such as income-driven repayment options, allow borrowers to adjust their monthly payments based on their income, preventing overwhelming debt burdens. Deferment or forbearance options provide temporary relief from payments during periods of financial hardship, such as unemployment. Finally, robust borrower protections, like those offered by federal student loans, provide additional safeguards against unfair lending practices.

Risks Associated with Student Loans

Despite the presence of safety features, student loans inherently carry risks. Understanding these risks is essential for responsible borrowing.

High interest rates can dramatically increase the total cost of borrowing, particularly with variable-rate loans. Defaulting on a loan can have severe consequences, including damage to credit scores, wage garnishment, and difficulty obtaining future credit. Unexpected life events, such as job loss or illness, can create repayment challenges, even with flexible repayment plans. Finally, borrowing more than necessary can lead to unnecessary debt and financial stress, impacting long-term financial goals. A thorough understanding of these risks allows for responsible borrowing and mitigation strategies.

Comparison of Federal and Private Student Loan Safety Features

Federal and private student loans differ significantly in their safety features, impacting the overall risk for borrowers.

Federal student loans generally offer greater borrower protections. These include income-driven repayment plans, loan forgiveness programs (under certain circumstances), and robust consumer protections against lender misconduct. Private student loans, on the other hand, typically lack these extensive safeguards. While they might offer competitive interest rates in some cases, they often come with less flexibility and fewer protections for borrowers facing financial hardship. A careful comparison of these features is crucial before selecting a loan type.

Borrower Protection Mechanisms

Student loan borrowers are afforded various protections under federal and, in some cases, state regulations. These mechanisms aim to prevent predatory lending practices and ensure borrowers understand their rights and responsibilities. The goal is to balance the need for accessible higher education financing with the responsibility of repayment.

Government regulations play a crucial role in safeguarding student loan borrowers. These regulations cover various aspects of the loan process, from the initial application and loan terms to repayment options and default management. They aim to ensure transparency and fair treatment throughout the loan lifecycle.

Government Regulations Protecting Student Loan Borrowers

Numerous federal laws and regulations exist to protect student loan borrowers. The Truth in Lending Act (TILA), for example, requires lenders to disclose all loan terms clearly and concisely, including interest rates, fees, and repayment schedules. The Fair Credit Reporting Act (FCRA) ensures accuracy in credit reports, preventing erroneous information from negatively impacting a borrower’s ability to secure a loan or obtain favorable terms. Furthermore, the Higher Education Act (HEA) establishes various consumer protection measures specific to federal student loans, including borrower rights and protections against abusive lending practices. These laws collectively create a framework to ensure borrowers are treated fairly and have access to accurate information.

The Role of Credit Bureaus and Credit Scores in Assessing Loan Risk

Credit bureaus, such as Equifax, Experian, and TransUnion, collect and maintain individuals’ credit information. This information is used to generate a credit score, a numerical representation of an individual’s creditworthiness. Lenders utilize credit scores to assess the risk associated with lending money. A higher credit score generally indicates a lower risk of default, leading to more favorable loan terms, such as lower interest rates. Conversely, a lower credit score may result in higher interest rates, stricter eligibility criteria, or even loan denial. The credit scoring system, while imperfect, provides a standardized method for lenders to evaluate risk, contributing to a more efficient and equitable loan market.

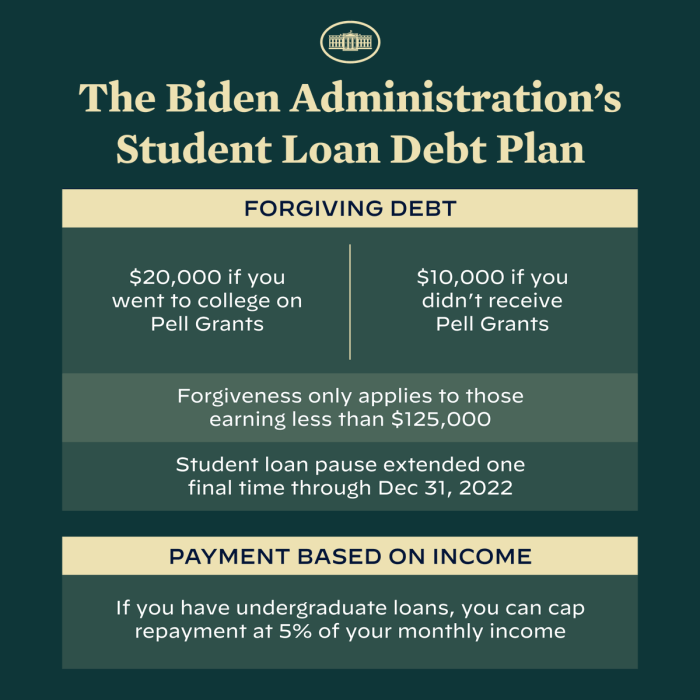

Implications of Loan Forgiveness Programs on Student Loan Safety

Loan forgiveness programs, while designed to alleviate the burden of student loan debt for certain borrowers, also have implications for the overall safety and stability of the student loan system. These programs can potentially increase the risk of default for other borrowers, as the cost of these programs is ultimately borne by taxpayers. Furthermore, the design and implementation of these programs can influence borrowing behavior, potentially leading to increased borrowing and higher overall debt levels. For example, the Public Service Loan Forgiveness (PSLF) program, while beneficial to qualifying borrowers, has faced challenges related to program complexity and eligibility requirements, resulting in lower-than-expected forgiveness rates. Careful consideration of the long-term financial implications is crucial for the sustainable management of loan forgiveness programs.

Hypothetical Scenario: Consequences of Student Loan Default

Imagine Sarah, a recent college graduate with $50,000 in student loan debt. Due to unexpected job loss and mounting medical bills, she falls behind on her loan payments. After repeated attempts to contact her lender, her account goes into default. This has several serious consequences: her credit score plummets, making it difficult to obtain credit for future needs like a car loan or mortgage. The government may garnish her wages, seizing a portion of her income to repay the debt. Her tax refunds could also be withheld. Furthermore, she may face legal action, including lawsuits and wage garnishment, potentially impacting her financial stability for years to come. This scenario highlights the significant risks associated with student loan default, underscoring the importance of responsible borrowing and proactive debt management.

Types of Safe Student Loans

Choosing the right student loan is crucial for your financial future. Understanding the differences between federal and private loans, and the various types within each category, is key to making informed decisions and minimizing potential risks. Federal student loans generally offer more robust borrower protections than private loans, making them a safer option for many students.

Federal Student Loan Characteristics

Federal student loans are considered safer due to several key characteristics. These loans are backed by the U.S. government, providing a safety net for borrowers in case of hardship. They offer various repayment plans, including income-driven repayment options, which can adjust payments based on your income and family size. Furthermore, federal loans often come with borrower protections like deferment and forbearance options, allowing temporary pauses in payments under specific circumstances. Finally, federal loan programs are subject to strict regulations designed to protect borrowers from predatory lending practices.

Types of Federal Student Loans

The following table summarizes the key differences between common types of federal student loans:

| Loan Type | Interest Rate | Repayment Options | Eligibility Requirements |

|---|---|---|---|

| Subsidized Direct Loan | Fixed rate set annually by the government. Interest does not accrue while the borrower is enrolled at least half-time or during grace periods. | Standard, graduated, extended, income-driven repayment plans. | Undergraduate students demonstrating financial need. |

| Unsubsidized Direct Loan | Fixed rate set annually by the government. Interest accrues from the time the loan is disbursed, regardless of enrollment status. | Standard, graduated, extended, income-driven repayment plans. | Undergraduate, graduate, and professional students. |

| Direct PLUS Loan (Graduate/Parent) | Fixed rate set annually by the government. Interest accrues from the time the loan is disbursed. | Standard, graduated, extended, income-driven repayment plans. | Graduate students and parents of dependent undergraduate students. Credit check required. |

Income-Driven Repayment Plans

Income-driven repayment (IDR) plans are designed to make federal student loan repayment more manageable. These plans calculate your monthly payment based on your income and family size. Several IDR plans exist, each with different eligibility requirements and payment calculations. The lower monthly payments offered by IDR plans can significantly improve loan safety by reducing the risk of default. However, it’s important to note that IDR plans typically extend the repayment period, potentially leading to higher overall interest payments. For example, the Revised Pay As You Earn (REPAYE) plan caps monthly payments at 10% of discretionary income, while the Income-Based Repayment (IBR) plan offers similar protections but with varying payment caps depending on loan origination date.

Private Student Loan Options

Private student loans are offered by banks, credit unions, and other financial institutions. While they can offer competitive interest rates, they generally lack the same borrower protections as federal loans.

| Loan Type | Interest Rate | Potential Benefits | Potential Risks |

|---|---|---|---|

| Variable Rate Private Loan | Fluctuates based on market conditions. | Potentially lower initial interest rate compared to fixed-rate loans. | Interest rate risk; payments can increase significantly if rates rise. Limited borrower protections. |

| Fixed Rate Private Loan | Remains constant throughout the loan term. | Predictable monthly payments. | Potentially higher initial interest rate compared to variable-rate loans. Limited borrower protections. |

| Private Loan with Co-Signer | May offer a lower interest rate or improved approval odds. | Improved chances of loan approval, potentially lower interest rate. | Co-signer remains responsible for the debt if the borrower defaults. |

Managing Student Loan Debt Safely

Successfully navigating student loan repayment requires proactive planning and a strategic approach. Understanding your repayment options, budgeting effectively, and protecting yourself from predatory practices are crucial for responsible debt management. This section will Artikel practical strategies to help you manage your student loans safely and efficiently.

Effective Budgeting Strategies for Student Loan Repayments

Creating a realistic budget is paramount to successful student loan repayment. This involves tracking your income and expenses meticulously to identify areas where you can cut back and allocate funds towards your loan payments. Consider using budgeting apps or spreadsheets to categorize your spending and monitor your progress. Prioritize essential expenses like housing, food, and transportation, then allocate as much as possible towards your student loan payments. Building a buffer for unexpected expenses is also crucial to avoid falling behind on payments. For example, a student earning $3000 a month might allocate $500 for rent, $400 for food, $200 for transportation, and $700 for loan repayments, leaving $1200 for other expenses and savings.

Improving Credit Scores to Qualify for Better Loan Terms

A strong credit score can significantly impact your ability to secure favorable loan terms, potentially lowering your interest rate and monthly payments. Improving your credit score involves consistently making on-time payments on all debts, including credit cards and student loans. Keeping your credit utilization low (ideally below 30%) is also important. Avoid applying for new credit frequently, as multiple inquiries can negatively impact your score. Regularly checking your credit report for errors and addressing them promptly is also recommended. For instance, consistently paying off your credit card balance in full each month and maintaining a low credit utilization ratio will improve your creditworthiness over time.

Student Loan Refinancing: Benefits and Drawbacks

Refinancing student loans involves replacing your existing loans with a new loan from a different lender, often with a lower interest rate. This can lead to lower monthly payments and potentially save you money over the life of the loan. However, refinancing might extend the repayment period, leading to higher total interest paid. It’s essential to carefully compare offers from multiple lenders and consider the long-term implications before refinancing. For example, a borrower with high-interest federal loans might benefit from refinancing to a lower interest private loan, but should weigh this against potential loss of federal loan benefits like income-driven repayment plans.

Avoiding Student Loan Scams and Predatory Lending Practices

Be wary of unsolicited offers promising unrealistic loan terms or quick solutions to your debt. Legitimate lenders will never ask for upfront fees or require you to share your personal information before verifying your identity. Research lenders thoroughly before applying for a loan and only work with reputable institutions. Familiarize yourself with the warning signs of predatory lending practices, such as high interest rates, hidden fees, and aggressive sales tactics. For example, avoid lenders who pressure you into signing a loan agreement without thoroughly reviewing the terms and conditions. Always seek independent financial advice before making any major financial decisions.

The Impact of Economic Factors

Economic fluctuations significantly impact student loan borrowers, affecting their ability to repay loans and influencing the overall safety and affordability of higher education. Understanding these economic forces is crucial for both borrowers and lenders to navigate the complexities of student loan debt effectively.

Economic downturns, such as recessions, often lead to increased unemployment and reduced earning potential. This directly affects borrowers’ ability to make timely student loan payments. Job losses, salary reductions, and reduced opportunities for career advancement all contribute to financial strain, potentially leading to loan default. Furthermore, during economic downturns, government support programs for struggling borrowers may be strained, limiting the availability of assistance.

Interest Rates and Student Loan Affordability

Interest rates play a pivotal role in determining the cost and overall safety of student loans. Higher interest rates increase the total amount borrowers must repay, making loans less affordable. Conversely, lower interest rates reduce the total cost, improving affordability and making repayment more manageable. For example, a borrower with a $50,000 loan at a 5% interest rate will pay significantly more over the life of the loan compared to a borrower with the same loan amount at a 3% interest rate. Fluctuations in interest rates, therefore, directly impact the long-term financial health of borrowers. Government intervention, through subsidized loans or interest rate caps, can mitigate some of these risks, providing a degree of safety to borrowers.

Inflation’s Impact on Student Loan Debt

Inflation erodes the purchasing power of money over time. While student loan debt remains fixed in nominal terms, its real value decreases as inflation rises. This means that the same amount of debt represents a smaller share of a borrower’s income in the future, particularly if wages also rise with inflation. However, if inflation outpaces wage growth, the real burden of the debt increases, making repayment more challenging. For instance, a $20,000 loan might seem manageable today, but its real value could decrease if inflation increases significantly over the next decade, potentially making repayment easier. Conversely, if wages remain stagnant while inflation rises, the same $20,000 loan will represent a larger portion of the borrower’s income, potentially leading to financial hardship.

Key Legislative Changes Affecting Student Loan Safety

Understanding the timeline of legislative changes impacting student loan safety provides valuable context for current policies.

| Year | Legislation/Event | Impact on Student Loan Safety |

|---|---|---|

| 1965 | Higher Education Act | Established federal student loan programs, providing a foundation for government involvement in student financing. |

| 2005 | Creation of the Direct Loan Program | Simplified the loan process and reduced reliance on private lenders. |

| 2007-2008 | Financial Crisis | Highlighted the vulnerability of borrowers during economic downturns and spurred calls for greater borrower protections. |

| 2010 | Health Care and Education Reconciliation Act | Made several changes to student loan programs, including adjustments to interest rates and repayment plans. |

| 2020-Present | COVID-19 Pandemic Emergency Relief | Implemented temporary payment pauses and interest rate reductions, providing significant relief to borrowers. |

Future of Safe Student Loans

The landscape of student loan financing is constantly evolving, influenced by shifting economic conditions, technological advancements, and evolving policy priorities. Understanding these changes is crucial for both prospective borrowers and policymakers aiming to create a more equitable and sustainable system. This section explores potential policy adjustments, emerging trends, and the long-term implications of various repayment strategies.

Potential Policy Changes to Enhance Student Loan Safety and Accessibility

Several policy changes could significantly improve the safety and accessibility of student loans. Income-driven repayment (IDR) plans, for instance, could be made more generous and streamlined, ensuring that monthly payments are truly affordable for borrowers across various income levels. Increased transparency in loan terms and interest rates would empower borrowers to make more informed choices. Furthermore, expanding loan forgiveness programs targeted at specific professions or those with significant student loan burdens could alleviate long-term debt stress. Finally, strengthening borrower protections against predatory lending practices is paramount to safeguarding borrowers from unfair or exploitative loan terms. For example, stricter regulations on private student loans could prevent high-interest rates and misleading marketing tactics.

Emerging Trends in Student Loan Financing and Their Implications for Borrowers

The rise of income-share agreements (ISAs) represents a significant emerging trend. ISAs offer an alternative to traditional loans, where borrowers agree to pay a percentage of their future income for a set period. While potentially beneficial for some, ISAs also carry risks, including the potential for prolonged repayment periods if income expectations aren’t met. Another trend is the increasing use of technology in student loan management, including mobile apps that facilitate repayment tracking and communication with lenders. This can enhance borrower convenience and potentially improve repayment rates, but also raises concerns about data security and potential biases embedded in algorithms used for credit scoring and loan approvals. Finally, the growing awareness of the student loan debt crisis is leading to increased advocacy for policy changes and greater consumer protection.

Visual Representation of Long-Term Effects of Student Loan Repayment Strategies

Imagine a graph with time on the x-axis and total debt on the y-axis. Three lines represent different repayment strategies: (1) Standard Repayment: This line shows a relatively steep decline in debt, representing consistent, higher payments over a shorter timeframe. (2) Income-Driven Repayment: This line shows a more gradual decline, reflecting lower monthly payments adjusted to income, potentially extending the repayment period. (3) Deferment/Forbearance: This line initially shows a plateau or even a slight increase as interest accrues during periods of non-payment, followed by a sharper decline once payments resume. The graph illustrates that while income-driven repayment might extend the repayment period, it minimizes the financial burden in the short term, potentially preventing default. Conversely, deferment/forbearance can lead to significantly higher overall debt due to accumulated interest.

Resources for Informed Decision-Making About Student Loans

Making informed decisions about student loans requires access to reliable information and guidance. Several resources are available to help students and borrowers navigate this complex process. The Federal Student Aid website (studentaid.gov) provides comprehensive information on federal student loan programs, repayment options, and borrower rights. Non-profit organizations like the National Consumer Law Center offer guidance on avoiding predatory lending practices and managing student loan debt. Finally, many colleges and universities provide financial aid offices that can assist students with understanding their loan options and developing a repayment plan. Utilizing these resources can significantly improve financial literacy and empower individuals to make responsible borrowing decisions.

Epilogue

Securing a safe student loan requires careful planning, diligent research, and a proactive approach to debt management. By understanding the different loan types, available protections, and potential risks, you can significantly improve your chances of successfully navigating the repayment process. Remember to prioritize responsible borrowing, utilize available resources, and stay informed about legislative changes impacting student loans. A well-informed approach to student loan financing can pave the way for a secure financial future.

FAQ Explained

What is the difference between subsidized and unsubsidized federal loans?

Subsidized loans don’t accrue interest while you’re in school, whereas unsubsidized loans do.

Can I consolidate my student loans?

Yes, loan consolidation combines multiple loans into one, potentially simplifying repayment. However, it might not always lower your interest rate.

What happens if I miss a student loan payment?

Missed payments can lead to late fees, damage your credit score, and eventually, default, which has serious financial consequences.

Are there resources available to help me manage my student loan debt?

Yes, many non-profit organizations and government agencies offer free counseling and resources to help manage student loan debt. The National Foundation for Credit Counseling (NFCC) is a good starting point.