The landscape of student loan debt in the United States is constantly shifting, a complex interplay of government policy, economic realities, and individual financial burdens. Millions grapple with repayment, facing a range of plans, interest rates, and potential forgiveness programs. Understanding the current situation requires navigating the intricacies of federal programs, recent administrative actions, and the ongoing debate surrounding the long-term solutions to this pervasive issue. This exploration delves into the current state of student loan repayment, examining the impact on borrowers and the economy, and considering potential alternative solutions.

From the Biden administration’s ambitious forgiveness plan and its legal challenges to the broader economic implications of widespread debt relief, the discussion covers a spectrum of viewpoints and potential outcomes. We will analyze the social equity aspects, exploring how student loan debt disproportionately affects certain demographics and hinders social mobility. Ultimately, the goal is to provide a comprehensive overview of this critical issue, empowering readers with a clearer understanding of the challenges and potential paths forward.

Current Status of Student Loan Repayment

The current status of federal student loan repayment is complex, marked by periods of pause and resumption, shifting repayment plans, and ongoing policy debates. Understanding the various programs and their implications is crucial for borrowers navigating this landscape. The information below provides a snapshot of the current situation, but it’s essential to consult the official federal student aid website for the most up-to-date details.

Following a long period of pandemic-related payment pauses, federal student loan repayments resumed in the fall of 2023. This resumption affects millions of borrowers and has significant financial implications for individuals and the national economy. The specific details of repayment plans and interest rates are detailed below.

Federal Student Loan Repayment Plans

Several repayment plans are available to borrowers, each with its own set of terms and conditions. The choice of plan significantly impacts monthly payments and the total amount paid over the life of the loan. Selecting the appropriate plan requires careful consideration of individual financial circumstances.

- Standard Repayment Plan: This is the default plan, requiring fixed monthly payments over a 10-year period. It typically results in the lowest total interest paid but may lead to higher monthly payments.

- Graduated Repayment Plan: Payments start low and gradually increase over time. This option can be helpful in the early years after graduation when income is typically lower, but total interest paid is usually higher than with the standard plan.

- Extended Repayment Plan: This plan extends the repayment period to up to 25 years, resulting in lower monthly payments but significantly higher total interest paid.

- Income-Driven Repayment (IDR) Plans: These plans (such as ICR, PAYE, REPAYE, andIBR) base monthly payments on income and family size. Payments are typically lower than other plans, but repayment periods are often longer, leading to higher total interest paid. After a certain number of years, any remaining balance may be forgiven under specific circumstances.

Interest Rates and Accruing Interest

Interest rates for federal student loans vary depending on the loan type and the year the loan was disbursed. Interest accrues even during periods of forbearance or deferment, although the accruing interest may be capitalized (added to the principal) in some cases. Understanding these nuances is crucial for accurate financial planning.

| Loan Type | Example Interest Rate (Approximate) | Accrual During Deferment/Forbearance |

|---|---|---|

| Subsidized Federal Stafford Loan | 4-7% | No (during in-school period) |

| Unsubsidized Federal Stafford Loan | 4-7% | Yes |

| Federal PLUS Loan | 7-10% | Yes |

Note: These are example rates and can change. Actual rates depend on the loan disbursement date and other factors. Consult the official federal student aid website for current rates.

Common Repayment Scenarios and Financial Implications

Let’s illustrate the impact of different repayment plans with a few examples. These examples are for illustrative purposes and may not reflect every individual’s situation.

Scenario 1: A borrower with $30,000 in federal student loans chooses the standard repayment plan (10 years). Assuming a 5% interest rate, their monthly payment would be approximately $330, and the total interest paid would be around $10,000.

Scenario 2: The same borrower chooses an income-driven repayment plan. Their monthly payments might be lower, perhaps $200, but the repayment period could extend to 20 years or more, resulting in significantly higher total interest paid, potentially exceeding $20,000.

These examples highlight the trade-off between lower monthly payments and higher total interest costs. Careful planning and consideration of long-term financial implications are crucial when choosing a repayment plan.

The Biden Administration’s Student Loan Forgiveness Plan

The Biden administration’s student loan forgiveness plan aimed to provide substantial debt relief to millions of Americans burdened by student loan debt. While ambitious in scope, the plan faced significant legal challenges and ultimately underwent significant revisions before its implementation was halted by the Supreme Court. Understanding its proposed structure, eligibility requirements, and legal battles is crucial to grasping its impact (and lack thereof) on the national student loan landscape.

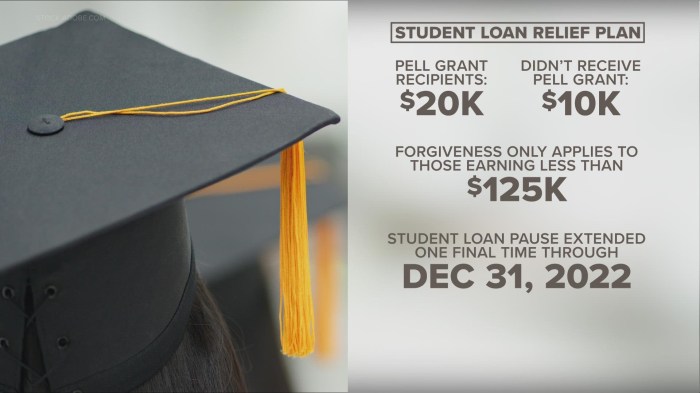

The plan initially proposed up to $20,000 in student loan forgiveness for Pell Grant recipients and up to $10,000 for non-Pell Grant recipients. This relief was intended to target borrowers most in need and alleviate the burden of student loan debt, thereby stimulating the economy. The administration argued this was a necessary step to address economic inequality and promote social mobility. The plan aimed to automatically apply forgiveness to eligible borrowers, simplifying the process and making it more accessible.

Eligibility Criteria for Student Loan Forgiveness

Eligibility for the proposed forgiveness hinged on several key factors. Borrowers needed to have received a federal student loan disbursed before June 30, 2022. Income limits were also established, with single borrowers needing to earn less than $125,000 annually and married couples less than $250,000. The amount of forgiveness was directly tied to Pell Grant receipt. Pell Grants are federal funds awarded to undergraduate students with exceptional financial need; recipients of Pell Grants were eligible for the higher $20,000 forgiveness amount, while non-recipients were eligible for up to $10,000. This tiered system reflected the administration’s intention to prioritize those most financially vulnerable.

Potential Legal Challenges and Their Impact

The plan faced significant legal challenges from the outset. Six states, led by Nebraska, filed a lawsuit arguing that the administration lacked the authority to implement such a sweeping forgiveness program without explicit Congressional authorization. The Supreme Court ultimately sided with the plaintiffs, halting the implementation of the plan. The court’s decision highlighted the limitations of executive power in enacting such significant policy changes without explicit legislative backing. This ruling significantly impacted the plan’s implementation, effectively nullifying the proposed debt relief for millions of borrowers.

Comparison with Previous Student Loan Relief Initiatives

The Biden administration’s plan was more ambitious in scope than previous student loan relief efforts. While previous administrations had implemented programs offering targeted loan forgiveness or modifications to repayment plans (such as income-driven repayment plans), none had attempted such a large-scale, blanket forgiveness program. For example, the Obama administration’s efforts focused primarily on modifying existing repayment plans to make them more affordable, rather than outright forgiveness. The Biden plan represented a significant departure from these earlier, more incremental approaches, aiming for a more immediate and impactful solution to the student debt crisis. The legal challenges it faced, however, underscore the political and legal complexities involved in implementing such transformative policies.

Impact on Borrowers and the Economy

Student loan forgiveness, on a widespread scale, presents a complex interplay of potential economic benefits and drawbacks for both individual borrowers and the national economy. Understanding these impacts requires careful consideration of various factors, from immediate relief for indebted individuals to long-term effects on government spending and overall economic growth.

The potential economic consequences of widespread student loan forgiveness are multifaceted and far-reaching. A significant injection of capital into the economy, as borrowers redirect funds previously allocated to loan repayment, could stimulate consumer spending and boost economic activity. Conversely, the substantial cost to the federal budget could lead to increased national debt and potential inflationary pressures. The effects on borrowers’ financial well-being and spending habits are also crucial considerations.

Economic Impact of Student Loan Forgiveness

Widespread student loan forgiveness could have a substantial impact on the US economy. A significant portion of borrowers’ disposable income is currently dedicated to loan repayment. Forgiveness could free up this money, potentially leading to increased consumer spending on goods and services, boosting economic growth. This effect is particularly pronounced among younger borrowers who may be more likely to spend additional income rather than save it. However, the magnitude of this effect is debated, with some economists arguing that the impact would be muted due to factors such as existing debt levels and other economic conditions. For example, a study by the Brookings Institution estimated that the macroeconomic effects of the Biden administration’s proposed forgiveness plan would be relatively small, though potentially positive. Conversely, a significant increase in aggregate demand could potentially contribute to inflation, eroding purchasing power. The impact will depend on how borrowers utilize the freed-up funds and the overall state of the economy.

Impact on Borrowers’ Financial Well-being

Student loan debt significantly impacts borrowers’ financial well-being. Many struggle to save for retirement, purchase homes, or start businesses due to substantial monthly loan payments. Forgiveness could alleviate this burden, improving their credit scores, reducing financial stress, and potentially enabling them to make larger investments in their future. For instance, borrowers might be able to invest more in education or job training, increasing their earning potential. On the other hand, some argue that forgiveness could disincentivize responsible borrowing behavior in the future, leading to increased debt levels for future generations. The long-term effects on individual financial stability will depend on how individuals manage their newfound financial flexibility.

Consequences for the Federal Budget and National Debt

The most significant drawback of widespread student loan forgiveness is the substantial cost to the federal budget. The amount would depend on the scope of the program, but it could run into trillions of dollars. This would inevitably increase the national debt and could lead to reduced government spending in other areas, potentially impacting essential social programs or infrastructure investments. For example, the Congressional Budget Office estimated that the Biden administration’s plan could cost over $400 billion. This added debt could also put upward pressure on interest rates, increasing the cost of borrowing for both the government and individuals. The long-term consequences for fiscal sustainability are a major concern.

Summary of Potential Impacts

| Category | Positive Impact | Negative Impact | Supporting Data |

|---|---|---|---|

| Borrowers | Increased disposable income, improved credit scores, reduced financial stress, increased investment in future | Potential disincentive to responsible borrowing, unequal distribution of benefits | Studies showing correlation between debt and financial stress; analyses of credit score improvements following debt forgiveness programs. |

| Economy | Stimulated consumer spending, boosted economic growth, increased investment in education and job training | Potential inflation, increased national debt, reduced government spending in other areas | Economic models predicting the impact of increased consumer spending; government budget projections related to debt and spending. |

| Federal Budget | Potential for long-term economic growth offsetting the cost | Significant increase in national debt, potential for reduced government spending in other sectors | Congressional Budget Office estimates of the cost of student loan forgiveness programs. |

| Future Generations | Potential for improved economic opportunities, reduced inequality | Increased burden of national debt, potential disincentive for responsible borrowing | Studies on the intergenerational effects of debt and economic inequality. |

Alternative Solutions and Future of Student Loan Debt

The current student loan crisis necessitates a multifaceted approach beyond simple forgiveness. Addressing the root causes and exploring alternative solutions is crucial to prevent future debt burdens and ensure equitable access to higher education. This section will examine income-driven repayment reforms, propose long-term solutions, and Artikel a policy proposal for systemic reform.

Income-Driven Repayment Reforms

Income-driven repayment (IDR) plans offer a crucial pathway for borrowers struggling to manage their student loan debt. These plans tie monthly payments to a borrower’s income and family size, resulting in lower monthly payments and potentially loan forgiveness after a set period. However, current IDR plans suffer from complexities, inconsistencies across programs, and administrative inefficiencies. Reforms should focus on simplifying the application process, standardizing calculations, and ensuring robust oversight to maximize their effectiveness. This would provide much-needed relief to struggling borrowers and promote responsible borrowing practices.

Potential Long-Term Solutions for Managing Student Loan Debt

Several long-term strategies can help manage and mitigate the student loan debt crisis. These solutions address both the immediate burden on borrowers and the systemic issues contributing to the problem.

- Increased Funding for Pell Grants: Expanding Pell Grant eligibility and increasing the maximum award amount would reduce the need for students to borrow as much. This would directly target the affordability of higher education and reduce reliance on loans. The potential benefit is a significant reduction in overall student loan debt, while a potential drawback could be the increased financial burden on the federal government.

- Tuition Reform: Implementing policies to control the rising cost of tuition, such as increased state funding for public universities or caps on tuition increases, would address the root cause of the debt crisis. Benefits include reduced borrowing and improved affordability. However, this may require difficult political compromises and might face resistance from universities concerned about their funding models.

- Expansion of Income Share Agreements (ISAs): ISAs offer an alternative financing model where investors provide funds for tuition in exchange for a percentage of a graduate’s future income. Benefits include reduced upfront costs for students and aligned incentives between investors and students. Drawbacks include potential risks for borrowers if their income doesn’t meet expectations, and regulatory challenges in establishing a fair and transparent system.

- Targeted Loan Forgiveness Programs: While broad-based forgiveness has significant economic implications, targeted programs focusing on specific professions (e.g., teachers, nurses) or borrowers facing severe financial hardship could offer relief while limiting overall cost. Benefits include targeted assistance to individuals in need and potential societal benefits through supporting essential professions. Drawbacks include the potential for inequities and difficulties in defining eligibility criteria fairly.

Policy Proposal for Reforming the Student Loan System

A comprehensive reform of the student loan system requires a multi-pronged approach. This proposal focuses on prevention and proactive measures to avoid future crises.

- Strengthening IDR Programs: Simplify application processes, standardize calculations across programs, and improve transparency and oversight to ensure borrowers benefit from these programs. This would make existing support mechanisms more effective.

- Increased Transparency in College Costs: Require universities to provide clear and accessible information about tuition, fees, and financial aid options to enable students to make informed borrowing decisions. This promotes responsible borrowing practices.

- Investment in Affordable Higher Education: Increase funding for Pell Grants and other need-based aid programs, and implement policies to control tuition increases. This would address the root cause of high student loan debt.

- Promote Alternative Financing Models: Explore and regulate alternative financing models like ISAs to offer students more choices beyond traditional loans. This introduces more diversity in financing.

Student Loan Forgiveness and Social Equity

The debate surrounding student loan forgiveness is deeply intertwined with issues of social equity. Arguments both for and against forgiveness often center on how existing debt structures impact different socioeconomic groups and their opportunities for upward mobility. Understanding these perspectives requires examining the disproportionate burden of student loan debt on specific demographics and its long-term consequences.

Student loan forgiveness proponents argue that the current system perpetuates existing inequalities. They contend that high levels of student debt disproportionately affect marginalized communities, hindering their ability to achieve financial stability and limiting their social mobility. Conversely, opponents argue that forgiveness would be unfair to those who diligently paid off their loans or chose not to pursue higher education, potentially leading to resentment and economic instability. They may also question the overall cost and effectiveness of such a large-scale initiative.

Disproportionate Impact of Student Loan Debt on Demographic Groups

Student loan debt does not affect all borrowers equally. Data consistently reveals that Black and Hispanic borrowers, as well as those from lower socioeconomic backgrounds, often carry significantly higher debt burdens relative to their income than their white and wealthier counterparts. This disparity stems from a complex interplay of factors, including lower access to financial aid, higher tuition costs at institutions they attend, and fewer opportunities for well-paying jobs post-graduation. For example, studies from organizations like the Brookings Institution have shown a significant racial wealth gap exacerbated by student loan debt. Black borrowers, on average, owe more and struggle more to repay than white borrowers with comparable educational attainment. Similarly, first-generation college students often face greater financial challenges and may take on more debt to finance their education.

Student Loan Debt and Social Mobility

The relationship between student loan debt and social mobility is complex but demonstrably negative for many. High levels of student loan debt can significantly impede upward mobility by restricting access to crucial life milestones such as homeownership, starting a family, and investing in business ventures. The weight of repayment can delay or prevent career changes, forcing individuals to stay in jobs they may not enjoy or that don’t offer sufficient earning potential. This creates a cycle of debt that makes it difficult to build wealth and advance economically, perpetuating intergenerational inequality. Research by the Federal Reserve Bank of New York, for instance, has highlighted the significant impact of student debt on homeownership rates, particularly for younger generations.

Visual Representation of Student Loan Debt Disparities

Imagine a bar graph. The horizontal axis represents different socioeconomic backgrounds, categorized perhaps as low-income, middle-income, and high-income families. The vertical axis represents the average student loan debt burden per borrower within each group. The bars would visually demonstrate a clear disparity, with the bar representing low-income families significantly taller than those representing middle- and high-income families. Further segmentation could be added to show racial and ethnic disparities within each income bracket, highlighting the compounding effect of multiple forms of disadvantage. For example, within the low-income bracket, a separate bar for Black borrowers might be even taller than the bar for low-income borrowers overall, visually illustrating the disproportionate burden on this group. This visual representation would clearly illustrate how student loan debt is not evenly distributed across socioeconomic groups, exacerbating existing inequalities.

Conclusive Thoughts

The future of student loan debt in the US hinges on a multifaceted approach that balances immediate relief with long-term systemic reform. While the Biden administration’s forgiveness plan offers a significant step towards addressing the crisis, its ultimate success remains uncertain. Ultimately, sustainable solutions necessitate a combination of targeted relief measures, reforms to income-driven repayment programs, and a critical examination of the affordability and accessibility of higher education itself. The ongoing dialogue and policy debates surrounding this issue will undoubtedly shape the financial well-being of millions for years to come.

FAQs

What are income-driven repayment plans?

Income-driven repayment (IDR) plans tie your monthly student loan payments to your income and family size. They offer lower monthly payments than standard repayment plans, potentially extending the repayment period.

What happens if I don’t repay my student loans?

Failure to repay your student loans can lead to wage garnishment, tax refund offset, and damage to your credit score. In severe cases, it could impact your ability to obtain loans or credit in the future.

Are private student loans included in the forgiveness programs?

Generally, federal student loan forgiveness programs do not apply to private student loans. Private loan terms and conditions are determined by the lender, not the government.

What is the difference between subsidized and unsubsidized loans?

Subsidized loans do not accrue interest while you’re in school (under certain conditions). Unsubsidized loans accrue interest from the time they are disbursed, even while you are enrolled.