Navigating the complex world of student government loans can feel overwhelming. This guide aims to demystify the process, providing a clear understanding of loan types, eligibility, repayment strategies, and available government assistance programs. We’ll explore both federal and private loan options, highlighting key differences in interest rates, repayment plans, and associated fees. Understanding these nuances is crucial for making informed decisions and managing your debt effectively post-graduation.

From the initial application process to long-term financial planning, we cover all aspects of student loan management. We also examine alternatives to loans, such as scholarships and grants, to help you find the most suitable financial path for your education. By the end of this guide, you’ll be equipped with the knowledge to confidently navigate the complexities of financing your education.

Types of Student Government Loans

Securing funding for higher education often involves navigating the complexities of student loans. Understanding the differences between federal and private loans is crucial for making informed financial decisions. This section will Artikel the key distinctions between these loan types, focusing on repayment plans, interest rates, and associated fees.

Federal and Private Student Loans: A Comparison

Federal student loans are offered by the U.S. government and generally come with more borrower protections than private loans. Private student loans, on the other hand, are provided by banks, credit unions, and other private lenders. The eligibility criteria, interest rates, and repayment options differ significantly between these two categories. Federal loans typically have lower interest rates and more flexible repayment plans, particularly for those facing financial hardship. However, private loans may be necessary for students who have exhausted their federal loan eligibility.

Repayment Plans for Federal and Private Student Loans

Federal student loans offer a variety of repayment plans designed to cater to different financial situations. These include standard repayment, graduated repayment (payments increase over time), extended repayment (longer repayment period), and income-driven repayment (payments are based on income and family size). Private loan repayment plans are typically less flexible and often consist of a standard fixed-payment plan over a set period. The specific options available depend on the lender and the loan terms.

Interest Rates and Fees Associated with Student Loans

Interest rates for federal student loans are set by the government and tend to be lower than those for private loans. The interest rate on a federal loan can vary depending on the loan type (e.g., subsidized vs. unsubsidized) and the prevailing market interest rates. Private loan interest rates are determined by the lender based on the borrower’s creditworthiness and other factors. They are typically variable or fixed, and usually higher than federal loan rates. Both federal and private loans may incur origination fees, which are charged at the time the loan is disbursed. Late payment fees can also apply to both types of loans.

Summary of Loan Types, Interest Rates, Repayment Options, and Fees

| Loan Type | Interest Rate | Repayment Options | Fees |

|---|---|---|---|

| Federal Subsidized Loan | Variable; set by the government; generally lower than private loans. | Standard, Graduated, Extended, Income-Driven | Origination fee; potential late payment fees. |

| Federal Unsubsidized Loan | Variable; set by the government; generally lower than private loans. | Standard, Graduated, Extended, Income-Driven | Origination fee; potential late payment fees. |

| Private Student Loan | Variable or fixed; determined by the lender; generally higher than federal loans. | Standard fixed-payment plan | Origination fee; potential late payment fees; prepayment penalties may apply. |

Eligibility and Application Process

Securing federal student loans involves understanding the eligibility requirements and navigating the application process. This section Artikels the criteria for eligibility, provides a step-by-step guide to applying, and details the necessary documentation. Understanding these aspects is crucial for a smooth and successful loan application.

Federal Student Loan Eligibility Criteria

Eligibility for federal student loans primarily hinges on factors such as U.S. citizenship or eligible non-citizen status, enrollment in an eligible educational program, demonstrated financial need (for some loan types), and maintaining satisfactory academic progress. Specific requirements may vary depending on the type of loan. For instance, a student might need to demonstrate financial need for a subsidized loan, whereas an unsubsidized loan doesn’t have this requirement. Furthermore, the student must be enrolled at least half-time in an eligible degree or certificate program at a participating institution. It is important to check with the institution and the lender to confirm eligibility requirements before applying.

Applying for Federal Student Loans: A Step-by-Step Guide

The application process for federal student loans begins with completing the Free Application for Federal Student Aid (FAFSA). This form gathers information about your financial situation and educational goals. After submitting the FAFSA, you’ll receive a Student Aid Report (SAR) summarizing your information and determining your eligibility for federal student aid. Based on your FAFSA information, your school will then notify you of your financial aid offer, which may include federal student loans. You’ll need to accept your loan offer and complete a Master Promissory Note (MPN) before the funds are disbursed. Finally, the funds will be disbursed directly to your educational institution to cover tuition, fees, and other eligible expenses.

Required Documentation for Loan Applications

The primary document required is the completed FAFSA form. This form requires detailed financial information, including your tax returns (or your parents’ tax returns, if you are a dependent student), income details, and assets. You may also need to provide documentation to verify your identity, citizenship or eligible non-citizen status, and enrollment in an eligible educational program. Additional documentation may be requested by the lender on a case-by-case basis. For example, a student may need to provide proof of enrollment or transcripts if there are discrepancies in their academic record.

Key Steps in the Federal Student Loan Application Process

The application process can be broken down into these key steps:

- Complete the FAFSA form accurately and submit it.

- Receive and review your Student Aid Report (SAR).

- Review your school’s financial aid offer, including loan amounts.

- Accept your loan offer and complete the Master Promissory Note (MPN).

- Funds are disbursed to your educational institution.

Managing Student Loan Debt

Successfully navigating student loan debt requires proactive planning and responsible financial management. Understanding repayment strategies, the potential consequences of default, and available options for managing your loans is crucial for long-term financial well-being. This section provides practical strategies to help you effectively manage your student loan debt.

Budgeting and Managing Student Loan Payments

Creating a realistic budget is paramount to successfully managing student loan payments. This involves tracking your income and expenses to identify areas where you can reduce spending and allocate funds towards your loan payments. Consider using budgeting apps or spreadsheets to monitor your finances effectively. Prioritize essential expenses like housing, food, and transportation, then allocate remaining funds to loan payments and savings. Explore different repayment plans offered by your loan servicer, such as graduated repayment (payments increase over time) or income-driven repayment (payments are based on your income). Automating your loan payments can prevent missed payments and late fees. Regularly review your budget and adjust as needed to ensure you stay on track.

Consequences of Defaulting on Student Loans

Defaulting on student loans has severe consequences. It can result in damaged credit scores, making it difficult to obtain loans, credit cards, or even rent an apartment in the future. Wage garnishment, where a portion of your paycheck is automatically deducted to pay your debt, is another possibility. The government may also seize your tax refunds or Social Security benefits. Furthermore, defaulting can impact your ability to secure employment in certain fields, and it can significantly hinder your long-term financial stability. For example, a default could lead to a significant decrease in your credit score, resulting in higher interest rates on future loans, costing you thousands of dollars over time.

Loan Consolidation and Refinancing Options

Loan consolidation combines multiple student loans into a single loan, often simplifying repayment by providing a single monthly payment. Refinancing involves replacing your existing loans with a new loan, potentially at a lower interest rate, reducing your monthly payments and the total amount you pay over the life of the loan. Both options can offer benefits, but it’s essential to carefully compare interest rates, fees, and repayment terms before making a decision. For example, refinancing could lower your monthly payment but might extend the repayment period, leading to a higher total interest paid. Consolidation might simplify your repayment process but might not always result in lower interest rates.

Sample Monthly Budget Incorporating Student Loan Payments

| Income | Amount |

|---|---|

| Net Monthly Salary | $3000 |

| Expenses | Amount |

| Housing | $1000 |

| Food | $400 |

| Transportation | $200 |

| Utilities | $150 |

| Student Loan Payment | $300 |

| Savings | $250 |

| Other Expenses | $700 |

This is a sample budget; your actual budget will depend on your individual circumstances. Remember to adjust this based on your income and expenses. Prioritizing loan payments within your budget is key to avoiding default and achieving long-term financial health.

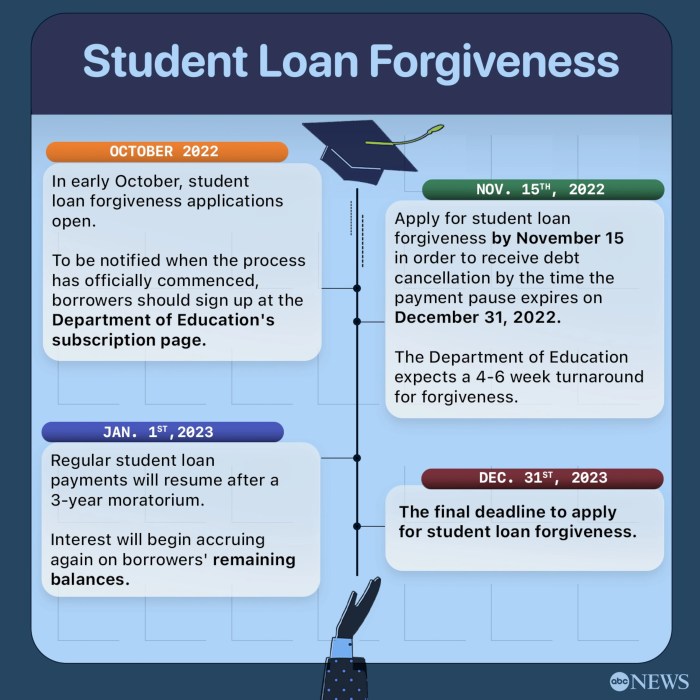

Government Loan Forgiveness Programs

Navigating the complexities of student loan repayment can be daunting, but several federal programs offer pathways to loan forgiveness. These programs, while offering potential relief, come with specific eligibility requirements and application processes. Understanding these details is crucial for borrowers hoping to utilize them.

Types of Federal Loan Forgiveness Programs

Several federal loan forgiveness programs exist, each designed for specific professions or circumstances. These programs aim to incentivize public service and address economic hardship. The availability and specifics of these programs can change, so it’s essential to check the official government websites for the most up-to-date information.

Public Service Loan Forgiveness (PSLF) Program

The Public Service Loan Forgiveness (PSLF) program forgives the remaining balance on your Direct Loans after you’ve made 120 qualifying monthly payments under a qualifying repayment plan while working full-time for a qualifying employer.

Eligibility for PSLF requires employment by a government organization or a 501(c)(3) non-profit organization. Your employment must be full-time, and your loans must be Direct Loans. Payments must be made under an income-driven repayment plan. The application process involves submitting an Employment Certification Form annually, and a final forgiveness application after 120 qualifying payments.

Teacher Loan Forgiveness Program

This program offers forgiveness of up to $17,500 on federal student loans for teachers who have taught full-time for at least five consecutive academic years in a low-income school or educational service agency. Eligibility hinges on teaching in a qualifying school and meeting the required years of service. The application process involves completing a specific form and providing documentation of employment and loan details.

Income-Driven Repayment (IDR) Plans and Forgiveness

Income-driven repayment plans, such as the Revised Pay As You Earn (REPAYE), Income-Based Repayment (IBR), and Income-Contingent Repayment (ICR) plans, are designed to make monthly payments more manageable based on income. After a specific number of years (typically 20-25), any remaining loan balance may be forgiven. Eligibility depends on income and loan type. The application process involves selecting an IDR plan and providing income documentation annually.

Comparison of Loan Forgiveness Programs

| Program | Eligibility Criteria | Forgiveness Amount | Application Process |

|---|---|---|---|

| Public Service Loan Forgiveness (PSLF) | 120 qualifying payments under an IDR plan while working full-time for a qualifying employer (government or 501(c)(3) non-profit) | Remaining loan balance | Annual Employment Certification Form, final forgiveness application after 120 payments |

| Teacher Loan Forgiveness | 5 consecutive years of full-time teaching at a low-income school or educational service agency | Up to $17,500 | Completion of specific form and documentation of employment and loan details |

| Income-Driven Repayment (IDR) Plans | Income and loan type; varies by plan | Remaining balance after 20-25 years (varies by plan) | Selection of IDR plan and annual income documentation |

The Impact of Student Loans on Higher Education

Student loans have fundamentally reshaped the landscape of higher education, impacting accessibility, affordability, and ultimately, the trajectory of students’ lives. While they provide crucial financial support enabling many to pursue higher education, their increasing prevalence and rising costs present significant challenges for both individuals and the broader educational system.

Student loans play a vital role in expanding access to higher education. For many, they represent the only feasible path to obtaining a college degree, bridging the gap between tuition costs and available financial resources. Without student loans, a significant portion of the population would be effectively barred from pursuing higher education, limiting opportunities for social mobility and economic advancement. This accessibility, however, comes at a cost, which we will explore in further detail.

The Influence of Rising Tuition Costs on Student Loan Debt

The escalating cost of tuition and fees has created a direct correlation with increasing student loan debt. As tuition continues its upward trend, exceeding the rate of inflation and wage growth, students are forced to borrow larger sums to cover their educational expenses. This phenomenon is particularly pronounced in the United States, where tuition costs have risen significantly over the past few decades, resulting in a dramatic increase in student loan debt levels. For instance, the average student loan debt for the graduating class of 2023 is estimated to be significantly higher than that of previous years, illustrating the escalating problem. This rise necessitates a closer look at the financial implications for borrowers.

The Correlation Between Student Loan Debt and Post-Graduation Employment Prospects

The relationship between student loan debt and post-graduation employment prospects is complex and multifaceted. While a college degree often leads to higher earning potential over a lifetime, the burden of significant student loan debt can negatively impact immediate post-graduation employment choices. Graduates may be forced to accept lower-paying jobs to manage their debt repayments, or they may delay pursuing their desired career paths due to financial constraints. The pressure to secure high-paying jobs quickly can also lead to hasty career decisions that may not be aligned with long-term career goals. This creates a ripple effect on job satisfaction and overall financial well-being.

The Long-Term Financial Implications of Student Loan Debt

Student loan debt can significantly impact long-term financial planning. The substantial monthly payments can restrict access to other financial opportunities, such as homeownership, starting a family, and investing for retirement. High levels of debt can also affect credit scores, making it more challenging to secure loans for major purchases or investments in the future. For example, a young professional burdened with significant student loan debt might delay buying a home, impacting their ability to build wealth through home equity. Similarly, the need to prioritize debt repayment could limit contributions to retirement savings, potentially compromising long-term financial security.

Alternatives to Student Loans

Securing higher education shouldn’t solely rely on student loans. Numerous alternatives exist, offering pathways to fund your studies without accumulating significant debt. Exploring these options carefully can significantly impact your financial future. Consider the following avenues to lessen or eliminate your reliance on loans.

Scholarships and Grants

Scholarships and grants represent a significant source of non-repayable funding for higher education. These awards are often based on merit, academic achievement, or demonstrated financial need. Numerous organizations, including universities, private foundations, and corporations, offer scholarships. Grants, typically awarded based on financial need, are provided by government agencies and private institutions. Effective scholarship and grant searching involves researching opportunities specific to your field of study, academic record, and demographic background. Utilizing online scholarship databases and contacting your university’s financial aid office are crucial steps in securing these valuable funds. For example, the Pell Grant program in the United States provides substantial financial aid to undergraduate students from low-income families. Many private scholarships, such as those offered by the Gates Millennium Scholars program, target students with exceptional academic potential and financial need.

Working While Studying

Working while studying presents both advantages and disadvantages. On the one hand, it provides immediate income to cover educational expenses, reducing reliance on loans. Part-time employment can also offer valuable work experience and enhance your resume. However, balancing work and studies requires strong time management skills and can potentially impact academic performance if not managed effectively. The number of hours worked should be carefully considered, ensuring that academic commitments remain the priority. Examples of successful work-study arrangements include students working in campus libraries, tutoring peers, or securing part-time jobs in their chosen field. The key is to find a balance that supports your financial needs without compromising your academic goals.

Using Savings or Family Contributions

Utilizing personal savings or family contributions offers a straightforward way to fund education. This approach eliminates the need for loans and avoids the burden of future debt repayment. However, the availability of such funds varies greatly among individuals and families. Families might contribute through direct payments towards tuition or living expenses, while students might use savings accumulated from previous employment or other sources. Careful budgeting and financial planning are essential to determine the feasibility of this option. For example, a student who has diligently saved a portion of their earnings over several years might be able to cover a significant portion of their tuition costs. Similarly, families with strong financial stability may be able to contribute substantially to their children’s education.

Summary of Alternatives

- Scholarships and Grants: Non-repayable funding based on merit or need, often requiring applications and meeting specific criteria. Examples include Pell Grants and private scholarships.

- Working While Studying: Earning income to offset educational costs, but requires effective time management to balance work and studies. Examples include campus jobs or part-time positions.

- Using Savings or Family Contributions: Utilizing personal savings or family support to fund education, eliminating loan dependence. This requires prior financial planning and savings.

Understanding Loan Terms and Conditions

Navigating the world of student loans requires a thorough understanding of the terms and conditions associated with them. Failure to grasp these details can lead to unexpected costs and financial difficulties down the line. This section clarifies key aspects of loan agreements, empowering you to make informed decisions about your borrowing.

Subsidized vs. Unsubsidized Loans

Subsidized and unsubsidized loans are two primary types of federal student loans. The key difference lies in interest accrual. With subsidized loans, the government pays the interest while you’re in school at least half-time, during grace periods, and during periods of deferment. Unsubsidized loans, however, accrue interest from the moment the loan is disbursed, regardless of your enrollment status. This means that with unsubsidized loans, you’ll owe more than the original loan amount upon graduation. Choosing between these loan types depends on your financial situation and ability to manage accumulating interest.

Loan Deferment and Forbearance

Loan deferment and forbearance are options that allow temporary pauses in loan repayment. Deferment postpones payments and, for subsidized loans, may also suspend interest accrual. Forbearance, on the other hand, typically involves temporarily reducing or suspending payments, but interest usually continues to accrue during this period. Both options are available under specific circumstances, such as unemployment or financial hardship, but they are not always guaranteed and should be explored carefully. It is important to note that deferment and forbearance can impact your credit score and extend the overall repayment period, leading to higher total interest paid.

Interest Capitalization

Interest capitalization is the process of adding accumulated interest to the principal loan balance. This increases the total amount you owe. It typically occurs at the end of a deferment or forbearance period or when you switch from in-school status to repayment. The impact of interest capitalization can be significant, especially over longer repayment periods. For example, if you have $10,000 in unsubsidized loan debt and accumulate $1,000 in interest during a deferment period, capitalization would increase your principal balance to $11,000, meaning you’ll be paying interest on that larger amount during repayment. Understanding how and when interest capitalization occurs is crucial for accurate repayment planning.

Student Loan Lifecycle

The student loan lifecycle can be visualized as a series of distinct stages. First is the Application and Disbursement phase, where you apply for loans, are approved, and receive the funds. Next is the In-School/Grace Period stage, where you use the funds for education and a grace period follows graduation before repayment begins. Then comes the Repayment phase, where you make regular payments according to your repayment plan. Finally, the Loan Completion stage signifies the full repayment of the loan or potentially loan forgiveness. Each stage has its own unique characteristics and implications for your financial situation. A visual representation would show these stages as interconnected boxes, with arrows illustrating the progression from one phase to the next, highlighting key events and decisions at each point. The overall visual would emphasize the linear progression of the loan from disbursement to completion, illustrating the key differences in the stages.

Final Summary

Securing a higher education is a significant investment, and understanding the intricacies of student government loans is paramount to success. This guide has provided a comprehensive overview of the various loan types, application procedures, repayment options, and available government assistance programs. By carefully considering the information presented, you can make informed decisions about financing your education and effectively manage your student loan debt, paving the way for a financially secure future.

Essential Questionnaire

What is the difference between subsidized and unsubsidized loans?

Subsidized loans don’t accrue interest while you’re in school, grace periods, or deferment. Unsubsidized loans accrue interest throughout your entire loan term.

What happens if I default on my student loans?

Defaulting can lead to wage garnishment, tax refund offset, and damage to your credit score, making it difficult to obtain loans or credit in the future.

Can I refinance my student loans?

Yes, refinancing can potentially lower your interest rate and monthly payments, but it may involve losing government benefits.

What are some strategies for budgeting with student loan payments?

Create a detailed monthly budget, track your expenses, prioritize loan payments, explore income-driven repayment plans, and consider additional income streams.