Navigating the complex world of student loans can feel overwhelming. Understanding the different types of lenders, loan programs, and repayment options is crucial for making informed decisions about financing your education. This guide provides a comprehensive overview of student loan companies, helping you compare options and choose the best path for your financial future. We’ll explore both federal and private loan programs, highlighting key differences in interest rates, repayment terms, and eligibility requirements.

From understanding the nuances of subsidized and unsubsidized loans to comparing the offerings of various private lenders, we aim to demystify the process and empower you to make confident choices. We’ll also delve into practical strategies for managing your student loan debt effectively, ensuring a smoother journey towards financial independence.

Types of Student Loan Companies

Navigating the world of student loans can feel overwhelming, especially with the variety of lenders available. Understanding the differences between federal and private lenders is crucial for making informed borrowing decisions. This section will Artikel the key distinctions between these lender types, focusing on their loan offerings, interest rates, repayment options, and loan forgiveness programs.

Federal and Private Student Loan Lenders

The primary distinction lies between federal and private student loans. Federal loans are offered by the U.S. government, while private loans come from banks, credit unions, and other financial institutions. Federal loans generally offer more borrower protections and flexible repayment options compared to private loans.

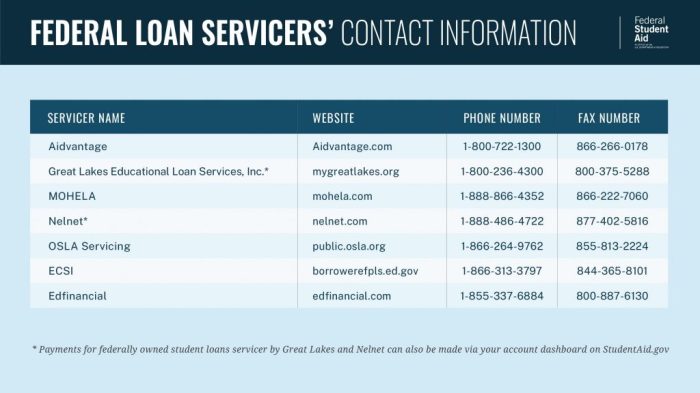

Federal Student Loan Programs

The federal government offers several loan programs, including subsidized and unsubsidized loans for undergraduates and graduate students, as well as PLUS loans for parents and graduate students. Subsidized loans do not accrue interest while the student is enrolled at least half-time, while unsubsidized loans accrue interest from the time of disbursement. PLUS loans typically have higher interest rates than subsidized and unsubsidized loans. Federal loans are subject to various income-driven repayment plans and potential loan forgiveness programs, depending on the borrower’s profession and income.

Private Student Loan Programs

Private student loans are offered by a wide range of lenders, each with its own eligibility criteria, interest rates, and repayment terms. These loans typically require a creditworthy co-signer, especially for students with limited or no credit history. Interest rates on private loans are generally variable and can fluctuate based on market conditions. Repayment options are usually less flexible than those offered for federal loans, and loan forgiveness programs are generally not available. The terms and conditions vary significantly between lenders, so careful comparison shopping is essential.

Comparison of Lender Types, Loan Types, Interest Rates, and Repayment Options

The following table provides an illustrative comparison, and actual rates and terms will vary depending on the lender and the borrower’s creditworthiness.

| Lender Type | Loan Type | Interest Rate Range (Illustrative) | Repayment Options |

|---|---|---|---|

| Federal | Subsidized Stafford Loan | Variable, based on current market rates (e.g., 4-7%) | Standard, graduated, income-driven repayment plans, deferment, forbearance |

| Federal | Unsubsidized Stafford Loan | Variable, based on current market rates (e.g., 4-7%) | Standard, graduated, income-driven repayment plans, deferment, forbearance |

| Federal | PLUS Loan | Variable, generally higher than Stafford loans (e.g., 7-10%) | Standard, graduated, extended repayment plans |

| Private | Undergraduate Loan | Variable, based on creditworthiness (e.g., 6-15%) | Standard, fixed-term repayment |

| Private | Graduate Loan | Variable, based on creditworthiness (e.g., 7-18%) | Standard, fixed-term repayment |

Federal Student Loan Programs

Federal student loan programs offer financial assistance to students pursuing higher education. These programs are administered by the U.S. Department of Education and offer various loan types with differing eligibility requirements and repayment terms. Understanding these differences is crucial for students to choose the most suitable option for their financial needs.

Direct Subsidized Loans

Direct Subsidized Loans are need-based loans offered to undergraduate students demonstrating financial need. The government pays the interest on these loans while the student is enrolled at least half-time, during grace periods, and during periods of deferment. This means borrowers don’t accrue interest during these periods, potentially saving them money in the long run.

- Eligibility: Demonstrated financial need as determined by the Free Application for Federal Student Aid (FAFSA).

- Interest: Subsidized during periods of enrollment, grace, and deferment.

- Loan Limits: Vary depending on the student’s year in school and the cost of attendance.

Direct Unsubsidized Loans

Unlike subsidized loans, Direct Unsubsidized Loans are not need-based. They are available to undergraduate, graduate, and professional students. Interest accrues from the time the loan is disbursed, regardless of the borrower’s enrollment status. This means borrowers will owe more than the original loan amount upon repayment.

- Eligibility: Generally available to all students who meet the requirements for federal student aid, regardless of financial need.

- Interest: Accrues from disbursement, regardless of enrollment status.

- Loan Limits: Vary depending on the student’s year in school, enrollment status (half-time or more), and the cost of attendance.

Direct PLUS Loans

Direct PLUS Loans are available to parents of dependent undergraduate students and to graduate or professional students. These loans are credit-based, meaning the borrower must pass a credit check. The interest rate is generally higher than subsidized and unsubsidized loans.

- Eligibility: Credit check required. Parents must demonstrate creditworthiness; graduate/professional students must meet basic eligibility requirements for federal student aid.

- Interest: Accrues from disbursement, regardless of enrollment status.

- Loan Limits: The cost of attendance minus other financial aid received.

Private Student Loan Providers

Private student loans can be a valuable supplement to federal loans, or a necessary option for students who don’t qualify for federal aid. However, it’s crucial to understand that private loans typically come with higher interest rates and less flexible repayment options than federal loans. Choosing the right private lender requires careful consideration of various factors, including interest rates, fees, and repayment terms.

Private student loan providers are financial institutions, such as banks and credit unions, that offer loans directly to students and their families to finance higher education expenses. Unlike federal student loans, which are backed by the government, private loans are subject to the lending institution’s specific terms and conditions. This means that interest rates, fees, and repayment options can vary significantly between lenders.

Prominent Private Student Loan Companies

Several major financial institutions offer private student loans. These lenders often compete for borrowers by offering various loan features and terms. It’s important to compare offers from multiple lenders before making a decision.

- Sallie Mae: A well-known provider offering a range of student loan products.

- Discover: Offers student loans with competitive interest rates and flexible repayment options.

- Citizens Bank: Provides private student loans with various features tailored to different student needs.

- PNC Bank: Another major bank offering student loan options.

- Wells Fargo: A large financial institution that provides private student loans.

Comparison of Loan Terms and Conditions

A direct comparison of loan terms across different private lenders is essential before selecting a loan. Key factors to consider include interest rates, fees, and repayment options. These aspects significantly influence the overall cost and repayment burden of the loan.

The following table compares the approximate interest rates, fees, and repayment terms offered by three major private student loan companies. Note that these are illustrative examples and actual rates and terms may vary based on individual creditworthiness and the specific loan product chosen. Always check the lender’s website for the most up-to-date information.

| Feature | Sallie Mae (Example) | Discover (Example) | Citizens Bank (Example) |

|---|---|---|---|

| Interest Rate (Variable) | 6.5% – 12% | 6% – 11% | 7% – 13% |

| Interest Rate (Fixed) | 7% – 13% | 7% – 12% | 8% – 14% |

| Origination Fee | 0% – 4% | 0% – 2% | 0% – 3% |

| Repayment Terms | 5-20 years | 5-15 years | 5-10 years |

Factors to Consider When Choosing a Lender

Choosing the right student loan lender is a crucial decision that can significantly impact your financial future. Understanding the various factors involved and weighing their importance will help you secure the best possible loan terms and navigate the repayment process smoothly. This section will Artikel key considerations to guide you in your selection.

Credit Score and Co-signer Requirements for Private Loans

Private student loans, unlike federal loans, typically require a credit check. Lenders assess your creditworthiness to determine your eligibility and the interest rate they’ll offer. A higher credit score generally translates to lower interest rates and more favorable loan terms. If your credit history is limited or your score is low, you may need a co-signer—someone with good credit who agrees to share responsibility for the loan. The co-signer’s creditworthiness is considered alongside yours, potentially increasing your chances of approval and securing a better interest rate. However, remember that a co-signer assumes financial responsibility if you default on the loan.

Other Key Factors in Choosing a Student Loan Company

Beyond credit scores and co-signers, several other factors deserve careful consideration. These include customer service responsiveness, the presence and nature of any fees associated with the loan, and the flexibility offered in repayment options. Reliable customer service is essential, especially when dealing with complex financial matters. Expect prompt responses to inquiries and efficient resolution of any issues that may arise. Scrutinize loan fees carefully, as these can significantly increase the overall cost of borrowing. Fees may include origination fees, late payment fees, and prepayment penalties. Finally, explore repayment options such as graduated repayment plans, income-driven repayment plans (if available), and deferment or forbearance options, to ensure the loan aligns with your anticipated post-graduation financial situation.

Federal Loans versus Private Loans: Benefits and Drawbacks

Federal student loans and private student loans differ significantly in their benefits and drawbacks. Federal loans often offer more borrower protections, including income-driven repayment plans, deferment options, and loan forgiveness programs under certain circumstances. Interest rates on federal loans are generally fixed and tend to be lower than those on private loans. However, federal loans may have lower borrowing limits than private loans. Private loans, on the other hand, may offer higher borrowing limits and potentially more flexible repayment terms, but usually come with higher interest rates and fewer borrower protections. The choice between federal and private loans depends heavily on individual circumstances, including credit history, financial need, and the total cost of education. Carefully weigh the advantages and disadvantages of each before making a decision.

Repayment Options and Plans

Understanding your repayment options is crucial for effectively managing your student loans. Choosing the right plan depends on your individual financial circumstances and goals. Different plans offer varying monthly payment amounts and total repayment periods. This section Artikels the various repayment plans available for federal student loans and provides examples to illustrate how monthly payments are calculated.

Federal Student Loan Repayment Plans

Several repayment plans are available for federal student loans, each designed to cater to different financial situations. These plans offer flexibility in terms of monthly payment amounts and loan repayment timelines.

- Standard Repayment Plan: This is the default plan, requiring fixed monthly payments over a 10-year period. The monthly payment is calculated based on your loan balance and interest rate. For example, a $30,000 loan at a 5% interest rate would have an approximate monthly payment of $316. This is a simple calculation, and the exact amount will depend on the specific loan terms and interest capitalization.

- Graduated Repayment Plan: This plan starts with lower monthly payments that gradually increase every two years over a 10-year period. This can be helpful for borrowers expecting their income to rise over time. However, it ultimately results in a higher total interest paid compared to the Standard plan. The initial payment on a $30,000 loan at 5% might be significantly lower than $316, but the final payments would be higher.

- Extended Repayment Plan: This plan allows for longer repayment periods, up to 25 years, resulting in lower monthly payments. However, this also leads to significantly higher total interest paid over the life of the loan. The monthly payment on a $30,000 loan at 5% over 25 years would be substantially lower than the standard plan, but the total interest paid would be much greater.

Income-Driven Repayment Plans

Income-driven repayment (IDR) plans tie your monthly payment to your income and family size. These plans are designed to make student loan repayment more manageable, especially for borrowers with lower incomes. Several IDR plans exist, each with its own eligibility criteria and payment calculation method.

- Income-Based Repayment (IBR): Eligibility typically requires a demonstrated need for repayment assistance. Payments are calculated based on your discretionary income (income minus 150% of the poverty guideline for your family size) and loan balance. The repayment period is typically 20 or 25 years. The exact calculation is complex and involves several factors. A simplified example might show a significantly lower monthly payment than the standard plan for someone with a low income.

- Pay As You Earn (PAYE): Similar to IBR, PAYE bases payments on your discretionary income (income minus 150% of the poverty guideline) and loan balance. The repayment period is 20 years. The calculation, similar to IBR, is quite complex and depends on numerous factors.

- Revised Pay As You Earn (REPAYE): REPAYE also considers discretionary income (income minus 150% of the poverty guideline) and loan balance. However, it includes both undergraduate and graduate loans in the calculation. The repayment period is 20 years. Again, a precise calculation requires specific financial information.

- Income-Contingent Repayment (ICR): This plan considers your income, family size, and loan balance. The repayment period can be up to 25 years. The calculation formula differs slightly from other IDR plans and is best determined through official government resources.

Calculating Monthly Payments

Calculating the exact monthly payment for each plan requires using the loan amount, interest rate, and repayment period. There are online calculators available from the federal government and various student loan websites that can assist in this process. The formula itself is complex and involves several financial variables, making manual calculation difficult. However, it’s essential to remember that the total interest paid will vary greatly depending on the chosen repayment plan and the length of the repayment period. For instance, an extended repayment plan will result in a lower monthly payment but a much higher total interest cost compared to a standard repayment plan. Choosing the right plan requires carefully weighing the trade-offs between lower monthly payments and the total cost of the loan.

Understanding Loan Terms and Fees

Navigating the world of student loans requires a clear understanding of the terminology and associated costs. This section will clarify key loan terms and demonstrate how they impact the overall cost of borrowing, enabling you to make informed decisions.

Understanding these terms is crucial for responsible financial planning and avoiding unexpected expenses. Failure to grasp these concepts can lead to higher overall borrowing costs and difficulties in managing repayment.

Interest Rate

The interest rate is the percentage charged on the principal loan amount. It represents the cost of borrowing money. A higher interest rate means you’ll pay more in interest over the life of the loan. For example, a loan with a 5% interest rate will accrue less interest than a loan with a 7% interest rate, assuming all other factors remain constant. The interest rate is usually fixed or variable. A fixed interest rate remains constant throughout the loan term, while a variable interest rate can fluctuate based on market conditions. This variability introduces uncertainty into the total repayment amount.

Principal

The principal is the original amount of money borrowed. This is the amount you’re initially responsible for repaying, excluding interest. For instance, if you borrow $10,000 for your education, that $10,000 is your principal. As you make payments, the principal balance decreases. The principal is the foundation of your loan calculations.

Amortization

Amortization refers to the process of paying off a loan through regular payments. Each payment typically includes a portion of the principal and a portion of the interest. Early in the loan term, a larger portion of each payment goes toward interest, while later on, a larger portion goes towards principal. A standard amortization schedule shows the breakdown of principal and interest for each payment over the life of the loan. Understanding amortization allows you to see the progress of your loan repayment and track the balance reduction.

Loan Origination Fees

Loan origination fees are charges levied by the lender to cover the administrative costs of processing your loan application. These fees are typically a percentage of the loan amount and are added to the total amount you borrow. For example, a 1% origination fee on a $20,000 loan would be $200. This fee increases the overall cost of borrowing and should be factored into your decision-making process.

Impact of Interest Rates and Loan Terms on Total Cost

Different interest rates and loan terms significantly impact the total cost of borrowing. Consider two loans, both for $10,000: one with a 5% interest rate over 10 years and another with a 7% interest rate over 10 years. The loan with the higher interest rate will result in significantly higher total interest paid over the life of the loan, even though the principal remains the same. Similarly, a longer loan term (e.g., 15 years instead of 10 years) at the same interest rate will result in a higher total interest paid due to more interest accruing over the extended repayment period.

Illustrative Representation of Interest Rate Impact

Imagine two bar graphs representing total repayment amounts over time. Both graphs have the same initial principal loan amount represented by the initial bar height. The graph representing the lower interest rate shows a more gradual increase in the total repayment amount over time, with a smaller final bar representing the total amount repaid. In contrast, the graph representing the higher interest rate shows a steeper increase, resulting in a significantly taller final bar illustrating a much larger total repayment amount. This visual representation clearly demonstrates how even small differences in interest rates can drastically affect the overall cost of the loan.

Managing Student Loan Debt

Successfully navigating student loan repayment requires proactive planning and a comprehensive understanding of available resources. Effective management minimizes financial strain and promotes long-term financial well-being. This section Artikels strategies for responsible debt management, including budgeting, repayment planning, and utilizing available assistance programs.

Budgeting and Creating a Repayment Plan

Creating a realistic budget is the cornerstone of effective student loan management. This involves tracking all income and expenses to identify areas for potential savings. Once a clear picture of your financial situation emerges, you can develop a repayment plan that aligns with your budget. This might involve prioritizing high-interest loans first (avalanche method) or focusing on paying off the smallest loans first for a sense of accomplishment (snowball method). Consider using budgeting apps or spreadsheets to simplify the process and monitor progress. A well-structured repayment plan should detail the amount you’ll allocate to student loan payments each month, the repayment timeline, and any potential adjustments needed based on changing circumstances.

Loan Deferment and Forbearance Options

Borrowers facing temporary financial hardship may qualify for loan deferment or forbearance. Deferment temporarily suspends loan payments, often without accruing interest on subsidized federal loans. Forbearance allows for temporary reduced payments or a pause in payments, but interest usually continues to accrue. Eligibility criteria vary depending on the type of loan and the borrower’s circumstances. Documentation of financial hardship, such as job loss or medical expenses, is typically required. It’s crucial to understand that while deferment and forbearance provide temporary relief, they ultimately extend the repayment period and increase the total interest paid over the life of the loan. Therefore, these options should be considered carefully and only used when absolutely necessary.

Improving Credit Scores and Maintaining Financial Health

Maintaining a good credit score is vital during and after student loan repayment. On-time loan payments are a significant factor in credit score calculation. Consistent, timely payments demonstrate responsible financial behavior, positively impacting your creditworthiness. Additionally, regularly checking your credit report for errors and addressing any inaccuracies is crucial. Furthermore, managing other aspects of your financial health, such as keeping credit utilization low (the amount of credit used compared to the total available credit), contributes to a healthier credit profile. A strong credit score opens doors to better interest rates on future loans and other financial products, ultimately facilitating improved financial well-being.

Closing Summary

Securing funding for your education is a significant step, and understanding the landscape of student loan companies is paramount. By carefully considering the factors Artikeld in this guide – including lender type, loan terms, repayment options, and your individual financial circumstances – you can make informed decisions that align with your long-term financial goals. Remember to explore all available resources and seek professional advice when needed to navigate this important process successfully.

Query Resolution

What is the difference between a subsidized and unsubsidized federal student loan?

With subsidized loans, the government pays the interest while you’re in school (under certain conditions). Unsubsidized loans accrue interest from the time the loan is disbursed.

Can I refinance my student loans?

Yes, you can refinance both federal and private student loans, potentially lowering your interest rate or simplifying your payments. However, refinancing federal loans means losing federal protections.

What happens if I can’t make my student loan payments?

Contact your lender immediately. They may offer options like deferment, forbearance, or income-driven repayment plans to help you manage your debt.

How can I improve my credit score to qualify for better loan terms?

Pay bills on time, keep credit utilization low, and maintain a diverse credit history. Monitor your credit report regularly for errors.