Navigating the complexities of student loan repayment while pursuing a fulfilling career in the nonprofit sector presents unique challenges. Many nonprofit employees find themselves grappling with substantial debt alongside often lower salaries compared to for-profit counterparts. This exploration delves into the various strategies and resources available to help nonprofit workers manage their student loans effectively, from understanding loan forgiveness programs to developing sound financial planning techniques.

This guide offers a comprehensive overview of federal and state loan forgiveness programs specifically designed for nonprofit employees, analyzing their eligibility requirements, application processes, and potential benefits. We’ll also examine income-driven repayment (IDR) plans and their impact on monthly payments, long-term repayment strategies, and the overall financial well-being of nonprofit professionals. Furthermore, we address the crucial role of financial planning, salary negotiation, and the influence of student loan debt on career choices within the nonprofit sector.

Student Loan Forgiveness Programs for Nonprofit Employees

Many nonprofit employees dedicate their careers to serving their communities, often facing significant financial challenges, including substantial student loan debt. Fortunately, several federal and state programs offer loan forgiveness opportunities specifically designed to incentivize and support these individuals. Understanding the eligibility requirements, application processes, and comparative advantages of these programs is crucial for maximizing financial well-being.

Eligibility Requirements for Federal and State Loan Forgiveness Programs

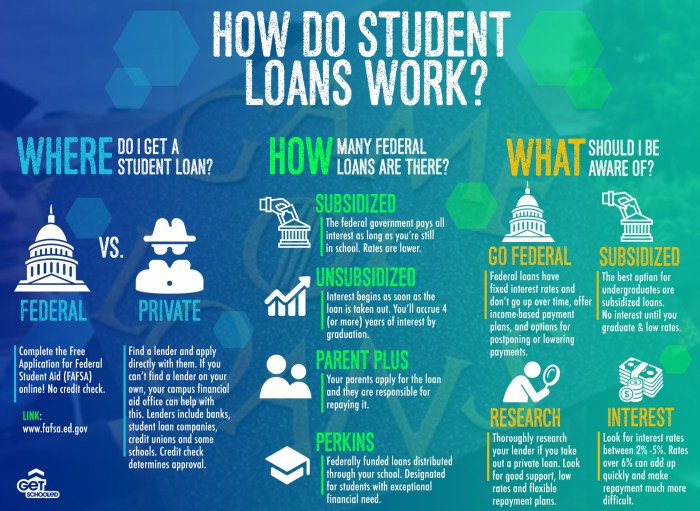

Eligibility for student loan forgiveness programs targeting nonprofit employees varies depending on the specific program. Federal programs generally require working full-time for a qualifying nonprofit organization for a specific period (typically 10 years under the Public Service Loan Forgiveness (PSLF) program). Qualifying nonprofits include those that are tax-exempt under section 501(c)(3) of the Internal Revenue Code, as well as certain other types of organizations. State programs may have additional or different requirements, such as residency restrictions or specific types of nonprofit employment. For example, some states might offer forgiveness programs specifically for teachers or healthcare professionals working in underserved areas. It’s essential to carefully review the specific requirements of each program to determine eligibility.

Comparative Analysis of Different Forgiveness Programs

Several federal and state programs offer loan forgiveness to nonprofit employees. The Public Service Loan Forgiveness (PSLF) program is a prominent federal program. It forgives the remaining balance of your Direct Loans after you’ve made 120 qualifying monthly payments under an income-driven repayment plan while working full-time for a qualifying employer. However, PSLF has stringent requirements and a complex application process, often leading to denials due to procedural errors. Some state programs may offer more streamlined processes or higher forgiveness amounts, but they typically cover a smaller pool of borrowers due to budgetary constraints. Advantages include significant debt reduction and financial relief, while disadvantages include lengthy repayment periods, strict eligibility criteria, and potential administrative hurdles.

Application Process and Required Documentation

The application process for each program varies. For the PSLF program, borrowers must consolidate their federal student loans into a Direct Consolidation Loan, submit an Employment Certification Form each year, and ensure they are enrolled in an income-driven repayment plan. Required documentation generally includes proof of employment (pay stubs, W-2 forms), tax returns, and loan servicing information. State programs may have different application forms and documentation requirements, often available through the respective state’s higher education agency or website. Timelines for processing applications can also vary significantly, ranging from several months to over a year.

Comparison of Key Features of Loan Forgiveness Programs

| Program | Eligibility Requirements | Forgiveness Amount | Application Process |

|---|---|---|---|

| Public Service Loan Forgiveness (PSLF) | 120 qualifying payments under an income-driven repayment plan while working full-time for a qualifying nonprofit | Remaining loan balance | Consolidation, annual employment certification, income-driven repayment plan |

| Teacher Loan Forgiveness Program | 5 years of full-time teaching in a low-income school | Up to $17,500 | Application through Federal Student Aid |

| State-Specific Programs (Example: [Insert a specific state program and its details here]) | [State-specific requirements, e.g., residency, type of nonprofit, years of service] | [Amount varies by state] | [Application process specific to the state] |

Income-Driven Repayment Plans and Nonprofit Employment

Income-driven repayment (IDR) plans offer a lifeline to many borrowers, particularly those working in the nonprofit sector, by adjusting monthly payments based on income and family size. These plans can significantly reduce the financial burden of student loan debt, making it more manageable while pursuing a career dedicated to public service. Understanding how these plans work and their long-term implications is crucial for nonprofit employees navigating student loan repayment.

IDR Plan Mechanics for Nonprofit Workers

IDR plans calculate monthly payments as a percentage of discretionary income, typically 10-20%, after accounting for basic living expenses. The specific percentage and income calculation method vary depending on the chosen plan (e.g., ICR, PAYE, REPAYE,IBR). For nonprofit employees, this often translates to lower monthly payments than standard repayment plans because salaries in the nonprofit sector are frequently lower than those in the for-profit sector. The lower income results in a smaller percentage being used to calculate the monthly payment. The government considers the borrower’s income and family size to determine the amount. This allows individuals to manage their debt while still contributing to their chosen field.

Examples of IDR Plan Payment Reductions

Consider two nonprofit employees: Sarah, a social worker earning $40,000 annually with $50,000 in student loan debt, and David, a teacher earning $60,000 annually with $75,000 in student loan debt. Under a standard repayment plan, both might face substantial monthly payments. However, under an IDR plan, Sarah’s monthly payment might be significantly lower, perhaps around $200-$300, while David’s might be in the $400-$500 range. These figures are estimates and would vary based on the specific IDR plan chosen, family size, and other factors. The key is the reduction in monthly payments compared to standard plans, making repayment more feasible.

Long-Term Implications of IDR Plans

Choosing an IDR plan has long-term implications. While monthly payments are lower, the repayment period extends significantly, potentially to 20 or 25 years. This results in a higher total interest paid over the life of the loan. However, many IDR plans include provisions for loan forgiveness after a certain number of qualifying payments (typically 120 or 240, depending on the plan and income), which can be a significant benefit, particularly for those in public service. For example, if Sarah qualifies for forgiveness after 240 payments under an IDR plan, a substantial portion, or even all, of her remaining debt could be forgiven. The trade-off between lower monthly payments and higher total interest paid should be carefully considered, weighing the immediate financial relief against the long-term cost.

Applying for and Managing an IDR Plan: A Flowchart

The process of applying for and managing an IDR plan can be visualized as follows:

[A textual description of a flowchart is provided below, as image creation is outside the scope of this response. The flowchart would visually represent the steps.]

Step 1: Determine Eligibility: Check eligibility requirements for each IDR plan based on income and loan type.

Step 2: Choose an IDR Plan: Select the plan that best suits individual financial circumstances.

Step 3: Complete the Application: Fill out the necessary forms and submit them to the loan servicer.

Step 4: Income Certification: Provide documentation to verify income annually.

Step 5: Monitor Payments: Track payments regularly and ensure they are accurately reflecting income.

Step 6: Re-certification: Re-certify income annually or as required by the plan.

Step 7: Forgiveness (if applicable): After making the required number of payments, apply for loan forgiveness.

Financial Planning Strategies for Nonprofit Employees with Student Loans

Working in the nonprofit sector is often driven by passion and a desire to make a difference, but it frequently comes with lower salaries compared to for-profit counterparts. This can make managing significant student loan debt a considerable challenge, especially when balancing other financial responsibilities. Effective financial planning is crucial for nonprofit employees to navigate these complexities and build a secure financial future.

Common Financial Challenges Faced by Nonprofit Employees with Student Loan Debt

Nonprofit employees with substantial student loan debt often face a unique set of financial hurdles. Lower salaries frequently mean less disposable income, making loan repayments a significant burden. The pressure to maintain a lifestyle while contributing to charitable causes can lead to overspending and difficulty saving. Furthermore, the lack of employer-sponsored benefits like robust retirement plans or student loan repayment assistance, common in the for-profit sector, further exacerbates the situation. This can create a sense of financial insecurity and limit opportunities for career advancement or personal financial growth. For instance, an individual might struggle to save for a down payment on a house or adequately fund their retirement account due to the significant monthly student loan payments.

Creating a Realistic Budget for Nonprofit Employees

Developing a realistic budget is the cornerstone of effective financial planning. This involves a step-by-step process. First, meticulously track all income and expenses for at least one month to gain a clear understanding of your current financial situation. Next, categorize expenses (housing, food, transportation, loan payments, etc.) and identify areas where spending can be reduced. Prioritize essential expenses, such as housing and food, followed by loan payments and then savings. Allocate funds for unexpected expenses by establishing an emergency fund. Finally, regularly review and adjust the budget as needed, accounting for any changes in income or expenses. For example, using budgeting apps or spreadsheets can significantly aid in this process, offering visual representations of income and expenses and facilitating easier tracking.

Managing Student Loan Payments Alongside Other Financial Responsibilities

Balancing student loan payments with other financial obligations like retirement savings and emergency funds requires a strategic approach. Prioritize high-interest debt first, focusing on aggressively paying down loans with the highest interest rates to minimize overall interest costs. Simultaneously, allocate a portion of your income towards retirement savings, even if it’s a small amount. Consider tax-advantaged retirement accounts like a 401(k) or Roth IRA to maximize savings. Building an emergency fund is equally crucial, aiming for 3-6 months’ worth of living expenses to cushion against unexpected events. A systematic approach, such as automating loan payments and savings contributions, can ensure consistent progress toward these financial goals. For instance, automatically transferring a set amount to a savings account each month simplifies the process and makes it less prone to being overlooked.

Resources and Tools for Effective Financial Management

Several resources and tools can assist nonprofit employees in effectively managing their finances.

- Budgeting Apps: Mint, YNAB (You Need A Budget), Personal Capital offer features like expense tracking, budgeting tools, and financial goal setting.

- Financial Counseling Services: Nonprofit credit counseling agencies provide free or low-cost financial guidance and debt management plans.

- Student Loan Repayment Calculators: These tools help estimate monthly payments under different repayment plans and explore potential savings.

- Online Financial Education Resources: Websites like the Consumer Financial Protection Bureau (CFPB) and Khan Academy offer valuable information on personal finance topics.

The Impact of Student Loan Debt on Nonprofit Career Choices

The significant burden of student loan debt can profoundly shape career decisions, particularly within the nonprofit sector. The lower average salaries often found in nonprofit work, when compared to for-profit industries, create a complex financial equation for graduates grappling with substantial loan repayments. This necessitates a careful examination of how this debt influences career paths, job satisfaction, and overall professional trajectory within the nonprofit world.

The weight of student loan repayments significantly impacts career choices within the nonprofit sector. Many recent graduates, burdened by considerable debt, may prioritize higher-paying jobs in for-profit sectors, even if their passion lies in nonprofit work. The financial pressure of loan repayments can outweigh the intrinsic rewards of a fulfilling but lower-paying nonprofit career. This often leads to a difficult choice between personal financial stability and professional fulfillment.

Salary Comparisons Across Sectors

A comparison of average salaries reveals a stark difference between the nonprofit and for-profit sectors. For example, a recent graduate with a degree in social work might find an entry-level position in a nonprofit organization paying significantly less than a similar role in the private sector, such as a corporate social responsibility department. This disparity in compensation directly affects the ability of individuals to repay their student loans effectively and timely. The longer repayment period needed due to lower salaries can also lead to increased overall interest payments, further exacerbating the financial strain. Consider a hypothetical case: two graduates with identical student loan debt, one working in a for-profit firm earning $60,000 annually and the other in a nonprofit earning $40,000. The for-profit employee would likely repay their loans much faster, experiencing less financial stress and more flexibility in their future financial decisions.

Effects on Career Advancement and Job Satisfaction

Student loan debt can significantly hinder career advancement within nonprofit organizations. The financial pressure might discourage individuals from pursuing further education or professional development opportunities that could enhance their career prospects, even if these opportunities are offered by their employer. Furthermore, the constant worry about loan repayments can negatively impact job satisfaction. The stress associated with managing debt can affect morale, productivity, and overall well-being, potentially leading to burnout and higher turnover rates within the nonprofit sector. For instance, a case study could be performed observing individuals who defer promotions due to the increase in salary not being sufficient to outweigh the increased tax burden and loan repayments.

Visual Representation of Student Loan Debt and Career Choices

Imagine a graph with two axes. The horizontal axis represents the level of student loan debt (low, moderate, high), while the vertical axis represents the likelihood of choosing a nonprofit career (high, moderate, low). The graph would show a negative correlation. As the level of student loan debt increases, the likelihood of choosing a nonprofit career decreases. The line representing this correlation would slope downwards, illustrating how a heavier debt burden makes a nonprofit career, with its typically lower salaries, less attractive compared to higher-paying alternatives in the for-profit sector. This visual representation clearly demonstrates the impact of financial pressures on career decisions.

Negotiating Salary and Benefits Considering Student Loan Debt

Negotiating salary and benefits as a nonprofit employee with significant student loan debt requires a strategic approach. Openly and honestly communicating your financial situation, while maintaining professionalism, can significantly impact the outcome of your negotiations. Remember that your goal is to secure a compensation package that allows you to manage your debt responsibly while also meeting your living expenses.

Effectively Communicating the Financial Impact of Student Loan Debt During Salary Negotiations

When discussing salary, frame your student loan debt not as a personal problem, but as a quantifiable financial factor impacting your overall needs. Instead of saying “I have a lot of student loan debt,” try, “My monthly student loan payments are approximately [Dollar Amount], and this significantly impacts my required salary to maintain a comfortable standard of living.” This provides a concrete number for the employer to consider. Research the average salary for similar positions in your area to justify your requested salary. Providing a detailed budget outlining essential expenses (housing, food, transportation, etc.) alongside your loan payments can further strengthen your position. This demonstrates your financial responsibility and preparedness.

Strategies for Negotiating Benefits to Alleviate Student Loan Repayment Burden

Many nonprofits offer benefits beyond salary that can significantly reduce the burden of student loan repayment. Negotiating these benefits can be just as crucial as negotiating salary itself.

Employers may be willing to negotiate contributions to a 401(k) plan or other retirement savings vehicles, thus enabling you to potentially save for the future while simultaneously alleviating the burden of loan payments. This can free up additional cash flow to direct toward your student loan debt. Another avenue to explore is the possibility of increased paid time off (PTO). Additional PTO can provide opportunities for part-time work to supplement income, or it can be used to take a short break to focus intensely on tackling your student loan debt. For instance, a summer off dedicated to intensive repayment could significantly reduce the overall loan principal. Finally, some employers offer tuition reimbursement or professional development stipends which could help you acquire additional skills or further your education, potentially leading to higher-earning opportunities in the future, easing your long-term debt burden.

Understanding the Total Compensation Package

It’s crucial to look beyond just the base salary. The total compensation package encompasses all forms of compensation, including health insurance, retirement contributions, paid time off, professional development opportunities, and other perks. A lower base salary coupled with a generous benefits package could prove more financially advantageous than a higher salary with limited benefits, particularly when considering the weight of student loan payments. Carefully evaluate the total value of the offered package and compare it to your financial needs, including loan repayment. Use a spreadsheet or budgeting tool to calculate the total value of the benefits and factor it into your decision-making process. For example, a comprehensive health insurance plan can save thousands of dollars annually compared to purchasing a plan independently.

Approaching Discussions About Student Loan Debt During the Interview Process

While it’s generally advisable to avoid discussing personal financial details early in the interview process, you can subtly weave in your financial priorities. During discussions about your career goals and motivations, you can mention your desire for a stable and financially secure position that allows you to manage your long-term financial goals effectively. This sets the stage for later conversations about salary and benefits. Remember, your focus should be on how your skills and experience will benefit the organization and how a fair compensation package allows you to contribute fully and effectively. Avoid explicitly mentioning your student loan debt during the initial interview unless directly prompted. The salary negotiation stage is the most appropriate time to discuss this specific aspect of your financial needs.

Ultimate Conclusion

Successfully managing student loan debt while working in the nonprofit sector requires proactive planning and a thorough understanding of available resources. By leveraging loan forgiveness programs, utilizing income-driven repayment plans, and implementing effective budgeting strategies, nonprofit employees can navigate their financial responsibilities and achieve long-term financial stability. Remember, seeking professional financial advice tailored to your specific circumstances can provide invaluable support and guidance throughout this journey. The commitment to public service should not be hindered by overwhelming debt; with careful planning and informed decision-making, a fulfilling career in the nonprofit sector is entirely achievable.

Question & Answer Hub

Can I consolidate my student loans to lower my monthly payments?

Consolidation can simplify repayment by combining multiple loans into one, but it might not always lower your monthly payment, depending on the interest rate of the consolidated loan.

What happens if I leave my nonprofit job before loan forgiveness is complete?

The requirements for loan forgiveness programs often include a minimum period of employment at a qualifying nonprofit. Leaving before meeting those requirements may mean you lose the forgiveness.

Are there any tax implications for student loan forgiveness?

In some cases, forgiven student loan debt may be considered taxable income. Consult a tax professional for personalized advice.

What if I’m struggling to make my student loan payments?

Contact your loan servicer immediately to explore options like deferment or forbearance. They can help you create a manageable repayment plan.