Navigating the complexities of student loan financing can feel overwhelming, especially when confronted with the concept of maximum loan amounts. Understanding these limits is crucial for responsible borrowing and long-term financial well-being. This guide delves into the intricacies of federal and private student loan maximums, exploring factors that influence eligibility and the potential consequences of borrowing the maximum amount. We’ll equip you with the knowledge to make informed decisions about your educational funding.

From understanding the different loan programs and their respective limits based on your dependency status and educational level to exploring the impact of credit history and cost of attendance, we’ll provide a comprehensive overview. We will also examine the potential long-term financial implications of maximum borrowing and offer strategies for effective debt management. By the end, you’ll have a clearer picture of how to navigate the student loan landscape responsibly.

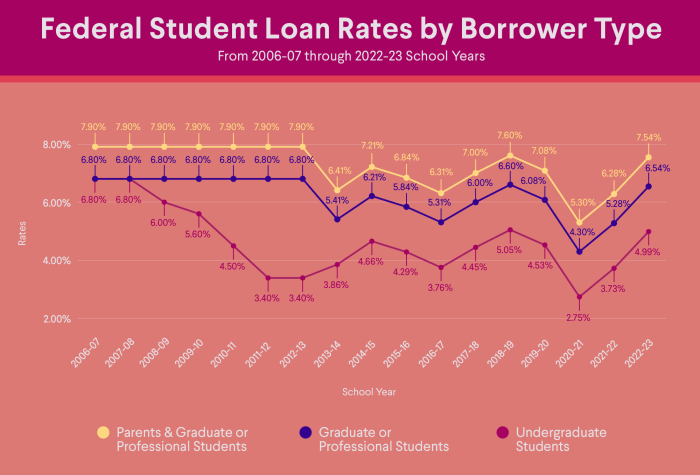

Federal Student Loan Limits

Understanding federal student loan limits is crucial for prospective students and their families in planning for higher education costs. These limits vary depending on several factors, including the student’s year in school, dependency status, and the type of loan program. This information will clarify the maximum amounts available under different scenarios.

Undergraduate Loan Limits

Federal student loan limits for undergraduates differ based on dependency status (dependent versus independent) and the type of loan. Dependent students generally have lower borrowing limits than independent students. The annual loan limits also increase slightly for students who are entering their second, third, and fourth years of undergraduate study.

Graduate and Professional Student Loan Limits

Graduate and professional students have access to different loan programs with higher borrowing limits than undergraduate programs. The specific limits depend on the program and the student’s enrollment status. Independent students generally have access to higher loan amounts. These higher limits reflect the typically increased costs associated with graduate and professional degree programs.

Dependency Status and Loan Limits

A student’s dependency status significantly impacts their eligibility for federal student aid, including loan limits. A dependent student is typically one who is claimed as a dependent on a parent’s tax return, while an independent student meets specific criteria indicating financial independence. Independent students usually qualify for higher loan amounts. This is because they are considered to have greater financial responsibility.

Loan Program Breakdown and Limits (2023-2024 Academic Year)

The following table Artikels the maximum loan amounts for different federal student loan programs for the 2023-2024 academic year. Note that these amounts are subject to change, so it’s important to consult the official Federal Student Aid website for the most up-to-date information.

| Loan Program | Dependency Status | Loan Type | Maximum Loan Amount |

|---|---|---|---|

| Direct Subsidized Loans | Dependent | Undergraduate | $3,500 (first year), $4,500 (second year), $5,500 (third/fourth year) |

| Direct Subsidized Loans | Independent | Undergraduate | $5,500 (first year), $6,500 (second year), $7,500 (third/fourth year) |

| Direct Unsubsidized Loans | Dependent | Undergraduate | $2,000 (first year), $2,000 (second year), $2,000 (third/fourth year) + Dependent Subsidized Loan Limit |

| Direct Unsubsidized Loans | Independent | Undergraduate | $2,000 (first year), $2,000 (second year), $2,000 (third/fourth year) + Independent Subsidized Loan Limit |

| Direct Unsubsidized Loans | Dependent/Independent | Graduate/Professional | $20,500 |

| Grad PLUS Loans | Dependent/Independent | Graduate/Professional | Cost of attendance minus other financial aid |

Factors Affecting Student Loan Maximums

Securing the maximum amount of federal student loan funding hinges on several key factors. Understanding these factors is crucial for students aiming to maximize their financial aid for higher education. This section details the influence of credit history, cost of attendance, enrollment status, and program of study on loan eligibility.

Credit History’s Impact on Loan Eligibility

While federal student loans typically don’t require a credit check for undergraduate students, a strong credit history can indirectly affect loan eligibility. A poor credit history might make it more difficult to obtain private student loans, which often supplement federal aid. Lenders assess creditworthiness to determine the risk associated with lending, and a history of missed payments or defaults can lead to higher interest rates or even loan denial. Conversely, a good credit history can potentially improve access to private loans with more favorable terms, effectively increasing the overall amount of available funding.

Cost of Attendance and Loan Eligibility

The cost of attendance (COA) at a given institution plays a significant role in determining the maximum loan amount a student can receive. The COA encompasses tuition, fees, room and board, books, and other necessary expenses. Federal loan programs typically set limits based on the student’s COA, ensuring the loan amount doesn’t exceed the actual educational expenses. For example, if a student’s COA is $25,000, the maximum loan amount might be capped at a certain percentage of this figure, say, $20,000, depending on the student’s year in school and dependency status. This prevents students from borrowing more than they need for their education.

Other Factors Influencing Maximum Loan Amounts

Several other factors influence the maximum loan amount a student can receive. Enrollment status (full-time versus part-time) directly affects eligibility. Full-time students generally qualify for higher loan amounts than part-time students because they are pursuing their degree at a faster pace. The program of study can also impact loan limits, although this is less common with federal loans. Some specialized programs might have different funding structures, potentially affecting the maximum loan amounts available. Finally, the student’s dependency status (dependent or independent) significantly impacts loan eligibility and maximum amounts, as independent students often qualify for higher loan limits.

Flowchart: Determining Maximum Loan Eligibility

The following flowchart illustrates the decision-making process for determining maximum student loan eligibility:

[Imagine a flowchart here. The flowchart would start with a box labeled “Student Applies for Federal Student Loans.” This would branch to boxes assessing: “Credit History (Indirectly Affects Private Loan Eligibility)”, “Cost of Attendance (Determines Maximum Loan Amount)”, “Enrollment Status (Full-time/Part-time)”, and “Dependency Status (Dependent/Independent)”. Each of these boxes would lead to a final box labeled “Maximum Loan Amount Determined”. Arrows would connect the boxes, indicating the flow of the decision-making process. The flowchart would visually represent how these factors interact to determine the final loan amount.]

Private Student Loan Maximums

Private student loans offer an alternative funding source for higher education, supplementing federal loans or covering costs not met by federal aid. However, unlike federal loans with established maximums based on factors like dependency status and year in school, private loan limits vary significantly between lenders and are determined on a case-by-case basis. Understanding these variations is crucial for prospective borrowers to make informed decisions.

Private lenders assess individual financial situations to determine the maximum loan amount they’re willing to provide. This contrasts with federal student loans, which have set maximums based on factors such as year in school and dependency status. The process is more individualized, often leading to a wider range of loan amounts available, but also potentially requiring more stringent eligibility criteria.

Factors Considered by Private Lenders When Setting Loan Limits

Several factors influence a private lender’s decision regarding loan limits. These include the borrower’s credit history (or the co-signer’s credit history, if one is required), income, debt-to-income ratio, the applicant’s educational background and the intended program of study. A strong credit history and a low debt-to-income ratio generally lead to higher loan limits and more favorable interest rates. The lender also considers the cost of attendance at the chosen institution to determine the overall need for funding and to ensure the loan amount is reasonable in relation to the educational expense. For example, a student attending a highly expensive private university may be eligible for a larger loan amount than a student attending a less expensive public institution, assuming all other financial factors are equal. Furthermore, the type of degree program can play a role; programs leading to higher-earning potential might justify higher loan amounts.

Private Student Loan Application Process and Required Information

Applying for a private student loan typically involves completing an online application form and providing supporting documentation. This documentation often includes proof of enrollment (acceptance letter, transcript), information about the cost of attendance (tuition, fees, living expenses), and personal financial information (income statements, tax returns, credit report). The lender will use this information to assess creditworthiness, determine the applicant’s need for funding, and set the loan limit. The lender will also verify the applicant’s identity and educational institution. Co-signers are frequently required, especially for students with limited or no credit history. The co-signer’s credit history and financial stability significantly impact the loan approval and the loan terms offered. Failure to provide complete and accurate information can delay or prevent loan approval.

Comparison of Private Student Loan Offers from Different Lenders

It is important to note that interest rates and repayment options are subject to change and depend on the individual’s creditworthiness and other factors. The following is a sample comparison and should not be considered exhaustive or a recommendation. Always check directly with the lender for the most up-to-date information.

- Lender A: Maximum loan amount may vary, but can reach up to $100,000; interest rates typically range from 6% to 12%; repayment options include standard, graduated, and extended repayment plans.

- Lender B: Maximum loan amount is typically capped at $75,000; interest rates generally range from 7% to 14%; repayment options may include fixed-rate and variable-rate loans with different repayment schedules.

- Lender C: Maximum loan amount can vary based on creditworthiness and may reach up to $50,000; interest rates typically range from 8% to 15%; repayment options may be limited compared to other lenders.

Consequences of Borrowing the Maximum

Borrowing the maximum amount in student loans can have significant long-term financial implications, impacting your ability to save, invest, and achieve other financial goals. While higher education is a valuable investment, understanding the potential drawbacks of maximal borrowing is crucial for responsible financial planning. This section explores the ramifications of maximum loan utilization, examining different repayment strategies and offering effective debt management techniques.

The most immediate consequence is the sheer size of the debt. A large student loan balance necessitates substantial monthly payments, potentially impacting your ability to save for a down payment on a house, invest in retirement, or even comfortably manage everyday expenses. This burden can extend for many years, significantly impacting your financial flexibility and overall quality of life. The longer it takes to repay the loan, the more interest you accrue, compounding the total cost of your education.

Impact of Different Repayment Plans on Total Interest Paid

Choosing the right repayment plan is crucial in minimizing the total interest paid. Standard repayment plans offer fixed monthly payments over a 10-year period, while income-driven repayment plans (IDR) adjust your monthly payment based on your income and family size. IDR plans typically extend the repayment period to 20 or 25 years, resulting in lower monthly payments but significantly higher total interest paid over the life of the loan.

For example, a $100,000 loan with a 6% interest rate would have a monthly payment of approximately $1,018.65 under the standard 10-year plan, resulting in a total interest payment of roughly $22,238. Under an IDR plan with a 20-year repayment period, the monthly payment might be significantly lower, but the total interest paid could easily exceed $50,000. This illustrates the trade-off between lower monthly payments and increased overall cost.

Strategies for Managing Student Loan Debt Effectively

Effective student loan debt management involves a multifaceted approach encompassing budgeting, prioritizing payments, and exploring potential repayment options. Creating a detailed budget allows you to track income and expenses, ensuring you can afford your monthly payments without compromising other essential needs. Prioritizing loan payments, perhaps by focusing on higher-interest loans first, can help minimize the total interest paid over time. Exploring options like refinancing or consolidation can also help streamline payments and potentially lower your interest rate.

Furthermore, maintaining a good credit score is crucial for securing favorable loan terms and accessing financial products in the future. Regularly monitoring your credit report and paying bills on time are essential steps in managing your credit responsibly. Finally, seeking professional financial advice can provide personalized guidance and support in navigating the complexities of student loan repayment.

Sample Repayment Schedule

The following table demonstrates the differences between standard and income-driven repayment plans for a hypothetical $50,000 loan at a 5% interest rate. These are simplified examples and actual repayment amounts may vary based on individual circumstances and loan terms.

| Year | Standard Repayment (10 years) Monthly Payment | Standard Repayment (10 years) Total Interest Paid (Cumulative) | Income-Driven Repayment (20 years) Monthly Payment (Example) | Income-Driven Repayment (20 years) Total Interest Paid (Cumulative) |

|---|---|---|---|---|

| 1 | $530 | $1,560 | $265 | $780 |

| 5 | $530 | $7,800 | $265 | $3,900 |

| 10 | $530 | $14,040 | $265 | $7,800 |

| 20 | – | $14,040 | $265 | $15,600 |

Resources for Understanding Loan Limits

Navigating the world of student loans can be daunting, especially when trying to understand the maximum amounts you can borrow. Fortunately, several reliable resources exist to help you find accurate information and make informed decisions about your borrowing. Understanding these resources and employing effective research strategies is crucial for responsible financial planning.

Reliable Sources for Student Loan Information

Understanding your options requires accessing accurate information from trusted sources. Federal government websites offer the most reliable data on federal student loan limits. Additionally, independent, non-profit organizations dedicated to student financial aid provide valuable guidance and resources.

Federal Government Websites

The official websites of the U.S. Department of Education and the Federal Student Aid (FSA) office are primary sources for information on federal student loan programs, eligibility criteria, and maximum loan amounts. These websites provide detailed information on different loan types (such as subsidized and unsubsidized loans), repayment plans, and the implications of borrowing the maximum amount. They also offer tools and calculators to help estimate your borrowing needs and project your future loan payments. These sites are regularly updated to reflect changes in federal student loan programs and policies.

Independent Non-profit Organizations

Several non-profit organizations dedicated to student financial aid provide unbiased information and guidance. These organizations often offer resources such as loan comparison tools, financial literacy workshops, and one-on-one counseling to help students make informed decisions about their student loan borrowing. Their websites typically contain articles, guides, and FAQs that address common questions and concerns about student loans. These organizations frequently partner with educational institutions and government agencies to ensure the accuracy and relevance of their information.

Researching and Comparing Loan Options

Once you’ve identified reliable sources of information, you can begin researching and comparing different loan options. This involves understanding the terms and conditions of each loan, including interest rates, repayment periods, and any fees associated with the loan.

Understanding Loan Terms and Conditions

Before accepting any student loan, it is imperative to thoroughly understand the loan terms and conditions. This includes the interest rate, which determines the cost of borrowing; the repayment period, which affects the monthly payment amount; and any fees, such as origination fees or late payment fees. A clear understanding of these terms allows you to make informed decisions and avoid unexpected costs or financial difficulties. Carefully reviewing the loan documents and asking questions to clarify any uncertainties is essential.

Managing Student Loan Debt

Managing student loan debt effectively requires planning and proactive strategies. Several resources are available to help students navigate this process.

Resources for Debt Management

The Federal Student Aid website offers tools and resources to help students create a repayment plan that fits their budget. They provide information on various repayment options, such as income-driven repayment plans, and explain the benefits and drawbacks of each. Additionally, many non-profit organizations offer free financial counseling services to help students develop a comprehensive debt management strategy. These services can include budgeting assistance, debt consolidation advice, and guidance on avoiding potential financial pitfalls. These resources emphasize the importance of proactive planning and responsible financial behavior to ensure successful loan repayment.

Last Recap

Successfully managing student loan debt requires proactive planning and a thorough understanding of the available options. By carefully considering the factors influencing loan eligibility, exploring various repayment plans, and utilizing available resources, you can navigate the complexities of student loan borrowing and build a strong financial foundation for your future. Remember that responsible borrowing and diligent planning are key to mitigating the long-term financial implications of student loan debt.

Top FAQs

What happens if I borrow the maximum amount and can’t repay?

Defaulting on student loans can have serious consequences, including damage to your credit score, wage garnishment, and difficulty obtaining future loans. Explore options like income-driven repayment plans or loan consolidation to avoid default.

Can I refinance my student loans to lower my interest rate?

Yes, refinancing can potentially lower your interest rate and monthly payments. However, carefully compare offers from different lenders and consider the terms and conditions before refinancing.

Are there any grants or scholarships I can apply for to reduce my loan burden?

Yes, many grants and scholarships are available to students based on merit, need, or specific criteria. Research and apply for these options to reduce your reliance on loans.

How do I choose between a standard repayment plan and an income-driven repayment plan?

Standard plans offer fixed payments over a set period, while income-driven plans adjust payments based on your income. Consider your current financial situation and long-term income projections when making your decision.