The question of student loan forgiveness hangs heavy in the air, a complex issue intertwined with economic policy, political maneuvering, and the very future of higher education. Millions grapple with crippling debt, while policymakers debate the potential consequences of widespread loan cancellation. This exploration delves into the multifaceted aspects of this pressing national concern, examining current programs, political viewpoints, economic impacts, and alternative solutions to navigate this challenging landscape.

From analyzing existing forgiveness programs and their eligibility criteria to projecting the economic ramifications of large-scale debt relief, we’ll consider the perspectives of borrowers, policymakers, and economists. We will also explore innovative alternatives and the crucial role of higher education institutions in mitigating the student debt crisis. The journey will uncover the intricate web of factors shaping the future of student loan debt and its potential impact on generations to come.

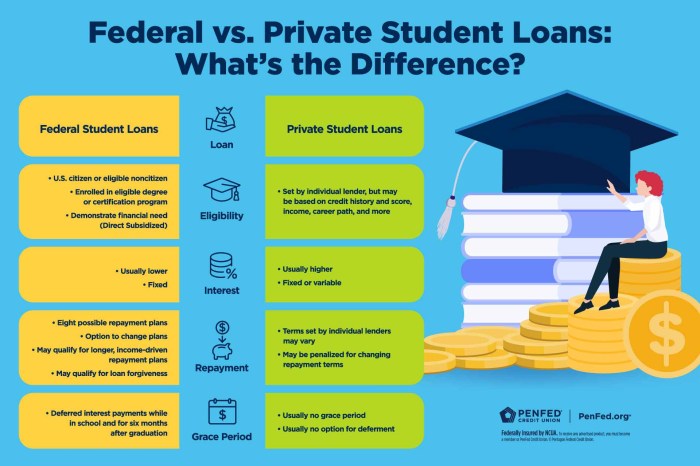

Current Student Loan Forgiveness Programs

The US government offers several programs designed to forgive or reduce the burden of student loan debt. These programs vary significantly in their eligibility requirements and the amount of forgiveness offered. Understanding the nuances of each program is crucial for borrowers seeking relief.

Types of Student Loan Forgiveness Programs

Several federal programs provide pathways to student loan forgiveness. These programs are targeted at specific professions, employment situations, or individuals with disabilities. Understanding their differences is essential for determining eligibility.

Public Service Loan Forgiveness (PSLF) Program

The PSLF program forgives the remaining balance on federal Direct Loans after 120 qualifying monthly payments under a qualifying repayment plan while working full-time for a qualifying government or non-profit organization.

| Program Name | Eligibility Requirements | Forgiveness Amount | Application Process |

|---|---|---|---|

| Public Service Loan Forgiveness (PSLF) | 120 qualifying monthly payments under a qualifying repayment plan while working full-time for a qualifying government or non-profit organization; Federal Direct Loans | Remaining loan balance | Apply through the Federal Student Aid website. Requires employment verification. |

| Teacher Loan Forgiveness Program | Full-time employment as an elementary or secondary school teacher for five complete and consecutive academic years in a low-income school; Federal Direct Loans or FFEL Program loans | Up to $17,500 | Apply through the Federal Student Aid website. Requires documentation of employment and school status. |

| Income-Driven Repayment (IDR) Plans | Various eligibility requirements based on income and family size; Federal Direct Loans and FFEL Program loans (consolidated) | Remaining balance after 20-25 years (depending on plan) | Select an IDR plan through your loan servicer. Requires annual income recertification. |

| Total and Permanent Disability (TPD) Discharge | Documentation of total and permanent disability from the Social Security Administration (SSA) or the Department of Veterans Affairs (VA); Federal Direct Loans, FFEL Program loans, and Perkins Loans | Remaining loan balance | Apply through your loan servicer, providing required documentation from the SSA or VA. |

Comparison of Forgiveness Programs

The programs differ significantly in their eligibility criteria, forgiveness amounts, and application processes. PSLF targets public service employees, while the Teacher Loan Forgiveness Program is specifically for teachers in low-income schools. IDR plans offer gradual forgiveness based on income, and TPD discharge is for borrowers with disabilities. Each program has its own specific requirements and application procedures. It’s important to carefully review the eligibility criteria for each program to determine the best option for your situation.

Political Landscape and Student Loan Debt

The issue of student loan debt has become a significant political battleground in recent years, shaping election campaigns and influencing legislative agendas. Differing philosophies on the role of government intervention in higher education and the economy fuel the debate, leading to varied proposals and significant political polarization. Understanding these diverse perspectives is crucial to comprehending the ongoing discussion surrounding student loan forgiveness and reform.

The current political landscape reveals a stark divide on the issue of student loan forgiveness. Progressive Democrats generally advocate for broad-based forgiveness, viewing student debt as a systemic barrier to economic mobility and a crucial element of social justice. Conversely, many Republicans express concerns about the economic implications of widespread forgiveness, arguing that it could exacerbate inflation, disproportionately benefit higher earners, and unfairly burden taxpayers who did not attend college. While some Republicans acknowledge the need for student loan reform, their proposed solutions typically focus on targeted relief or changes to the existing loan system rather than large-scale forgiveness.

Key Political Figures and Proposed Solutions

Several key political figures have taken prominent stances on student loan debt. President Biden, for example, has overseen the extension of payment pauses and implemented targeted forgiveness programs, although these have faced legal challenges and have not addressed the scale of the problem advocated for by many progressives. Senator Elizabeth Warren has been a vocal advocate for broad-based student loan forgiveness, proposing plans to cancel significant amounts of student loan debt for millions of Americans. Conversely, figures such as Senator Mitch McConnell have voiced strong opposition to widespread forgiveness, arguing against its economic feasibility and fairness. These differing perspectives highlight the significant political chasm surrounding this issue.

Potential Economic Impacts of Widespread Student Loan Forgiveness

The potential economic impacts of widespread student loan forgiveness are complex and subject to ongoing debate among economists. Proponents argue that forgiveness could stimulate the economy by freeing up borrowers’ disposable income, leading to increased consumer spending and economic growth. They also point to potential benefits for the housing market and other sectors dependent on consumer spending. Opponents, however, warn that forgiveness could lead to inflation, increase the national debt, and potentially distort the higher education market by reducing the incentive for responsible borrowing and prudent financial planning. The actual economic effects would depend on the scale and design of any forgiveness program, as well as broader macroeconomic conditions. For example, a targeted forgiveness program focused on lower-income borrowers might have different economic effects than a broad-based program.

Timeline of Significant Legislative Actions

A timeline of significant legislative actions related to student loan debt reveals a pattern of evolving policy responses. The creation of the federal student loan program itself marked a significant intervention, expanding access to higher education but also leading to the accumulation of substantial debt. Subsequent legislative actions, including various attempts at loan reform and targeted relief programs, reflect the ongoing political struggle to address this complex issue. For example, the HEROES Act of 2003 provided some debt relief for victims of natural disasters, while the American Rescue Plan Act of 2021 included provisions extending the COVID-19 payment pause. These, along with President Biden’s recent targeted forgiveness initiatives, illustrate the piecemeal nature of the legislative response to student loan debt, and the ongoing political challenges involved in achieving more comprehensive reform.

Economic Impacts of Student Loan Forgiveness

The complete elimination or substantial forgiveness of student loan debt would trigger significant and multifaceted economic consequences, impacting individuals, businesses, and the government. The scale of these effects depends heavily on the specifics of any forgiveness plan, such as the eligibility criteria and the method of implementation. Understanding these potential impacts is crucial for informed policymaking.

The potential economic effects of student loan forgiveness are complex and far-reaching, affecting various sectors and demographics differently. A comprehensive analysis necessitates considering both short-term and long-term implications, acknowledging the inherent uncertainties involved in economic forecasting.

Inflationary Pressures

Widespread student loan forgiveness would inject a considerable amount of money into the economy. Borrowers would have more disposable income, potentially leading to increased consumer spending. This surge in demand, if not met by a corresponding increase in supply, could push prices upward, contributing to inflation. The magnitude of this inflationary effect would depend on factors such as the size of the forgiven debt, the speed of its disbursement, and the overall state of the economy. For example, if the economy is already operating near full capacity, the inflationary pressure would likely be more pronounced than in a recessionary environment. Historical examples of large-scale government spending programs, such as stimulus packages, provide some insight into the potential for increased inflation following significant financial injections. However, the specific impact of student loan forgiveness would differ due to the targeted nature of the program and the differing spending habits of the recipients.

Government Spending and the Budget Deficit

Student loan forgiveness would represent a substantial cost to the federal government, adding to the national debt. The exact amount would depend on the scale of the forgiveness program. This increased deficit could lead to several potential consequences, including higher interest rates on government borrowing, potentially crowding out private investment. The government might also need to implement austerity measures in other areas to offset the cost of forgiveness, potentially impacting essential services or social programs. The long-term implications for the federal budget would be significant, requiring careful consideration of fiscal sustainability. For instance, a program forgiving $1 trillion in student loan debt would necessitate a significant adjustment to the federal budget, possibly requiring tax increases, spending cuts, or a combination of both to maintain fiscal stability.

Arguments For and Against Student Loan Forgiveness from Different Economic Perspectives

Economists hold differing views on the economic wisdom of student loan forgiveness. Keynesian economists, for example, might argue that the increased consumer spending resulting from forgiveness would stimulate aggregate demand, boosting economic growth. Conversely, some classical economists might argue that forgiveness would distort markets, create moral hazard (encouraging future borrowing without due diligence), and ultimately lead to unsustainable government debt. Supply-side economists might focus on the potential impact on labor markets, arguing that forgiveness could increase labor mobility and productivity by freeing individuals from the burden of debt. However, others might counter that the benefits are not guaranteed, and the costs to the government outweigh the potential benefits.

Hypothetical Scenario: Complete Loan Forgiveness

Imagine a scenario where the government forgives all outstanding student loan debt totaling $1.7 trillion (a hypothetical figure). In the short term, a significant portion of this money would likely be used for immediate needs, such as paying down other debts, improving living standards, and increasing consumer spending. This could lead to a temporary boost in economic activity, potentially increasing GDP growth. However, this surge in demand could also exacerbate inflationary pressures, potentially leading to a rise in interest rates by the Federal Reserve to combat inflation. In the long term, the impact is less certain. Increased consumer spending could lead to sustained economic growth, but the increased national debt could lead to higher interest rates and potentially slower economic growth in the future. The impact on the labor market would also be complex, with potential benefits from increased labor mobility and productivity offset by the potential costs of reduced incentives to repay loans and increased government debt. This scenario highlights the trade-offs inherent in considering large-scale student loan forgiveness.

The Impact on Borrowers

Student loan forgiveness would have a profound and multifaceted impact on individual borrowers, extending beyond the simple cancellation of debt. The effects would ripple through their financial lives, impacting their credit scores, future borrowing capabilities, and even their mental well-being. Understanding these consequences is crucial to assessing the overall effectiveness and equity of any large-scale forgiveness program.

Loan forgiveness would offer immediate and substantial financial relief for many borrowers. The elimination of monthly payments could free up significant portions of their disposable income, allowing them to pursue financial goals like homeownership, starting a family, or investing in their education or businesses. This injection of capital into the economy could also stimulate consumer spending and economic growth.

Credit Score Implications

The effect of loan forgiveness on credit scores is complex and depends on how the forgiveness is implemented. If the forgiven debt is reported as “paid in full,” it could positively impact credit scores over time. However, if the forgiveness is reported differently, or if the borrower had a history of missed payments before forgiveness, the impact on their score might be less pronounced or even negative. For example, a borrower with a history of responsible repayment who receives forgiveness might see a slight increase in their score as the debt is removed, while a borrower with a history of delinquencies might not see as much of a positive effect. Credit reporting agencies would need to establish clear guidelines to ensure fair and consistent reporting of forgiven loans.

Future Borrowing Capacity

The ability to borrow money in the future, such as for a mortgage or car loan, would be influenced by loan forgiveness. While the immediate relief is beneficial, lenders often use debt-to-income ratios to assess risk. Forgiveness, while removing existing debt, might not immediately improve these ratios, especially if the borrower has other outstanding debts. Conversely, the increased disposable income resulting from forgiveness could strengthen their borrowing power over time by improving their debt-to-income ratio and credit history, demonstrating improved financial responsibility.

Psychological Impact of Debt Alleviation

The psychological burden of student loan debt is substantial. Many borrowers experience chronic stress, anxiety, and depression due to the weight of their debt. Studies have shown a correlation between high levels of student loan debt and decreased mental health. Loan forgiveness could significantly alleviate this psychological burden, freeing borrowers from the constant worry and stress associated with repayment. This positive mental health impact could translate into increased productivity, improved relationships, and overall improved well-being.

Case Study: Sarah’s Journey

Sarah graduated with a degree in nursing, burdened by $150,000 in student loans. For years, she struggled to make her monthly payments, often delaying other essential expenses like healthcare and savings. The constant pressure of debt significantly impacted her mental health, leading to anxiety and sleeplessness. She postponed starting a family and buying a home due to her financial constraints. If Sarah received loan forgiveness, the immediate relief would be transformative. She could finally focus on her career, invest in her personal well-being, and pursue her long-delayed life goals without the constant financial pressure. This scenario illustrates the profound personal and societal benefits that could result from targeted loan forgiveness programs.

Alternative Solutions to Student Loan Debt

The current debate surrounding student loan forgiveness highlights the need for a multifaceted approach to addressing the burden of student loan debt. While complete forgiveness is a significant policy proposal, exploring alternative solutions is crucial for developing a more sustainable and equitable system. These alternatives focus on making repayment more manageable and preventing future debt accumulation.

Several strategies offer viable pathways to alleviate the student loan crisis without resorting to widespread forgiveness. These approaches aim to balance the needs of borrowers with the financial realities of the government and the higher education system. Effective solutions require a nuanced understanding of the complexities of student loan debt and the varying circumstances of borrowers.

Income-Driven Repayment Plans Compared to Loan Forgiveness

Income-driven repayment (IDR) plans adjust monthly payments based on a borrower’s income and family size. This contrasts sharply with loan forgiveness, which eliminates the debt entirely. IDR plans offer immediate relief by lowering monthly payments, potentially making them more affordable for struggling borrowers. However, they often extend the repayment period significantly, leading to higher overall interest payments compared to standard repayment plans. Loan forgiveness, while offering complete relief, has substantial budgetary implications and may not address the root causes of high student loan debt. The effectiveness of each approach depends on individual circumstances and long-term financial goals. A borrower with a low income and a large loan balance might benefit significantly from an IDR plan, while someone with a higher income and a smaller loan might find standard repayment more efficient.

Alternative Solutions: Key Features

A range of alternative solutions can help manage and reduce student loan debt. These solutions address different aspects of the problem, from making repayment more manageable to preventing future debt accumulation.

- Income-Driven Repayment (IDR) Plans: These plans calculate monthly payments based on income and family size, offering lower monthly payments than standard plans. However, repayment periods are typically longer, resulting in higher total interest paid. Examples include the Revised Pay As You Earn (REPAYE), Income-Based Repayment (IBR), and Income-Contingent Repayment (ICR) plans.

- Targeted Loan Forgiveness Programs: These programs focus on specific groups of borrowers, such as public service workers or those with disabilities. This approach addresses the debt burden of specific populations while minimizing the overall cost of widespread forgiveness. The Public Service Loan Forgiveness (PSLF) program is an example.

- Debt Consolidation and Refinancing: Consolidating multiple loans into a single loan with a lower interest rate can simplify repayment and potentially reduce the total interest paid. Refinancing allows borrowers to secure a new loan with better terms, potentially lowering their monthly payments.

- Increased Funding for Need-Based Grants and Scholarships: Investing in need-based financial aid reduces the reliance on loans for higher education, addressing the problem at its source. This proactive approach helps prevent future debt accumulation.

- Tuition Reform and Cost Control: Addressing the rising cost of higher education is crucial. This could involve increased state funding for public universities, greater transparency in college pricing, and incentives for colleges to control costs.

The Role of Higher Education Institutions

The escalating student loan debt crisis is a complex issue with multiple contributing factors. While individual borrowers bear responsibility for their borrowing decisions, the role of higher education institutions in driving up costs and contributing to the problem cannot be ignored. Colleges and universities, through their pricing structures and operational practices, significantly influence the amount students borrow and the resulting debt burden.

Universities’ pricing strategies, including tuition increases that often outpace inflation and the growth of ancillary fees, have substantially increased the cost of attendance. This, coupled with a lack of transparency in pricing and financial aid processes, often leaves students and families struggling to understand the true cost of a degree and making informed borrowing decisions. Furthermore, the expansion of non-academic services and amenities, while potentially beneficial to student life, adds to the overall cost and contributes to rising tuition.

Tuition and Fee Structures

Many universities have implemented significant tuition increases over the past few decades, often exceeding the rate of inflation and wage growth. This has led to a reliance on student loans to bridge the gap between the cost of education and available financial resources. Several factors contribute to these increases, including reduced state funding for public institutions, escalating administrative costs, and the pressure to compete with other universities by offering more amenities and services. A more transparent and predictable tuition model, coupled with a commitment to controlling non-academic spending, could significantly alleviate the financial burden on students.

Strategies for Reducing Higher Education Costs

Institutions can implement various strategies to mitigate the cost of higher education. These include increasing the availability of need-based financial aid, expanding merit-based scholarships, and implementing more efficient operational practices to reduce administrative costs. Investing in online learning technologies could also expand access to education and reduce the need for expensive on-campus infrastructure. Furthermore, universities could explore innovative funding models, such as income-share agreements, to help reduce the upfront cost of tuition.

Examples of Institutions Addressing Affordability

Some institutions are proactively addressing affordability. For instance, several public universities have frozen or capped tuition increases, demonstrating a commitment to keeping education accessible. Other institutions are expanding their scholarship programs and investing in financial literacy initiatives to help students make informed borrowing decisions. Purdue University’s efforts to expand online learning and offer more affordable degree options serve as a positive example. Similarly, initiatives focusing on reducing the cost of textbooks and other educational materials are gaining traction.

Potential Impact of Cost-Reduction Strategies

Implementing these cost-reduction strategies could have a significant impact on student debt levels. By making college more affordable, students would rely less on loans, resulting in lower overall debt burdens upon graduation. This, in turn, would positively affect their long-term financial well-being, enabling them to achieve their financial goals sooner, such as purchasing homes, starting families, and contributing more fully to the economy. The reduced reliance on loans would also contribute to a healthier overall economic climate, mitigating the risks associated with widespread student loan debt.

Long-Term Implications of Student Loan Policies

The long-term consequences of various student loan policies are far-reaching, impacting not only individual borrowers but also the future of higher education and the overall economy. Understanding these implications requires considering the interplay between debt levels, access to education, and the potential for economic growth or stagnation. Different approaches to student loan forgiveness, interest rates, and repayment plans will create distinct ripple effects across generations.

The impact on future generations is particularly crucial. High levels of student loan debt can lead to delayed major life decisions such as homeownership, starting a family, and retirement planning. This can create a cycle of financial strain that extends across generations, impacting economic mobility and social well-being. Conversely, policies that promote affordable higher education can lead to increased economic productivity and a more equitable society.

Potential Scenarios for the Future of Student Loan Debt

Several potential scenarios could unfold regarding student loan debt in the US. One scenario involves a continuation of the current trend, with steadily increasing debt levels and ongoing debates over forgiveness programs. This could lead to a chronic burden on the economy and a widening gap in economic opportunity. Another scenario might involve significant policy changes, such as substantial loan forgiveness coupled with reforms to higher education financing. This could alleviate the immediate crisis but may also necessitate significant changes in the way higher education is funded and accessed. A third possibility is a gradual reduction in student loan debt through a combination of responsible borrowing, increased financial literacy, and targeted government intervention. This approach would likely involve a slower, more sustainable solution, prioritizing long-term stability over immediate relief. The specific trajectory will depend on political will, economic conditions, and the evolution of higher education itself.

Visual Representation of Long-Term Effects

Imagine a branching tree diagram. The trunk represents the current state of student loan debt. Three major branches extend upward, representing the three potential scenarios described above: (1) Continuing high debt levels, shown by a branch that continues to thicken and grow upward, eventually becoming burdened by leaves representing individual borrowers struggling under heavy debt; (2) Significant policy changes, represented by a branch that splits into several smaller, healthier branches symbolizing a more equitable distribution of resources and opportunities; and (3) Gradual reduction in debt, depicted by a branch that steadily grows but remains relatively slender, representing a more sustainable and manageable approach. The leaves on each branch represent various long-term outcomes: economic growth or stagnation, increased or decreased social mobility, and the overall health and accessibility of higher education. The overall health and vibrancy of the tree represent the long-term well-being of the higher education system and the broader economy. The leaves’ colors can further illustrate economic prosperity (green) or hardship (brown). The size of the branches reflects the scale of the impact, with thicker branches representing larger consequences.

Conclusive Thoughts

The question of whether student loans will disappear entirely remains unanswered, a complex issue dependent on evolving political landscapes and economic realities. While complete forgiveness presents significant challenges, the current system is undeniably strained. Exploring alternative solutions, fostering greater affordability in higher education, and promoting responsible borrowing practices are crucial steps toward a more sustainable future. Ultimately, a comprehensive approach addressing both immediate relief and long-term systemic change is needed to navigate the ongoing student loan debt crisis effectively.

FAQ Section

What is the average student loan debt in the US?

The average student loan debt varies depending on the source and year but generally falls within a range of tens of thousands of dollars.

Can I consolidate my student loans?

Yes, federal student loan consolidation is an option that combines multiple loans into one, often simplifying repayment.

What are income-driven repayment plans?

Income-driven repayment plans adjust your monthly payments based on your income and family size, potentially lowering your monthly burden.

What happens if I default on my student loans?

Defaulting on student loans can have severe consequences, including wage garnishment, tax refund offset, and damage to your credit score.